{kind=link}

China Steel Market Update: Domestic Price Trends and Industrial Outlook

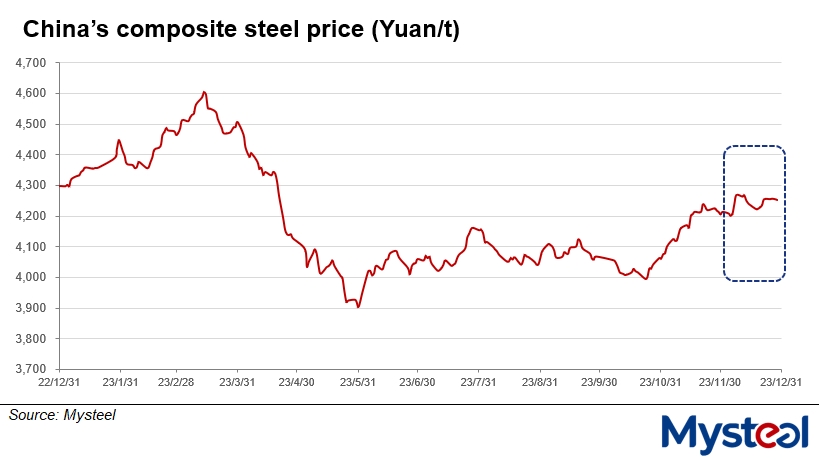

China’s domestic steel prices continue to face downward pressure as of late June 2024, driven by sluggish demand in the property sector and high inventory levels at major mills. According to data tracked by the China Iron and Steel Association (CISA), spot prices for construction-grade rebar and hot-rolled coils have remained volatile, reflecting a broader struggle to balance production capacity with cooling infrastructure investment.

What is driving current steel price fluctuations in China?

The primary driver of price instability is the persistent weakness in China’s real estate market, which historically accounts for roughly one-third of the nation’s steel consumption. Despite various government stimulus measures aimed at property developers, new construction starts remain at historic lows. The National Bureau of Statistics of China reported that investment in property development dropped significantly in the first five months of 2024, directly impacting demand for structural steel. Mills are now caught between the high cost of imported iron ore and a lack of pricing power in the domestic market.

How do domestic prices compare to global benchmarks?

While domestic prices in China have been trending lower, they remain a critical reference point for global commodity markets. Because China produces more than half of the world’s crude steel, its internal price shifts often precede changes in export competitiveness. As noted by S&P Global Commodity Insights, when domestic demand softens, Chinese mills often increase export volumes to clear inventory, which effectively exports deflationary pressure to markets in Southeast Asia and Europe.

Market Comparison: Domestic vs. Export Dynamics

| Factor | Domestic Market Impact | Global Export Impact |

|---|---|---|

| Inventory Levels | High; exerting downward pressure | Increasing; aggressive pricing abroad |

| Property Demand | Weak; recovery remains slow | Neutral; decoupled from local trends |

| Production Costs | Stabilizing due to iron ore prices | Competitive advantage for Chinese mills |

What happens next for the steel industry?

Industry analysts expect production curbs to become a major focus for the second half of 2024. The Chinese government has previously mandated crude steel output caps to meet environmental and carbon-neutrality goals. According to reports from Reuters, if domestic consumption fails to rebound in the third quarter, major steelmakers will likely face increased pressure to reduce output to prevent further price erosion. Investors and stakeholders are watching for the upcoming Third Plenum in July, where potential new fiscal policies could signal a shift in infrastructure spending priorities.

Key Market Takeaways

- Real Estate Lag: The property sector remains the largest hurdle for a domestic price recovery.

- Export Pressure: Excess supply is forcing Chinese mills to seek overseas buyers, impacting global price competitiveness.

- Regulatory Risks: Potential government-mandated production cuts remain the most significant variable for future supply levels.

- Cost Sensitivity: Profit margins for domestic mills remain thin as they navigate the high cost of raw material inputs against soft end-user demand.

The outlook for the remainder of the year depends heavily on whether state-led infrastructure investment can offset the decline in private residential construction. As of late June, market participants remain cautious, prioritizing inventory management over aggressive expansion.