{kind=link}

Medical credit cards often feature deferred-interest promotions that can lead to significant financial penalties if balances aren’t paid in full by the end of the promotional period. According to the Consumer Financial Protection Bureau (CFPB), these products differ from standard credit cards because interest accrues from the date of the initial purchase and is retroactively applied to the entire original balance if any portion remains unpaid at the promotional deadline.

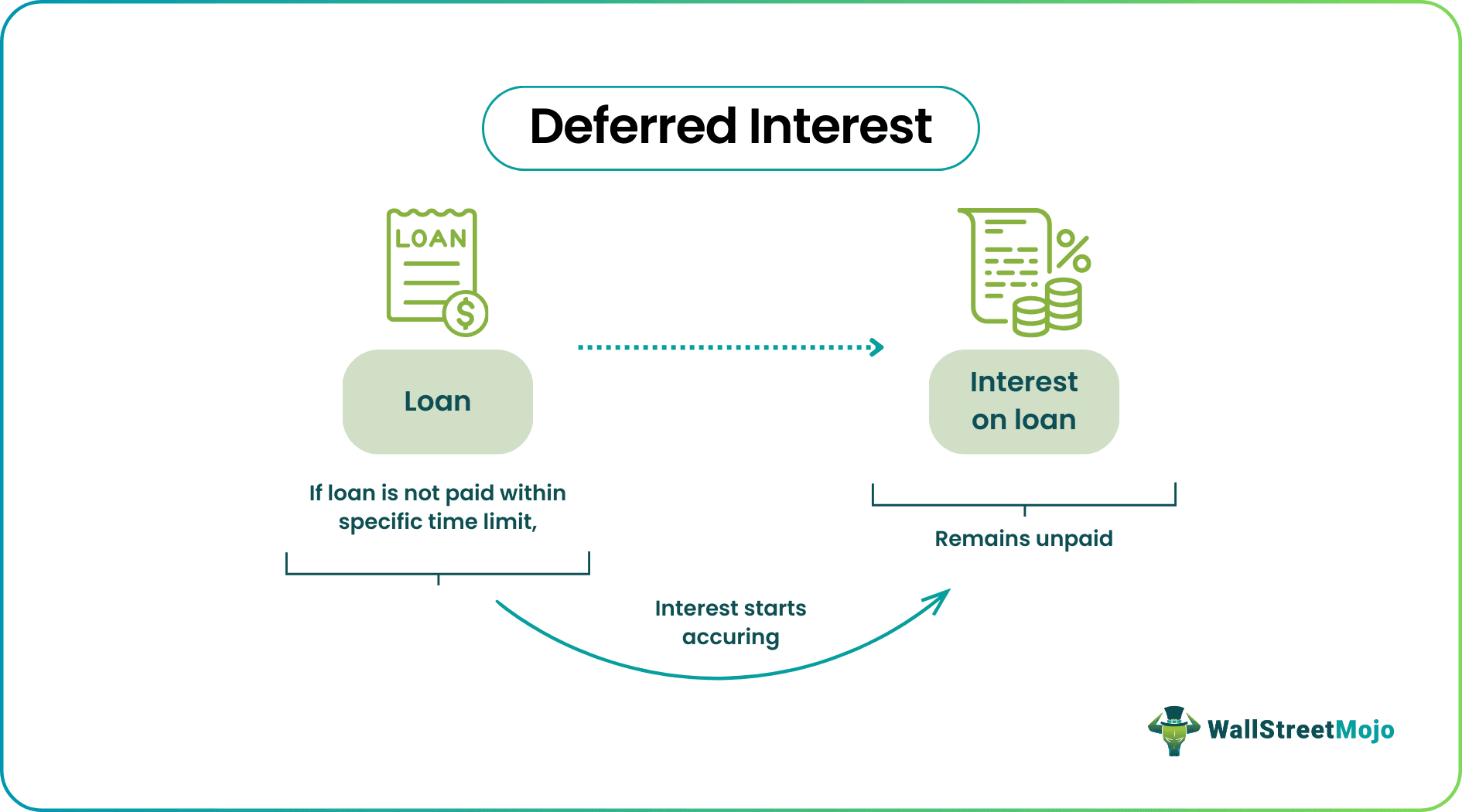

How Deferred-Interest Mechanisms Function

Unlike standard credit cards, where interest is charged only on the remaining balance, medical credit cards often utilize a "deferred-interest" structure. The CFPB warns that consumers frequently misunderstand this distinction. If a patient fails to pay off the full amount within the agreed-upon window—which typically ranges from 6 to 24 months—the lender applies interest charges for the entire duration of the loan. This can result in an effective annual percentage rate (APR) that significantly exceeds the advertised rates of traditional personal loans or standard credit cards.

Financial Risks for Patients

The CFPB report highlights that medical credit cards are frequently marketed within healthcare settings, such as dentists’ offices or elective surgery clinics, at the point of care. Patients in urgent need of treatment may feel pressured to accept these financing options without fully reviewing the complex terms.

According to data from the Federal Reserve, unexpected medical expenses remain a primary driver of household debt. When medical credit cards are used for large procedures, a failure to meet the strict repayment terms can lead to a "interest trap," where the balance grows rapidly despite consistent monthly payments, because those payments are first applied to fees or interest rather than the principal.

Comparison of Medical Financing Options

| Feature | Medical Credit Cards | Personal Loans |

|---|---|---|

| Interest Type | Deferred (retroactive if unpaid) | Fixed or Variable |

| Repayment | Often requires full payoff by deadline | Structured monthly installments |

| Application | Often at point-of-care | Financial institution or online lender |

| Penalty Risk | High (accrued interest applied) | Low (late fees/credit impact) |

Guidance for Consumers

Financial regulators and consumer advocates suggest that patients should explore alternatives before signing up for specialized medical credit cards.

- Request an Itemized Estimate: Before accepting financing, confirm the total cost of the procedure and the specific interest terms.

- Compare APRs: Check if a standard low-interest credit card or a personal loan from a credit union offers a lower total cost of borrowing.

- Inquire About Payment Plans: Many hospitals and clinics offer internal, interest-free payment plans that do not involve third-party lenders or deferred-interest clauses.

- Review the Agreement: If a medical credit card is the only option, verify the exact end date of the promotional period and calculate the required monthly payment to clear the balance before that date.

The CFPB continues to monitor the medical payment product market, noting that the combination of high-pressure sales environments and complex deferred-interest triggers poses a persistent risk to consumer financial health. Patients should treat these cards as high-risk financial instruments rather than standard payment methods.

Worth a look