{kind=link}

Federal Reserve’s Next Move: How the Upcoming Jobs Report Could Reshape Interest Rates and the Economy

Wall Street is bracing for this week’s May 2026 Nonfarm Payrolls report, a critical data point that could either confirm or challenge the Federal Reserve’s hawkish stance on inflation. Traders, economists, and policymakers are closely watching whether the labor market remains robust enough to justify further rate hikes—or if cooling wage growth signals a pivot toward easing. Here’s what the numbers could mean for your wallet, investments, and the broader economy.

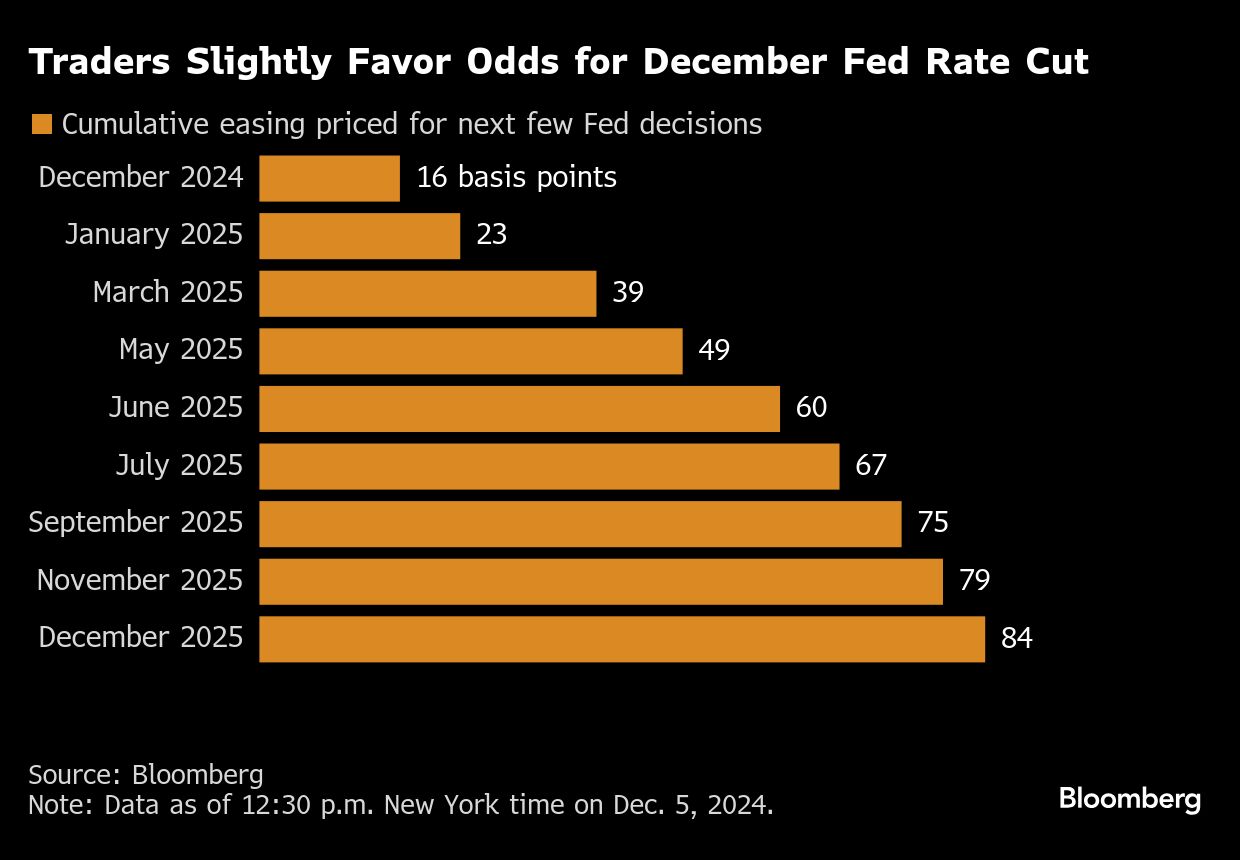

— ### Why This Jobs Report Matters: The Fed’s Dilemma The Federal Reserve has spent the past two years walking a tightrope: keeping inflation in check while avoiding a recession. With the Federal Reserve now signaling a potential pause or even a rate cut later this year, the May jobs report will be the first major test of whether their strategy is working. Key questions on the table: – Is the labor market still overheating? If payrolls grow stronger than expected (consensus forecasts call for around 200,000 new jobs, but some analysts predict 250,000+), the Fed may see it as a sign that demand remains too high. – Are wages cooling? Rising wages can fuel inflation, so if average hourly earnings dip or grow slower than anticipated, it could ease pressure on the Fed to keep rates elevated. – What’s the unemployment rate doing? A drop below 3.9% (the current rate as of April 2026) could reignite fears of an overheating economy. *”The Fed’s next move hinges on whether this report shows a labor market that’s still firing on all cylinders or one that’s finally showing signs of fatigue,”* says Sarah House, Senior Economist at Wells Fargo. *”Right now, the market is pricing in a 60% chance of a rate cut by September—if this jobs number surprises to the upside, that timeline could shift.”* — ### What the Fed Has Said So Far: A Shift Toward Caution In its May 1 meeting, the Federal Open Market Committee (FOMC) struck a more cautious tone, acknowledging that inflation had “eased further” but stressing that “the Committee will continue to assess the implications of incoming data for the economic outlook.” Notably: – Three of the 19 FOMC members now expect at least one rate cut by year-end, up from just one in March. – Chair Jerome Powell has repeatedly emphasized that the Fed’s decision will be “data-dependent,” meaning this jobs report is non-negotiable. *”The bar for cutting rates is higher than it was a year ago,”* Powell told reporters. *”We need to see sustained progress on inflation, and the labor market is a key indicator of whether demand is cooling appropriately.”* — ### How a Strong vs. Weak Jobs Report Could Play Out The market’s reaction will hinge on whether the data aligns with three critical thresholds: | Scenario | Payrolls Growth | Unemployment Rate | Wage Growth (YoY) | Fed’s Likely Response | Market Impact | Overheating Economy | +250,000+ | Drops below 3.9% | 3.8%+ | Hold or hike rates (delay cuts until 2027) | Stocks dip, Treasury yields rise | | Goldilocks Zone | 180,000–220,000 | Holds near 4.0% | 3.5%–3.7% | Pause rates, signal possible cuts later | Mixed reaction; tech stocks may rally | | Cooling Labor Market | Below 150,000 | Rises above 4.1% | Below 3.5% | Cut rates by September | Stocks surge, bond yields fall | *”A ‘Goldilocks’ report—neither too hot nor too cold—would be the sweet spot for the Fed,”* says Gregory Daco, Chief Economist at EY. *”But with inflation still sticky in services, even a moderate jobs number could keep the Fed cautious.”