{kind=link}

Managing Your Insurance Through Online Banking: A Streamlined Approach to Financial Oversight

For the modern consumer, the fragmentation of financial services is a persistent pain point. Managing a checking account in one portal, a savings account in another, and insurance policies across three different provider websites is inefficient. This is why the integration of insurance management into online banking—a model known in the industry as Bancassurance—has become a cornerstone of the fintech evolution.

By consolidating insurance products within a primary banking dashboard, users can move from passive policy ownership to active financial management. Whether you are handling life, health, or property insurance, the ability to access these documents using your existing banking credentials simplifies the user experience and enhances oversight.

How to Access Insurance Products via Your Banking Portal

While every financial institution has a slightly different interface, the workflow for accessing integrated insurance services is generally standardized to ensure ease of use. If your bank offers insurance integration, the process typically follows these steps:

- Navigate to the Product Menu: Once logged into your secure online banking environment, look for a tab labeled “Products,” “Services,” or “My Portfolio.”

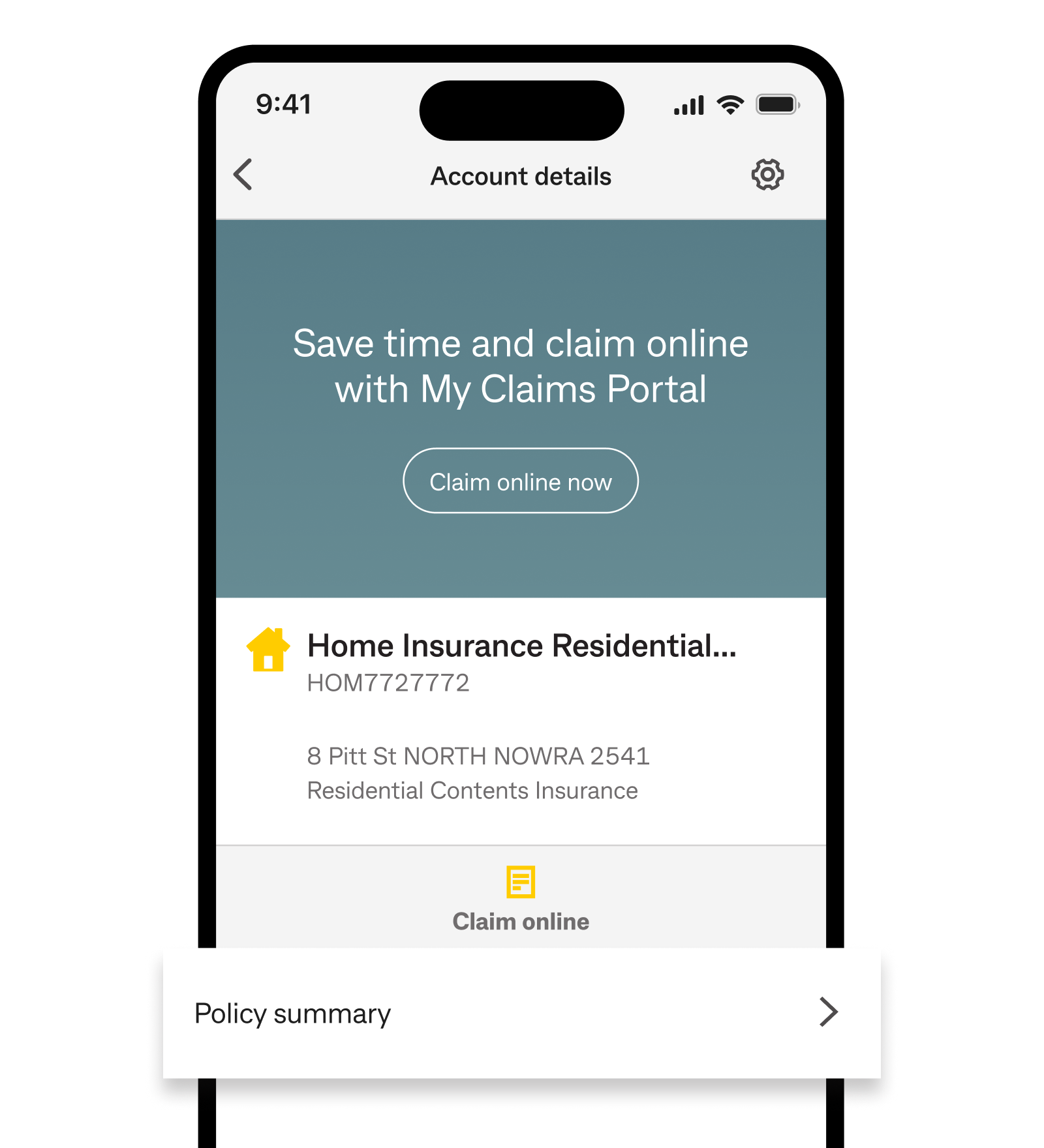

- Select the Insurance Category: Within the product menu, select the “Insurance” (or Versicherung in German portals) option. This filters your view to only show active policies and available coverage options.

- Authentication: In most integrated systems, you do not need a separate password. You use your primary banking user ID and account number to authenticate your identity, ensuring that your sensitive policy data is protected by the same high-level security as your bank accounts.

- Manage Your Policy: Once inside the insurance module, you can typically view policy documents, update beneficiary information, or initiate claims.

The Strategic Value of Bancassurance

The trend of banks offering insurance isn’t just about convenience; it’s a strategic shift in how financial services are delivered. For the consumer, this integration provides several distinct advantages:

Centralized Documentation

One of the biggest challenges in insurance is the “paper trail.” By hosting policies within a banking portal, you eliminate the need to search through emails or physical files for policy numbers and terms of service. Everything is digitized and accessible in one location.

Simplified Payment Tracking

Because the insurance is linked to your bank account, premium payments are more transparent. You can track exactly when a premium was debited and set up automated alerts to ensure your coverage never lapses due to an overlooked payment.

Holistic Financial Planning

