{kind=link}

Managing a $7 Million Portfolio Without Traditional Asset Management Fees

Retirees with $7 million in assets can effectively manage their wealth without paying traditional AUM (assets under management) fees, which typically range from 0.5% to 1%. By utilizing a combination of flat-fee financial planners, automated investment platforms, and self-directed tax-efficient strategies, high-net-worth individuals can secure professional guidance while retaining a larger portion of their annual returns.

The Cost of Traditional Wealth Management

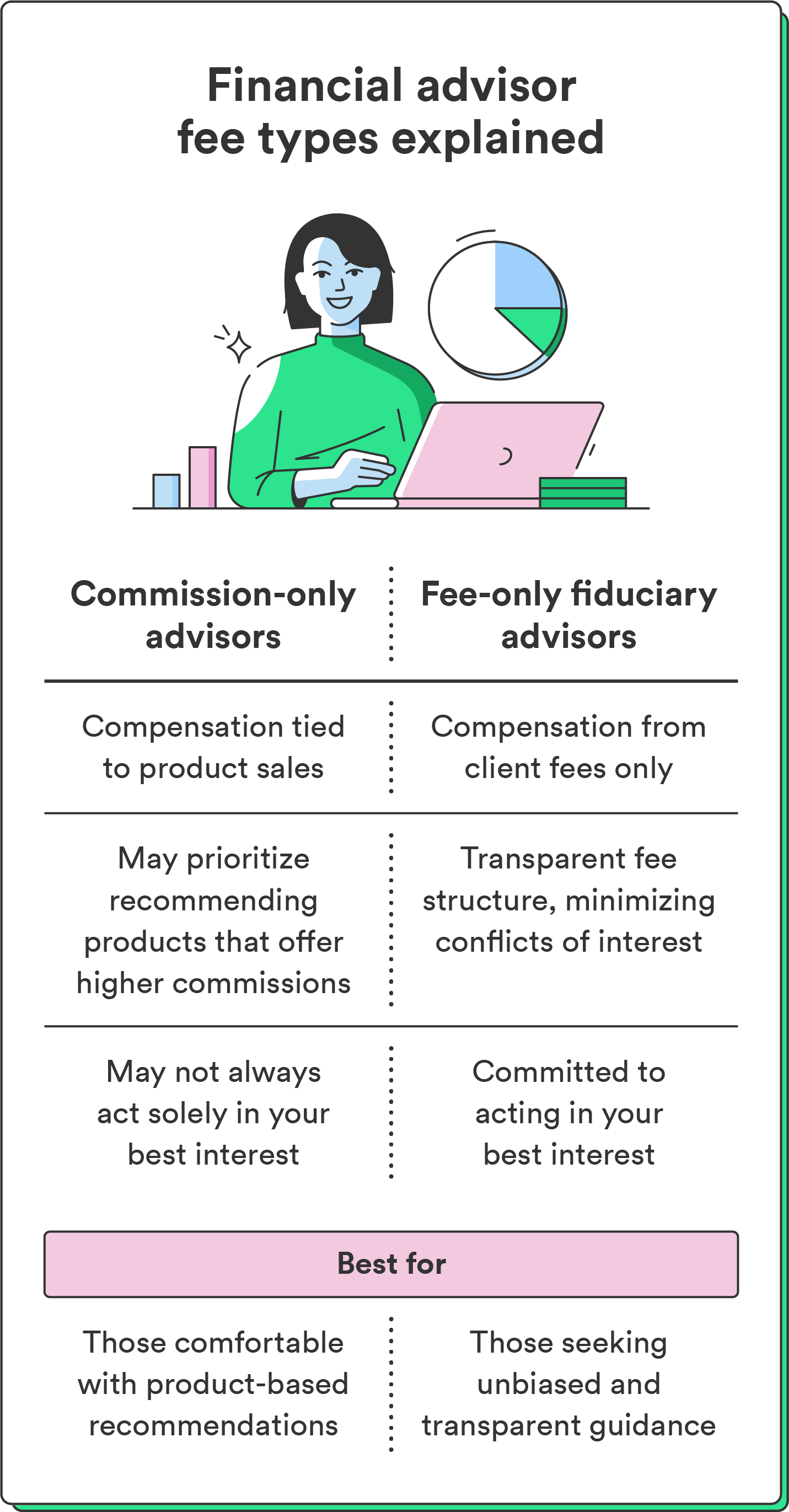

For an investor with $7 million, a standard 1% management fee equates to $70,000 in annual costs. According to the [Securities and Exchange Commission (SEC)](https://www.investor.gov/introduction-investing/investing-basics/glossary/investment-adviser), investment advisers must act as fiduciaries, but the fee structure often remains tied to the total account balance regardless of the complexity of the services rendered.

Investors seeking to avoid these percentage-based fees often pivot toward “fee-only” advisors. Unlike commission-based brokers, fee-only planners charge a flat hourly rate or a fixed annual retainer. This model decouples the cost of advice from the size of the portfolio, ensuring the client pays only for the time and expertise utilized rather than a percentage of their life savings.

Strategic Alternatives for Portfolio Oversight

High-net-worth retirees have several institutional-grade options that bypass the traditional percentage-based model:

* Flat-Fee Financial Planners: These professionals provide comprehensive financial planning, estate strategy, and tax optimization for a set fee. Organizations like the [National Association of Personal Financial Advisors (NAPFA)](https://www.napfa.org/) maintain directories of advisers who operate on a fee-only basis, explicitly excluding commissions and AUM-based pricing.

* Low-Cost Automated Investing: For the investment portion of a portfolio, many retirees utilize “robo-advisors” or direct-to-fund strategies. By holding low-cost index funds from providers like Vanguard, BlackRock, or Fidelity, investors can achieve broad market exposure with expense ratios often below 0.10%.

