{kind=link}

The Financial Reality of Medicare: Understanding Costs and Income Impact

For millions of older adults and individuals with disabilities, Medicare serves as a critical lifeline. However, the financial burden of navigating health care costs in retirement is often more significant than many beneficiaries anticipate. As a physician, I frequently see patients surprised by the out-of-pocket expenses that persist even after securing Medicare coverage. Understanding the intersection of fixed incomes and rising health care costs is essential for effective long-term financial and medical planning.

The True Cost of Medicare Coverage

Medicare is not “free” health care. While Part A (hospital insurance) is premium-free for most people who have paid Medicare taxes for at least 40 quarters, other components of the program—specifically Part B (medical insurance) and Part D (prescription drug coverage)—require monthly premiums. Beyond these premiums, beneficiaries face deductibles, coinsurance, and copayments that can accumulate rapidly.

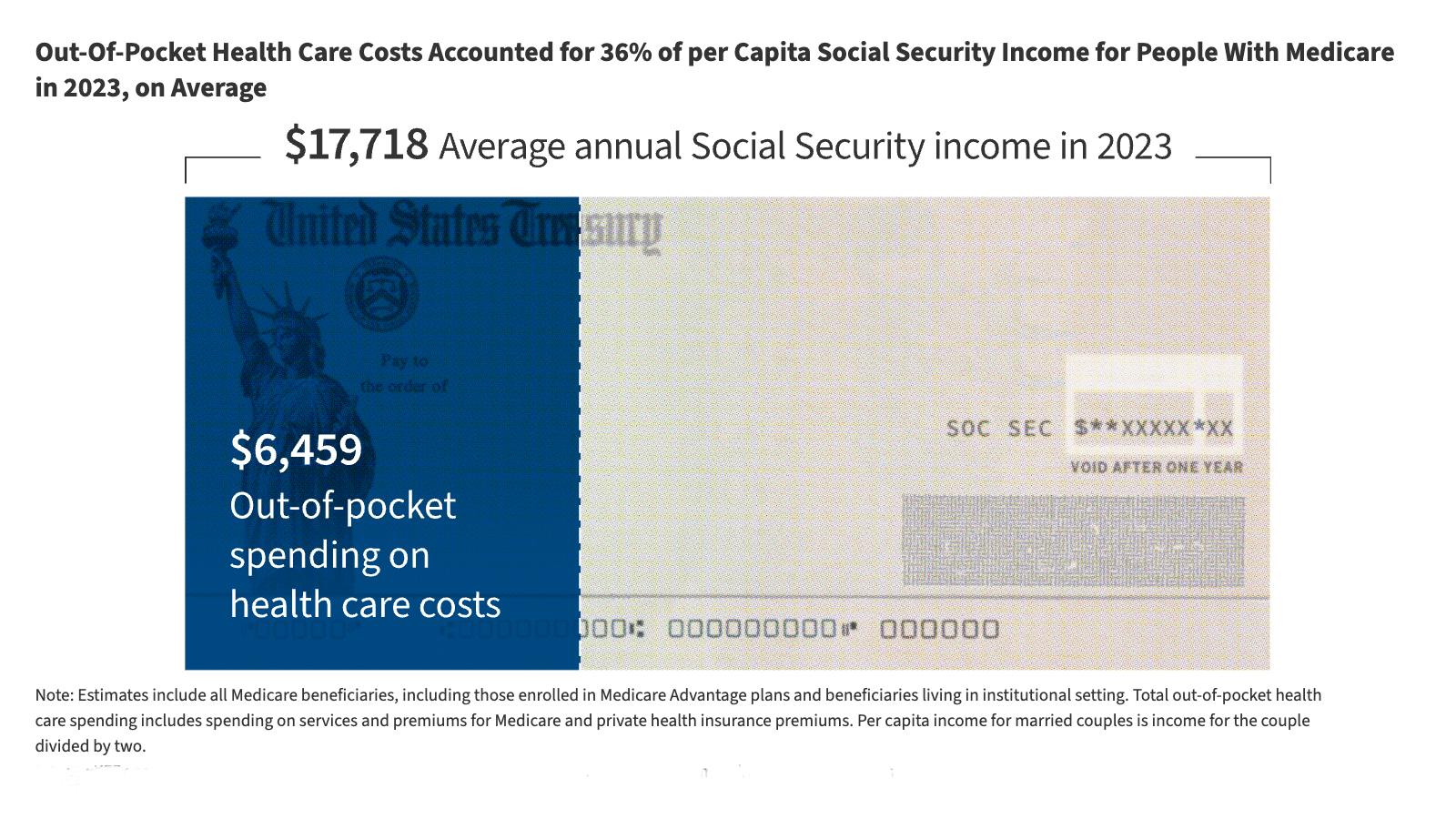

Data from the Medicare Current Beneficiary Survey highlights that out-of-pocket spending remains a substantial portion of a beneficiary’s budget. When you factor in non-covered services—such as routine dental, vision, and hearing care—the financial strain on those with chronic health conditions becomes even more pronounced.

Key Takeaways for Beneficiaries

- Fixed Income Dependency: A significant share of Medicare beneficiaries relies on Social Security for the vast majority of their total income, leaving little room for unexpected medical expenses.

- Premium Burden: Monthly Part B premiums represent a mandatory, non-negotiable deduction from Social Security checks, which impacts the net income available for other living expenses.

- Medigap and Supplemental Insurance: Many beneficiaries purchase Medigap policies to cover the “gaps” in Original Medicare. While these plans provide financial predictability, they add another layer of monthly premiums to a retiree’s budget.

Analyzing the Financial Burden

The financial pressure on Medicare households is distinct from that of non-Medicare households. According to the Bureau of Labor Statistics Consumer Expenditure Survey, households where all members are covered by Medicare often allocate a higher percentage of their total budget to health care compared to younger, working-age households. This is largely due to the combination of age-related health needs and the structure of Medicare cost-sharing.