When your insurance data sits alongside your assets and liabilities, it’s easier to assess your overall risk profile. For example, seeing your home equity next to your homeowners’ insurance policy allows you to determine if you are under-insured based on current market values.

Security and Privacy in Digital Insurance Management

Given that insurance policies contain highly sensitive personal and medical information, security is paramount. Professional banking portals employ several layers of protection to safeguard this data:

- Multi-Factor Authentication (MFA): Most portals require a second form of verification (such as a biometric scan or a timed code) before granting access to insurance details.

- End-to-End Encryption: Data transmitted between the insurance provider and the banking interface is encrypted to prevent interception.

- Role-Based Access: Even within a joint account, banks often implement controls to ensure that only authorized individuals can modify specific policy details.

Key Takeaways for Policyholders

- Efficiency: Use your existing banking credentials to avoid managing multiple passwords for different insurance providers.

- Visibility: Integrated portals allow for a “single pane of glass” view of your financial health, combining assets with protection.

- Security: Ensure your banking app is updated to the latest version to take advantage of the most recent security patches for your integrated services.

Frequently Asked Questions

Do I need a separate account for insurance if it’s in my banking app?

Generally, no. The banking portal acts as the interface (the “front end”), while the insurance company manages the policy (the “back end”). Your banking ID serves as the key to access both.

Can I buy new insurance policies directly through my bank?

Yes, most banks that offer insurance integration also provide a marketplace where you can compare quotes and purchase new policies directly through the app, often with streamlined underwriting because the bank already has your verified financial data.

Is my data shared between the bank and the insurance company?

Yes, but this is governed by strict data-sharing agreements and privacy laws. The bank shares necessary identity and financial verification data with the insurer to facilitate the policy, while the insurer shares policy status and billing data with the bank.

Looking Ahead: The Future of Integrated Finance

As we move further into the era of Open Banking, we can expect these integrations to become even more seamless. The next step is the move toward “hyper-personalized” insurance, where your banking patterns—such as spending on home improvements—could trigger automatic suggestions to increase your property coverage in real-time. For the proactive investor and homeowner, embracing these integrated tools is the most efficient way to ensure comprehensive protection in a digital world.