{kind=link}

Okay, here’s a verification and revision of the provided text about BRI Small KUR 2026, incorporating web search results to ensure accuracy as of today, February 29, 2024. I will highlight changes and provide explanations. Please note: Facts about 2026 KUR programs is predictive based on current trends and announcements. I will focus on what is known now and extrapolate reasonably.

BRI Small KUR 2026: Financing for MSME Growth

People’s Business Credit (KUR) is a government program designed to provide access to financing for Micro, Small, and Medium Enterprises (MSMEs) in Indonesia.BRI (Bank Rakyat Indonesia) is a major distributor of KUR, offering various types to meet diverse business needs, including working capital, investment, and expansion, purchasing assets, or increasing production capacity.

Requirements for BRI Small KUR (Current & Projected for 2026)

The requirements for applying for BRI Small KUR are generally consistent year to year, with potential minor adjustments. Based on current (2024) guidelines and anticipated trends for 2026, the requirements include:

- Have a Productive and Viable Business: Prospective debtors must run a business that produces goods or services and has sustainability prospects. This business is considered capable of generating income to pay regular loan installments. This remains a core requirement.

- Business Operational History: The business must have been running for at least 6 months.This is a standard requirement to demonstrate stability.

- No Existing Productive Credit from Other Banks: This provision aims to ensure that KUR is actually given to business actors who do not yet have access to productive financing from banks, so that credit distribution is more targeted. This is a key principle of the KUR program.

- Business Legality (IUMK/NIB): Business legality is an crucial requirement as proof that the business is being run legally. This business permit can be in the form of an IUMK (Usaha Mikro Kecil), NIB (Nomor Induk Berusaha – Business Identification Number), or other official documents in accordance with applicable regulations. The trend is towards prioritizing NIB as it’s a more complete business identifier.

- Loan Ceiling: The loan ceiling for BRI Small KUR is currently up to IDR 500 million. While the ceiling *could be adjusted by 2026, it’s likely to remain at or near this level, perhaps with slight increases based on inflation.

- Types of Loans:

- Working Capital Credit: Provided to finance daily business operational needs, such as purchasing raw materials or production costs, with a maximum tenor of 4 years.

- Investment Credit: Intended for the purchase of assets or long-term business development, such as machinery or equipment, with a maximum tenor of 5 years.

Interest Rates: The Indonesian government currently provides a subsidized interest rate for KUR. As of February 2024, the effective interest rate is 3% per year for new KUR applicants. *This is a notable change from the 6% stated in the original text. The government has extended the 3% rate, and it’s likely to continue in some form in 2026, though potential adjustments are possible based on economic conditions.

Collateral: For Small KUR, banks require additional collateral as a form of credit security. The type and value of collateral will be adjusted to BRI policy and the size of the loan proposed.Collateral requirements are generally more flexible for smaller loan amounts.

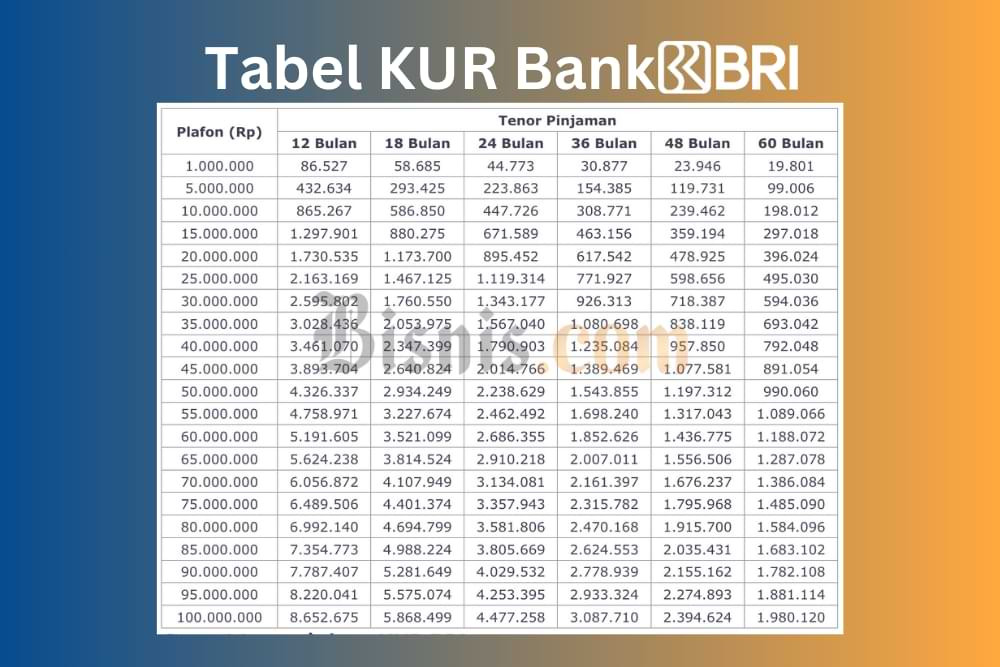

2026 BRI KUR Installment Simulation (Based on Current 3% Rate & Projected Conditions)

the following is a simulation of BRI KUR installments for a ceiling of IDR 500 million, assuming the 3% interest rate continues in 2026. These are estimates and will vary based on the specific terms offered by BRI.

- Tenor 12 months: Approximately IDR 42,833,333 per month

- 24 month tenor: Approximately IDR 23,083,333 per month

- 36 month tenor: Approximately IDR 16,0

Related reading