{kind=link}

Protect Your Credit: A Guide to Checking for and Disputing Unauthorized Loans

Your credit report is a crucial financial document, influencing everything from loan approvals to interest rates and even employment opportunities. Regularly checking your credit reports from all three major credit bureaus – Equifax, Experian and TransUnion – is essential to identify and address any inaccuracies, including unauthorized loans opened in your name. This guide provides a comprehensive overview of how to check your credit, dispute fraudulent activity, and protect your financial well-being.

Understanding Credit Reporting Agencies

In the United States, three primary credit bureaus collect and maintain your credit information: TransUnion, Equifax, and Experian. These agencies gather data from various sources, including lenders, creditors, and public records, to compile your credit report. Each bureau operates independently, meaning the information on your reports may vary slightly.

How to Obtain Your Credit Reports

By law, you are entitled to a free credit report from each of the three major credit bureaus annually. You can access these reports through:

- AnnualCreditReport.com: This is the official website authorized by federal law to provide your free annual credit reports. https://www.annualcreditreport.com/

- Directly from the Credit Bureaus: You can request your reports directly from Equifax, Experian, and TransUnion’s websites.

- Through Your Bank or Credit Card Issuer: Some financial institutions offer free credit report access as a benefit to their customers.

Identifying Unauthorized Loans

When reviewing your credit reports, carefully examine the “accounts” section for any loans or credit lines you don’t recognize. Pay close attention to:

- Account Names: Look for lenders you’ve never done business with.

- Account Opening Dates: Check for accounts opened without your knowledge.

- Loan Amounts and Payment History: Verify the accuracy of loan amounts and ensure all payments listed are yours.

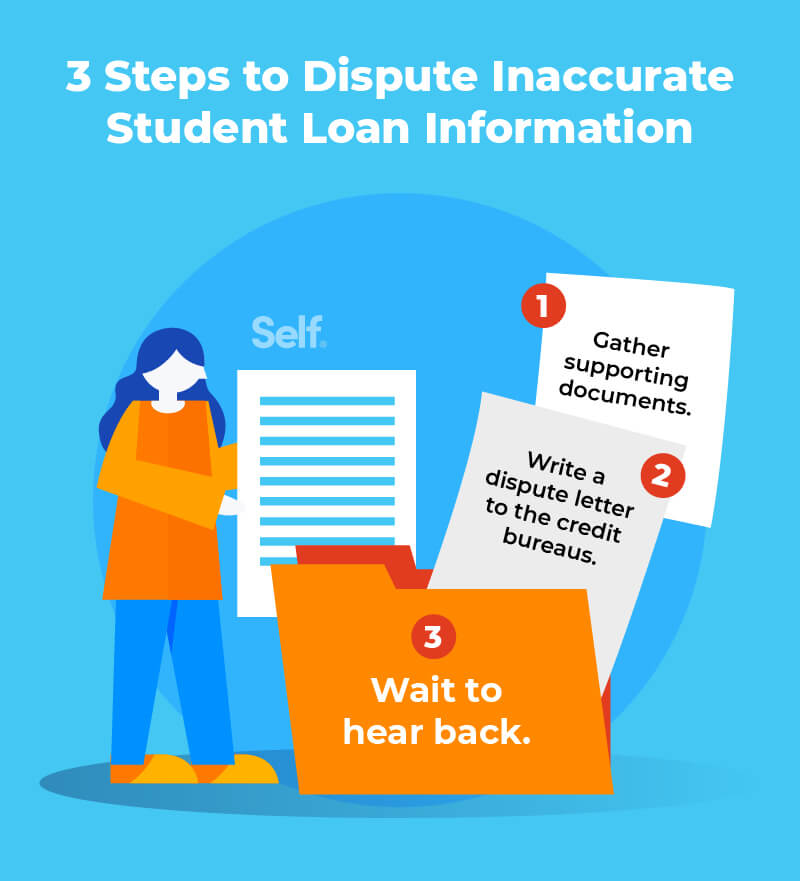

Disputing Unauthorized Loans

If you identify a loan or account that you did not authorize, it’s crucial to dispute it immediately with the credit bureau reporting the information. Each credit bureau has a specific process for filing disputes:

- Equifax: https://www.equifax.com/personal/credit-report-services/

- Experian: https://www.experian.com/disputes/

- TransUnion: https://dispute.transunion.com/

When filing a dispute, provide as much documentation as possible to support your claim, including:

- A copy of your credit report with the disputed item highlighted.

- A detailed explanation of why you believe the loan is fraudulent.

- Any supporting documents, such as a police report (if you’ve filed one) or an affidavit of identity theft.

The credit bureau is required to investigate your dispute within 30 days. They will contact the lender to verify the information. If the lender cannot validate the loan, it must be removed from your credit report.

Protecting Your Credit from Future Fraud

Taking proactive steps can help prevent future instances of credit fraud:

- Credit Monitoring: Consider subscribing to a credit monitoring service that alerts you to changes in your credit report.

- Fraud Alerts: Place a fraud alert on your credit reports, which requires lenders to verify your identity before opening new accounts.

- Credit Locks: A credit lock restricts access to your credit report, making it more difficult for identity thieves to open accounts in your name.

- Secure Your Personal Information: Protect your Social Security number, bank account details, and other sensitive information. Be cautious of phishing scams and shred documents containing personal data.

Key Takeaways

- Regularly check your credit reports from Equifax, Experian, and TransUnion.

- Promptly dispute any unauthorized loans or accounts.

- Take proactive steps to protect your credit from fraud.

Maintaining a vigilant approach to your credit health is essential in today’s digital landscape. By understanding your rights and taking appropriate action, you can safeguard your financial future.

Worth a look