For those living on a fixed income, even a modest increase in deductibles—as outlined in the Annual Report of the Boards of Trustees of the Federal Hospital Insurance and Federal Supplementary Medical Insurance Trust Funds—can create significant stress. It is crucial to view health care spending not just as an incidental cost, but as a core component of your retirement financial strategy.

Frequently Asked Questions

How can I lower my out-of-pocket Medicare costs?

Many beneficiaries explore Medicare Advantage (Part C) plans, which often bundle Part A, Part B, and sometimes Part D, while providing additional benefits like dental and vision. However, it is important to weigh the lower premiums against potential restrictions in provider networks. Alternatively, maintaining Original Medicare with a Medigap plan offers more flexibility but generally requires higher monthly premiums.

What is the “income-related monthly adjustment amount” (IRMAA)?

If your modified adjusted gross income (MAGI) exceeds certain thresholds, the Social Security Administration will impose an IRMAA surcharge on your Part B and Part D premiums. It is important to review your tax returns annually to understand if you fall into these brackets.

Are there programs for low-income beneficiaries?

Yes. If you have limited income and resources, you may qualify for the Medicare Savings Programs (MSPs), which help pay for Part B premiums, deductibles, and coinsurance. The Extra Help program assists with Medicare Part D prescription drug costs.

Looking Ahead

Navigating the costs of Medicare requires proactive engagement. Whether you are nearing retirement or are already enrolled, I encourage you to regularly review your plan options during the Annual Enrollment Period (October 15 – December 7). By understanding your specific health needs and the financial structure of your coverage, you can better protect your long-term financial health while ensuring you receive the medical care you deserve.

Disclaimer: This article is for informational purposes only and does not constitute financial or medical advice. Always consult with a qualified financial advisor or a Medicare counselor (SHIP) to discuss your personal situation.

Related reading