{kind=link}

The Fiscal Dominance Trap: When Government Debt Dictates Monetary Policy

For decades, the gold standard of economic stability has been the independence of the central bank. The theory is simple: by separating the people who spend the money (the government) from the people who print it (the central bank), a nation can prevent short-term political whims from triggering long-term hyperinflation. However, a dangerous trend is emerging globally—a phenomenon known as fiscal dominance.

Fiscal dominance occurs when a government’s debt becomes so massive and its fiscal indiscipline so ingrained that the central bank can no longer raise interest rates to fight inflation without risking a sovereign default. The central bank ceases to be an independent guardian of price stability and becomes a tool for financing government deficits.

- Fiscal Dominance: A state where monetary policy is subservient to the government’s borrowing needs.

- The Inflation Cycle: When central banks prioritize government solvency over inflation targets, price stability collapses.

- Global Risk: From emerging markets to the U.S. Federal Reserve, the tension between debt servicing and inflation control is reaching a breaking point.

The Anatomy of Monetary Mismanagement

The path to a fiscal crisis usually begins with fiscal indiscipline—excessive spending without corresponding revenue growth. When governments rely on “dilettante” policy-making, they often ignore the long-term implications of debt-to-GDP ratios, assuming that future growth or central bank intervention will solve the problem.

The Central Bank’s Dilemma

When inflation rises, the standard response is to raise interest rates. This cools the economy and protects the currency. But in a state of fiscal dominance, raising rates increases the cost of servicing the government’s own debt. If the interest payments become unsustainable, the central bank faces a choice: allow the government to default or retain rates artificially low to ensure solvency.

Choosing the latter leads to monetary mismanagement. By keeping rates low despite rising inflation, the central bank effectively prints money to fund the deficit, which further fuels inflation in a destructive feedback loop.

Case Studies in Fiscal Pressure

This is not a theoretical risk; it is a current reality across various economic tiers. The tension between fiscal needs and monetary mandates is playing out in real-time.

Emerging Market Volatility

In regions like Zimbabwe, the struggle to anchor stability is a constant battle against unresolved fiscal pressures. According to reporting by The Zimbabwe Independent, the Reserve Bank of Zimbabwe (RBZ) has attempted to reposition itself toward its foundational mandate, yet persistent fiscal squeezes continue to cast a shadow over the economic outlook.

The Developed Market Risk

Even the world’s reserve currency is not immune. Analysts have warned that the U.S. Federal Reserve is confronting a structural crisis where Washington’s debt could eventually force the bank to abandon its inflation mandate. As detailed by the Foreign Affairs Forum, the U.S. Risks falling into the same “fiscal dominance trap” that has historically crippled emerging markets.

The Long-Term Consequences of Policy Failure

When the boundary between the treasury and the central bank blurs, the results are predictable and painful. The “concentrated” result of this mismanagement typically manifests in three stages:

- Erosion of Trust: Investors lose confidence in the currency, leading to capital flight and a plummeting exchange rate.

- Inflationary Spirals: As the currency weakens, the cost of imports rises, pushing inflation higher and forcing the central bank to print more money to cover costs.

- Economic Stagnation: High inflation and volatile interest rates discourage long-term investment, killing productivity and growth.

FAQ: Understanding Fiscal Dominance

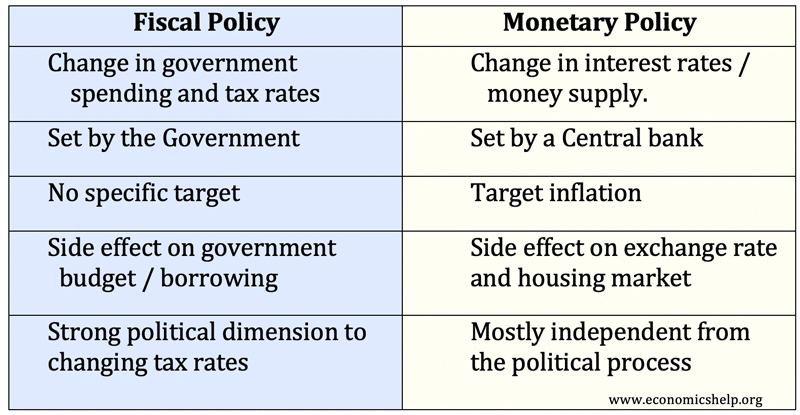

What is the difference between fiscal policy and monetary policy?

Fiscal policy refers to government spending and taxation. Monetary policy refers to the control of the money supply and interest rates, typically managed by a central bank.

Why is central bank independence so important?

Independence prevents politicians from printing money to fund popular short-term projects, which would otherwise lead to hyperinflation and currency devaluation.

Can a country recover from fiscal dominance?

Yes, but it requires “fiscal consolidation”—aggressive spending cuts and tax reforms—often paired with a commitment to a strict, independent monetary framework to regain market trust.

Looking Ahead: The Path to Stability

The current global economic climate suggests that the era of “effortless money” is over. For nations to avoid the trap of fiscal dominance, the solution is not more printing, but more discipline. The only sustainable path forward is a return to rigorous fiscal frameworks where spending is aligned with revenue and central banks are empowered to prioritize price stability over political convenience.

As we move through 2026, the divide between countries that embrace fiscal discipline and those that succumb to monetary mismanagement will likely define the next decade of global market leadership.