* Tax-Efficient Direct Indexing: Some investors utilize direct indexing, where they own the underlying stocks of an index rather than a fund. This allows for systematic tax-loss harvesting, which can offset capital gains and improve after-tax returns—a service that high-end software platforms now provide for a fraction of the cost of a traditional wealth manager.

Balancing Professional Help with Self-Direction

When managing $7 million, the primary challenge is not just investment selection, but tax and estate coordination. According to the [Internal Revenue Service (IRS)](https://www.irs.gov/businesses/small-businesses-self-employed/estate-tax), complex estate planning requires specialized legal and tax expertise that goes beyond basic investment management.

Many retirees find success by hiring a CPA or a tax attorney on a per-project basis to handle specific, high-stakes tasks, such as Roth conversions or trust structuring. This “unbundled” approach allows the retiree to maintain control over their core investment portfolio while bringing in expensive, specialized talent only when the complexity warrants it.

Key Considerations for Independent Wealth Management

| Strategy | Cost Structure | Primary Benefit |

| :— | :— | :— |

| Fee-Only Planner | Hourly or Flat Retainer | Objective, fiduciary advice without conflict of interest. |

| Index Fund Portfolio | Expense Ratio (<0.10%) | Market-matching returns with minimal oversight. |

| Direct Indexing | Software Subscription | Enhanced tax-loss harvesting and cost savings. |

| Project-Based CPA | Hourly/Flat Fee | Expert handling of specific tax or legal milestones. |

Moving Forward

Retirees who choose to manage their own portfolios must remain diligent regarding rebalancing and tax-bracket management. While moving away from a 1% AUM fee can save tens of thousands of dollars annually, it requires the investor to take an active role in monitoring their asset allocation. For those with $7 million in liquid assets, the most sustainable path often involves a hybrid model: using low-cost, automated investment vehicles for the bulk of the portfolio, while retaining a flat-fee professional for periodic, high-level strategic check-ins.

Related reading