{kind=link}

Medicare Advantage Out-of-Pocket Limits in 2026: Key Insights and Trends

As Medicare beneficiaries navigate their healthcare coverage options, understanding the financial protections offered by Medicare Advantage (MA) plans is critical. While traditional Medicare lacks an out-of-pocket spending cap, Medicare Advantage plans provide a maximum annual limit on out-of-pocket costs, a feature that has sparked ongoing policy debates. This article explores the 2026 landscape of Medicare Advantage out-of-pocket limits, highlighting key differences between plan types, enrollment trends, and historical context.

Medicare Advantage Out-of-Pocket Caps: 2026 Overview

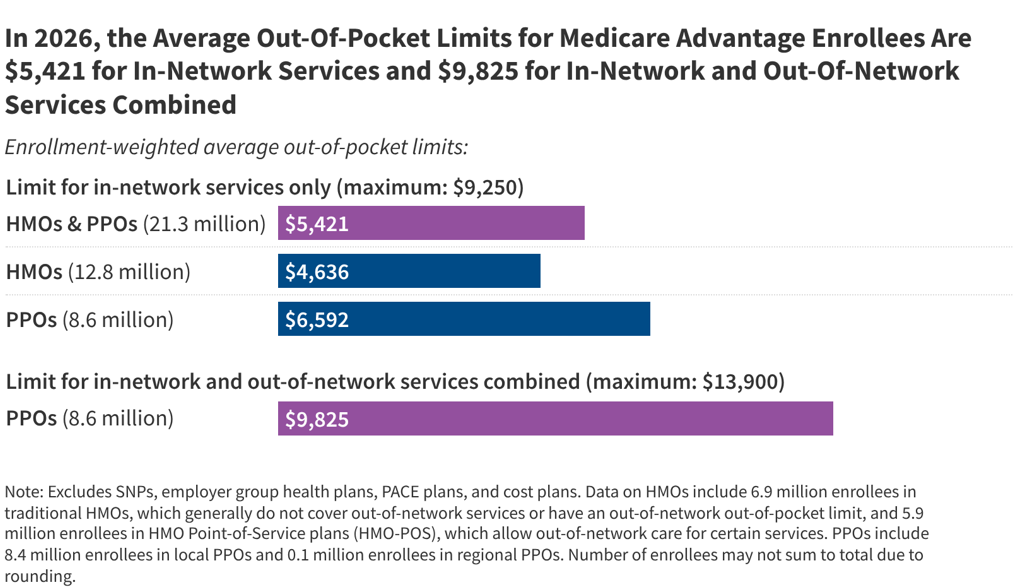

In 2026, the maximum out-of-pocket (OOP) limit for Medicare Advantage plans is set at $9,250 for in-network services and $13,900 for a combination of in-network and out-of-network services. However, these limits are not mandatory; plans may offer lower caps. The average enrollment-weighted OOP limit for in-network services is $5,421, while the combined limit averages $9,825—both below the statutory maximums.

These caps are designed to protect beneficiaries from catastrophic healthcare costs, a stark contrast to traditional Medicare, which does not include such protections. Most traditional Medicare beneficiaries rely on supplemental coverage (e.g., Medigap, Medicaid, or employer-sponsored plans) to offset out-of-pocket expenses.

Plan Type Differences: HMOs vs. PPOs

Medicare Advantage plans fall into two primary categories: Health Maintenance Organizations (HMOs) and Preferred Provider Organizations (PPOs). Their OOP limits reflect distinct trade-offs between cost and flexibility:

- HMOs (12.8 million enrollees in 2026) typically have lower OOP limits. The average in-network cap is $4,636, but they do not cover out-of-network services.

- PPOs (8.6 million enrollees in 2026) offer broader access to out-of-network providers but come with higher OOP limits. The average in-network cap is $6,592, and the combined limit is $9,825.

Rural-urban disparities also exist. Medicare Advantage enrollees in rural areas face an average in-network OOP limit $800 higher than those in urban areas ($6,078 vs. $5,291), partly due to a higher share of PPO enrollment in rural regions.

Enrollment Distribution and Trends

As of 2026, the distribution of enrollees across OOP tiers reveals significant variation:

- 13% (2.8 million) of enrollees are in plans with in-network OOP limits of $3,000 or less.

- 68% (14.4 million) are in plans with limits between $3,000 and $7,000.

- 19% (4.1 million) are in plans with limits exceeding $7,000, including 1.8 million in plans with the maximum $9,250 in-network cap.

For PPOs, 22% (1.8 million) of enrollees face the maximum combined OOP limit of $13,900. These figures underscore the importance of comparing plans based on both cost and coverage flexibility.

Historical Context and Policy Implications

The inclusion of OOP caps in Medicare Advantage is not new. In 1988, Congress temporarily enacted a cap, but it was repealed due to financing concerns. Since then, the Medicare Payment Advisory Commission (MedPAC) has advocated for similar protections in traditional Medicare, including combining Part A and Part B deductibles and simplifying cost-sharing structures.

From 2017 to 2023, average in-network OOP limits decreased by nearly $600, but they rose by $700 between 2023 and 2026. This fluctuation reflects changes in how Medicare Advantage plans allocate federal rebate dollars, which can be used to reduce beneficiary costs or fund additional benefits.

What Beneficiaries Should Know

When choosing a Medicare Advantage plan, beneficiaries should:

- Evaluate OOP limits alongside premiums, network coverage, and supplemental benefits.

- Consider their healthcare needs: HMOs may be cost-effective for those with stable, in-network care, while PPOs offer flexibility for out-of

More on this