{kind=link}

U.S. Shale Output Growth Faces Headwinds as Well Backlog Hits Record Low

The U.S. Shale industry, a critical engine for global energy supply, is facing a significant operational bottleneck. As global demand for crude oil intensifies following the conflict between the United States and Israel against Iran, producers are finding their ability to rapidly scale production constrained by a record-low inventory of drilled-but-uncompleted wells (DUCs).

The DUC Inventory Crisis

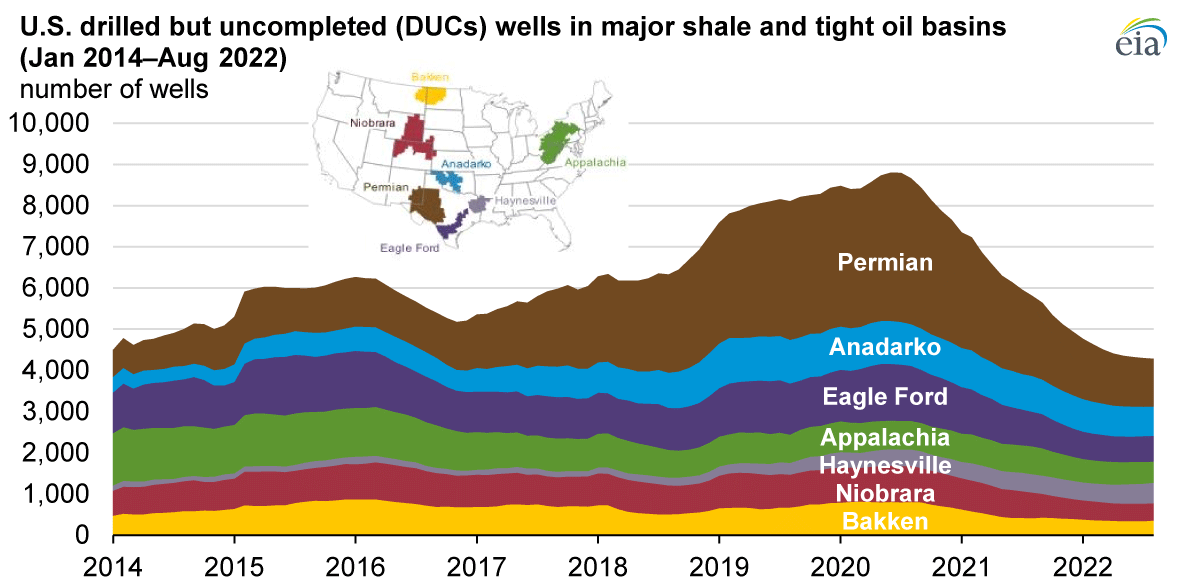

Drilled-but-uncompleted wells serve as the industry’s “buffer.” These wells have already been drilled, meaning they are ready for the final completion phase—a process that typically brings oil to the surface in six to nine weeks. This is significantly faster than the three to nine months required to drill and complete a brand-new well from scratch.

According to the U.S. Energy Information Administration, there were approximately 4,972 DUCs as of April 2026. This figure marks the lowest level in data dating back to 2013, following 14 consecutive months of decline. Analysts note that many of the wells currently counted in this inventory may never be completed, as they were either drilled for geological testing or are no longer economically viable under current conditions.

Market Pressures and Export Surges

The urgency to boost production stems from a shift in global energy flows. Since the conflict began and Iran effectively closed the Strait of Hormuz, Middle Eastern oil supplies have been largely bottled up. In response, U.S. Producers have ramped up exports to Asia and Europe to fill the supply gap.

This export surge, combined with increased refinery processing, has placed significant pressure on U.S. Domestic inventories. Government data indicates that U.S. Crude stockpiles fell by 12.4 million barrels in the week ending May 22, 2026, dropping to 806.8 million barrels—the lowest level since January 2025. Total stocks have declined by 52 million barrels since the onset of the conflict.

Economic Realities of Shale Development

The current depletion of DUCs is a byproduct of the industry’s financial strategy throughout 2025. With oil prices hovering around $65 a barrel last year, operators focused on completing existing wells rather than investing in expensive new drilling projects to conserve capital.

The cost disparity remains a major factor for operators:

- New Well Development: $8 million to $10 million per well.

- DUC Completion: $5 million to $6 million per well.

Linhua Guan, CEO of Surge Energy, one of the largest private producers in the Midland Basin, noted the industry’s shift in strategy: “I anticipate that oil-focused independent operators with meaningful DUC inventories will draw them down at a record pace over the coming months.”

Key Takeaways

- Supply Constraints: The record-low DUC backlog limits the industry’s ability to respond quickly to sudden price spikes or supply shortages.

- Inventory Decline: U.S. Crude stocks are at their lowest point since early 2025, driven by a surge in exports to Europe, and Asia.

- Operational Pivot: While rig counts are beginning to increase and producers are looking to replenish their DUC stocks, the transition from drilling to production remains a time-intensive process.

Looking Ahead

As shale producers move to replenish their DUC inventories, the industry faces a delicate balancing act. While higher oil prices provide the necessary incentive for increased capital expenditure, the lead times inherent in drilling new wells mean that the “quick-turn” production increases the market has grown accustomed to may remain elusive in the near term. Investors and energy analysts will be closely watching rig count data and completion rates in the coming months to determine if producers can effectively navigate this supply-side bottleneck.