{kind=link}

Strategic College Financing: Navigating Federal Loans and Financial Planning

For many families, the prospect of funding four years of higher education is the most significant financial hurdle they will face. As tuition costs continue to outpace inflation, the reliance on student loans has become a structural reality for millions. However, the stigma surrounding debt often obscures the reality that, when managed strategically, student loans are a financial tool rather than a failure of planning.

Understanding the distinction between federal and private debt, the mechanics of subsidies, and the long-term implications of borrowing is essential for any parent or student aiming to maintain fiscal health while pursuing academic goals.

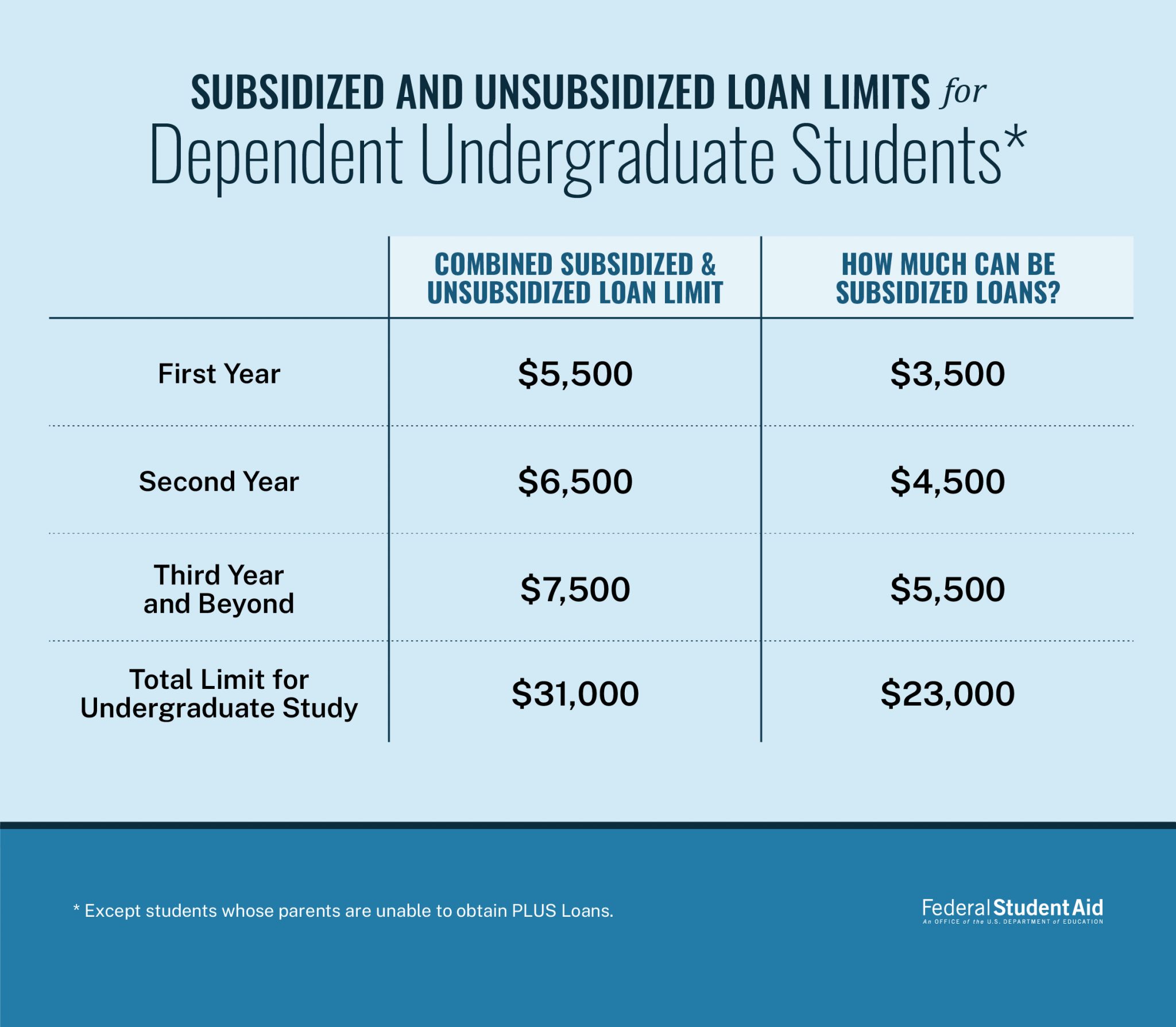

The Role of Federal Subsidized Loans

The cornerstone of responsible college financing is the Direct Subsidized Loan. These are awarded to undergraduate students who demonstrate financial need. The primary advantage of these loans is that the U.S. Department of Education pays the interest while the student is in school at least half-time, for the first six months after leaving school, and during periods of deferment.

By preventing interest from accruing during the undergraduate years, these loans significantly lower the total cost of borrowing compared to unsubsidized alternatives. Because these loans are capped by annual limits and carry fixed interest rates set by Congress, they serve as the most predictable and secure form of educational debt.

Key Takeaways for Families

- Prioritize Federal Aid: Always exhaust subsidized loan options before considering unsubsidized loans or private lending.

- Understand the Cost of Borrowing: Use the Federal Student Aid Loan Simulator to project future monthly payments based on anticipated debt levels.

- Minimize Principal: Even small, consistent contributions toward tuition during the college years can reduce the total principal, thereby decreasing interest accumulation on unsubsidized portions of your debt.

Strategic Financial Planning for College

Effective planning requires a shift from “saving for college” to “managing the investment.” A common misconception is that taking on any debt is inherently negative. In reality, maintaining liquidity—keeping cash available for emergencies or retirement contributions—is often a smarter financial move than liquidating all assets to pay for tuition upfront.

The Hierarchy of Funding

To optimize your financial strategy, approach funding in the following order:

- Scholarships and Grants: These represent “gift aid” and should be your first priority, as they do not require repayment.

- Federal Work-Study: This provides part-time employment to help students earn money for education expenses.

- Federal Subsidized Loans: Used to bridge the gap while benefiting from government interest coverage.

- Federal Unsubsidized Loans: These carry interest from the moment of disbursement.

- Private Loans: These should be viewed as a last resort due to generally higher interest rates and a lack of flexible repayment options like income-driven plans.

Frequently Asked Questions

Is it subpar to take out student loans?

Debt is a financial instrument. If the debt allows a student to graduate in four years and pursue a field with a strong return on investment, it is an investment in human capital. The danger lies in borrowing amounts that exceed the student’s expected starting salary upon graduation.

What is the difference between subsidized and unsubsidized loans?

The core difference is interest accrual. Subsidized loans have their interest paid by the federal government while the student is enrolled. Unsubsidized loans accrue interest immediately, which is then added to the principal balance (capitalized) if not paid during school.

How do I determine how much is “too much” to borrow?

A standard rule of thumb is to keep total student loan debt below the student’s expected first-year salary. If the projected debt significantly exceeds this amount, it is time to reassess the financial plan or explore more affordable academic alternatives.

Conclusion

Navigating the costs of higher education requires a dispassionate, analytical approach. By understanding the nuances of federal loan programs and prioritizing them over higher-cost private alternatives, families can manage the financial burden effectively. Education remains one of the most reliable drivers of long-term economic mobility; when approached with a clear strategy, the use of loans is simply a tactical decision in a larger, lifelong financial plan.

Worth a look