{kind=link}

Retiring comfortably in the United States requires a highly variable nest egg, with estimates ranging from hundreds of thousands to over a million dollars depending on geography and lifestyle. According to data from Investopedia, the total savings required for a typical couple varies significantly by state, driven primarily by cost-of-living differences, local tax structures, and housing expenses.

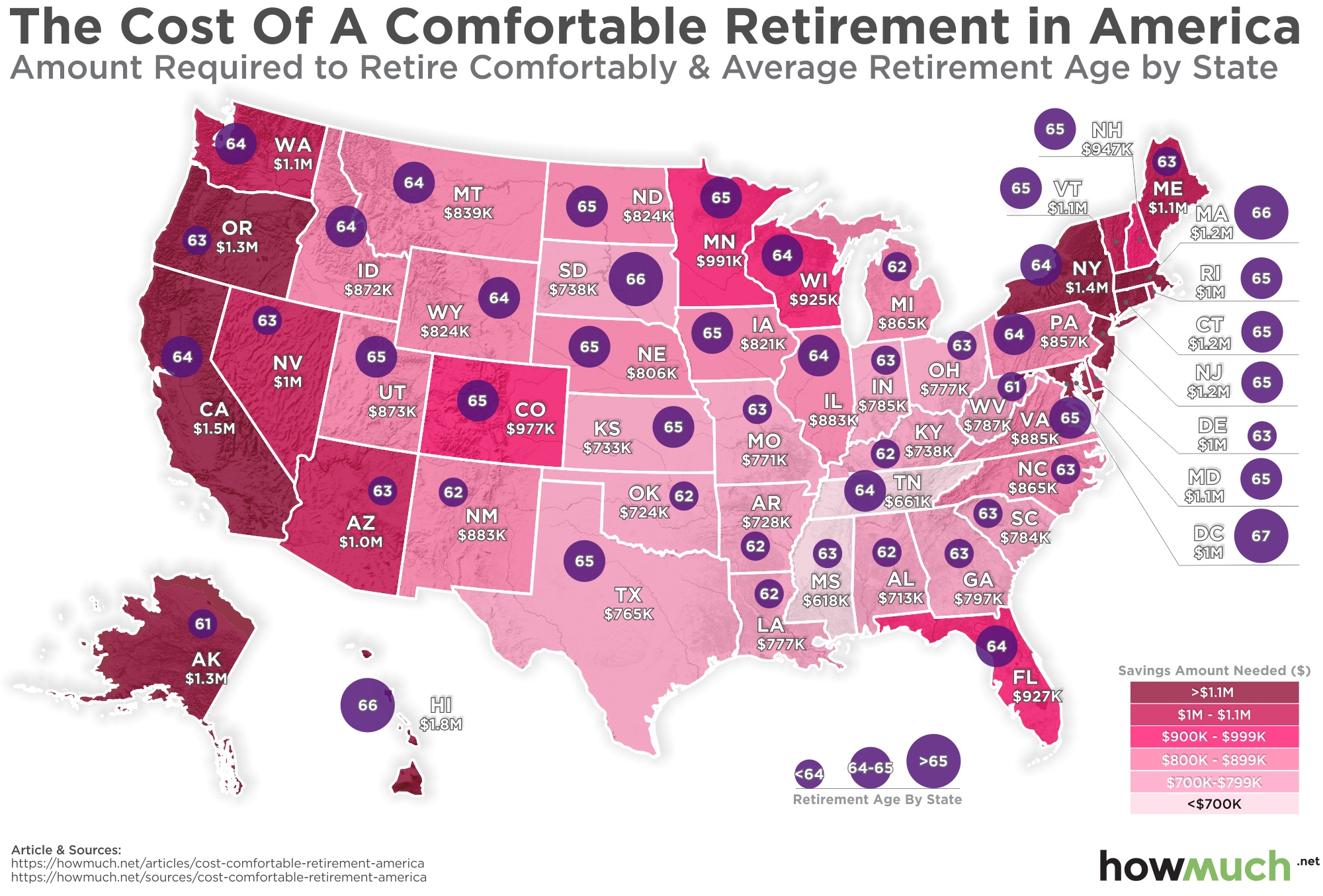

The Geography of Retirement Costs

The "magic number" for retirement is rarely universal. Analysis of state-by-state data shows that residents in high-cost areas like New York, California, and Hawaii face substantially higher thresholds than those in states like Mississippi or Oklahoma.

For instance, Investopedia’s state-by-state analysis highlights that the annual cost of living for retirees can swing by tens of thousands of dollars per year based solely on your ZIP code. When projecting these costs over a standard 20-to-25-year retirement horizon, the cumulative difference in required savings can exceed half a million dollars.

Arizona: A Case Study in Localized Expenses

Retirement planning often focuses on state-level averages, but 24/7 Wall St. notes that internal state variance is just as critical. In Arizona, for example, the cost of living fluctuates sharply between metropolitan hubs and rural areas.

While state-wide averages provide a baseline, financial planners suggest that retirees look at specific municipal data—such as property taxes, utility costs, and local healthcare availability—before finalizing a retirement budget. According to reporting from The Arizona Republic, the specific target for a comfortable retirement in Arizona often requires a savings goal that accounts for the state’s unique tax treatment of pension income and Social Security, which can influence how much of your nest egg you actually need to withdraw annually.

Factors Influencing Your Personal Target

Beyond geography, your personal retirement number is tethered to three primary variables:

- Housing Costs: Whether you own your home outright or carry a mortgage is the single largest determinant of your monthly cash flow requirements.

- Healthcare Inflation: As noted by The Daily Upside, medical expenses typically rise faster than the general Consumer Price Index (CPI), making healthcare the most volatile line item in a long-term budget.

- Tax Efficiency: States with no income tax or favorable treatment of retirement distributions—such as Florida, Texas, or Nevada—can lower the total nest egg required compared to states with heavy tax burdens on fixed income.

Evaluating Your Retirement Readiness

To determine your personal number, financial experts often suggest a "reverse-budgeting" approach. Instead of aiming for a round million-dollar figure, calculate your essential annual expenses and subtract your guaranteed income sources, such as Social Security and any defined-benefit pensions.

The resulting "gap" is the amount your portfolio must generate. By applying a common, though debated, guideline suggesting you can safely withdraw a small percentage of your portfolio in the first year of retirement—you can estimate the total nest egg required to sustain that gap.

As you plan for the future, prioritize your specific location’s cost-of-living data over national averages. Given the current economic climate, building a buffer for unexpected inflation and rising healthcare costs remains a standard recommendation for ensuring long-term financial security.