{kind=link}

<>

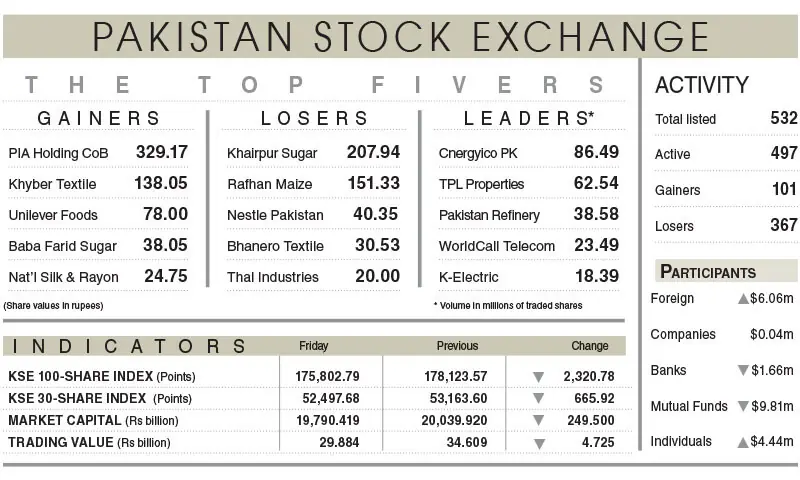

The Pakistan Stock Exchange (PSX) benchmark index retreated by 2,320.78 points, or 1.3 per cent, to close at 175,802.79 on Friday, as renewed geopolitical tensions and rising oil prices triggered a wave of profit-taking. The decline snapped a two-session recovery rally, with investors growing cautious over potential energy supply disruptions in the Strait of Hormuz.

Geopolitical Pressures and Market Sentiment

Escalating tensions between the United States and Iran dominated market sentiment throughout the trading session. According to Topline Securities Ltd, the index faced consistent selling pressure as reports of intensified strikes raised fears of a broader regional conflict. These geopolitical risks directly impact Pakistan’s economic outlook, given the country’s heavy reliance on imported energy.

Ali Najib, Deputy Head of Trading at Arif Habib Ltd, noted that the PSX experienced mixed trading activity. While the market opened higher due to selective buying, momentum shifted in the latter half of the day as investors chose to book gains ahead of the weekend. This cautious approach resulted in a decline in overall market activity, with traded volume dropping 15.73pc to 621 million shares and the total traded value falling 13.65pc to Rs29.8 billion.

Sector-Specific Selling

The market-wide downturn was driven by significant profit-taking in heavyweights across the financial and industrial sectors. Nine major companies—Engro Holdings, Systems Ltd, United Bank, Oil and Gas Development Company, Pakistan Petroleum, Hub Power, Meezan Bank, Habib Bank, and Lucky Cement—collectively accounted for 1,105 points of the index’s decline. Cnergyico PK emerged as the most active stock by volume, recording 86.4 million shares traded.

Macroeconomic Indicators and Growth

Pakistan’s technology sector remains a bright spot, with exports reaching a record $4.6bn, a 21pc year-on-year increase that now represents 46pc of total services exports, according to official data.

However, other indicators show continued pressure on the external account and foreign investment:

- Current Account: The country recorded a current account deficit of $649 million in June, closing the fiscal year with a marginal deficit of $139 million.

- Foreign Direct Investment: Net FDI inflows for the year stood at $1.64bn, representing a 34pc decline compared to the previous year.

- Exchange Rate: The Real Effective Exchange Rate (REER) climbed to 106.44 in June, marking its highest level since September 2018.

Outlook for Investors

Market analysts suggest that while geopolitical developments will likely keep investors on the sidelines in the near term, the ongoing corporate earnings season could provide a floor for the market. Appealing valuations in select sectors remain a primary focus for institutional participants. Investors are expected to continue monitoring the situation in the Middle East closely, as any further disruption to global oil supply chains remains the most significant risk to domestic inflationary targets and equity market stability.

Worth a look