* — ### What This Means for You: Rates, Mortgages, and Investments Whether you’re a homebuyer, investor, or saver, the Fed’s next move will have ripple effects: #### 1. Mortgage Rates: The Wildcard – If the Fed cuts rates, 30-year mortgage rates (currently hovering around 6.5%) could drop to 6.0% or lower by year-end, making homebuying more affordable. – If the Fed holds or hikes, rates may stay elevated, prolonging the housing slump for first-time buyers. *”Every 0.25% change in the Fed’s benchmark rate translates to about $50,000 in mortgage savings over a 30-year loan,”* notes Odeta Kushi, Deputy Chief Economist at First American. *”This report could be the difference between a spring buying frenzy and a summer slowdown.”* #### 2. Stocks: Tech vs. Financials – Tech stocks (especially growth names) tend to rally on rate-cut expectations, as lower borrowing costs boost valuations. – Financials (banks, insurers) may underperform if the Fed signals an imminent pivot, as net interest margins shrink. #### 3. Savings Accounts & CDs: The Catch-22 – High-yield savings accounts and CDs have benefited from elevated rates, but if cuts come, yields could drop back toward 4.0%–4.5% by late 2026. – *”Lock in rates now if you’re parking cash long-term,”* advises Ken Tumin, founder of DepositAccounts. *”The window for 5%+ yields may close sooner than expected.”* — ### FAQ: Your Burning Questions Answered Q: Will this jobs report affect my student loans? A: Federal student loan payments remain paused until at least June 30, 2026, regardless of the Fed’s moves. However, if rates fall, private loan refinancing could become more attractive. Q: Could the Fed cut rates even if the jobs report is strong? A: Unlikely—but not impossible. The Fed has signaled it’s prioritizing inflation over labor market strength. If services inflation (like rent and healthcare costs) stays elevated, they may ignore a hot jobs report. Q: How soon could we see a rate cut? A: Markets are pricing in a 60% chance of a cut by September, but the Fed has repeatedly pushed back against front-running data. A December cut is more likely unless inflation spikes again. Q: What if the jobs report is terrible? A: A weak report (e.g., payrolls below 100,000) could trigger a September cut, but it might also raise recession fears, causing stocks to dip. — ### The Bottom Line: A Pivotal Week for the Economy This week’s jobs report isn’t just another data point—it’s a stress test for the Fed’s credibility. If the labor market remains resilient, the central bank may double down on its fight against inflation, keeping rates higher for longer. But if cracks appear, we could see the first rate cut of 2026 by fall. One thing is certain: the market will react instantly. Whether you’re watching for a buying opportunity in stocks, planning a home purchase, or managing debt, the numbers on Friday will shape your financial strategy for months to come. *”This is the moment where the Fed’s narrative meets reality,”* says House. *”Get ready for volatility—and be prepared to act swift.”* —

Sources: Federal Reserve, Bureau of Labor Statistics (BLS), CME Group FedWatch, Wells Fargo Economics, First American Financial Corporation.

Keep reading