{kind=link}

Northeast Natural Gas Market Faces Infrastructure Constraints Amid Reawakening Demand

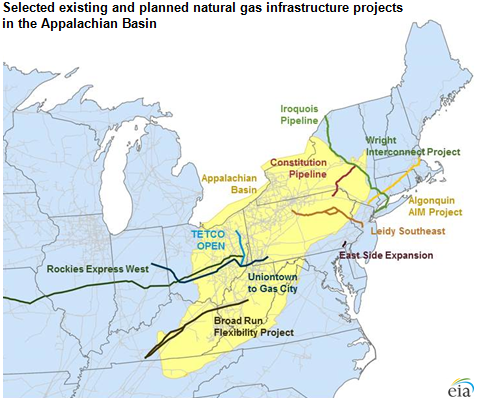

The Northeast natural gas market is experiencing a period of renewed activity as regional developers push for expanded pipeline connectivity to address long-standing capacity constraints. Despite rising demand for power generation and residential heating, developers face significant regulatory hurdles and legal challenges that have stalled major projects, according to data from the U.S. Energy Information Administration (EIA).

Why Is Northeast Pipeline Connectivity Stalled?

Pipeline expansion in the Northeast has slowed due to a combination of environmental litigation and stringent state-level permitting processes. Major projects, such as the Mountain Valley Pipeline, have faced years of delays rooted in disputes over water quality certifications and federal land use, as noted in reports from the Federal Energy Regulatory Commission (FERC).

While producers in the Marcellus and Utica shale plays maintain high output levels, the infrastructure to transport this supply to coastal markets remains limited. Analysts from S&P Global Commodity Insights observe that this “bottleneck” creates a persistent price disparity, where regional gas prices often trade at a significant discount compared to national benchmarks like Henry Hub.

How Do Regulatory Hurdles Impact Regional Energy Prices?

The lack of takeaway capacity means that regional producers cannot easily move excess supply to high-demand areas during peak winter months. When pipeline space is fully booked, local markets must rely on liquefied natural gas (LNG) imports or gas transported from other regions, which frequently drives up consumer costs.

According to the EIA’s latest regional analysis, the interplay between state environmental policies and federal infrastructure oversight creates a complex landscape for developers. Projects that receive FERC approval are still frequently challenged in federal courts, leading to what industry participants describe as “regulatory uncertainty” that discourages long-term capital investment.

What Does the Future Hold for Northeast Gas Infrastructure?

The outlook for new pipeline capacity remains tied to both judicial outcomes and the evolving energy transition policies of states like New York and Pennsylvania. While some operators are focusing on “debottlenecking” existing lines—increasing pressure or adding compression to boost throughput without building new routes—these efforts provide only incremental relief.

Market Comparison: Northeast vs. National Benchmarks

| Metric | Northeast Regional Market | Henry Hub (National) |

| :— | :— | :— |

| Primary Driver | Infrastructure Constraints | Global Export Demand |

| Price Status | Often Discounted (Basis) | Benchmark Reference |

| Key Variable | Pipeline Permitting | LNG Feedgas Volumes |

*Source: Compiled from EIA and S&P Global Commodity Insights data.*

Moving forward, the industry is closely watching how federal agencies balance the need for grid reliability with climate-related permitting requirements. As the region shifts toward a greater reliance on natural gas for electricity generation—partly to offset the retirement of coal and oil-fired plants—the pressure to resolve these infrastructure disputes is expected to intensify. Investors remain cautious, waiting for clear signals that the regulatory environment will allow for sustained, predictable project timelines.