{kind=link}

Strategic Debt Management: Optimizing Loans Through Refinancing and Term Extension

For business owners and investors, the cost of capital is a primary lever for growth. When interest rates shift or cash flow tightens, the ability to restructure existing debt can mean the difference between stagnation and scalability. Two of the most effective tools for managing this are private refinancing and the strategic extension of repayment terms.

- Private Refinancing: Replacing existing loans with new ones to capture lower interest rates, reducing the overall cost of debt.

- Term Extension: Increasing the repayment window (e.g., to 20–25 years) to lower mandatory monthly payments and improve immediate liquidity.

- The Trade-off: While longer terms reduce monthly overhead, they typically increase the total interest paid over the life of the loan.

The Mechanics of Private Refinancing

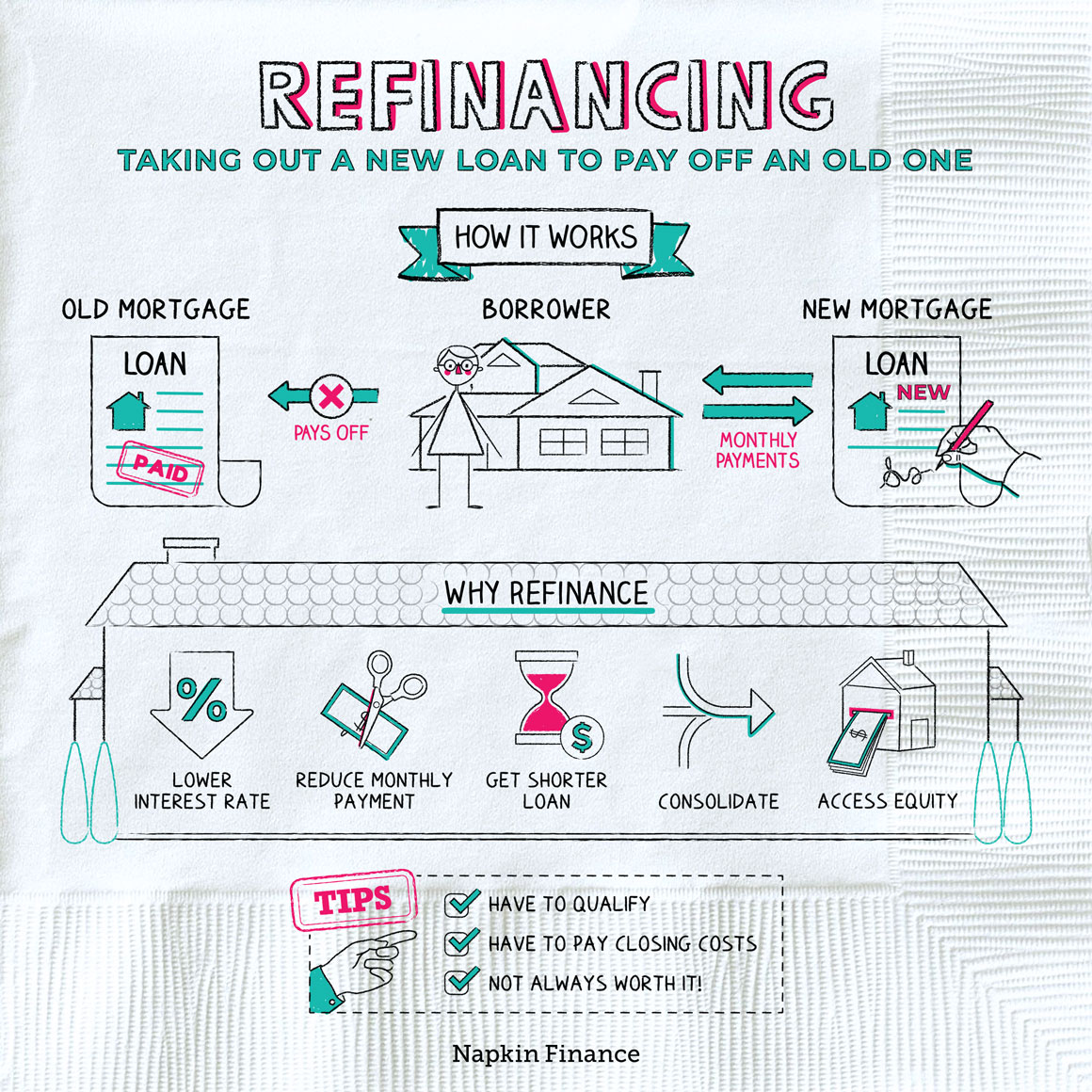

Refinancing is the process of taking out a new loan to pay off an existing one. This is typically pursued when market conditions improve—specifically when interest rates drop—allowing the borrower to secure a more favorable rate than the one attached to their original contract.

When to Pursue Refinancing

The decision to refinance shouldn’t be based on a slight dip in rates alone. Savvy borrowers calculate the “break-even point,” which is the moment the monthly savings from the lower rate offset the closing costs associated with the new loan. According to the Consumer Financial Protection Bureau (CFPB), borrowers should carefully review closing costs and potential prepayment penalties on their current loans before committing to a new agreement.

Benefits of Private Refinancing

- Reduced Interest Expense: Lowering the percentage rate directly reduces the amount of capital lost to interest.

- Improved Debt-to-Income Ratio: Lower payments can improve a company’s balance sheet, making it easier to secure future financing.

- Consolidation: Refinancing often allows borrowers to collapse multiple high-interest loans into a single, more manageable payment.

Leveraging Longer Repayment Terms

While refinancing focuses on the cost of the money, adjusting the repayment term focuses on the timing of the cash flow. Switching to a longer repayment term—such as 20 to 25 years—is a strategic move to lower mandatory monthly payments.

Improving Monthly Cash Flow

By spreading the principal balance over a longer duration, the mandatory monthly obligation decreases. This is particularly useful for businesses in growth phases that need to redirect capital toward operations, hiring, or R&D rather than debt service.

The Cost of Liquidity: The Interest Trade-off

It is critical to understand that extending a loan term is not a “free” reduction in cost. While the monthly payment drops, the total interest paid over the life of the loan increases because the principal is being paid down more slowly. This creates a tension between immediate liquidity and long-term cost.

| Strategy | Primary Benefit | Primary Risk/Downside |

|---|---|---|

| Refinancing | Lower overall interest cost | Upfront closing costs |

| Term Extension | Increased monthly cash flow | Higher total lifetime interest |

Final Strategic Considerations

Before restructuring debt, borrowers must evaluate their long-term exit strategy. If a business expects a significant liquidity event in the next few years, a longer term may be unnecessary. However, for those seeking stability and operational breathing room, the combination of a lower rate and a 20–25 year term provides a powerful hedge against volatility.

debt management is about aligning your repayment structure with your business’s growth trajectory. By monitoring rate trends and adjusting terms proactively, entrepreneurs can ensure their debt serves as a tool for leverage rather than a burden on operations.