{kind=link}

Navigating Retirement with Home Equity and Fixed Income

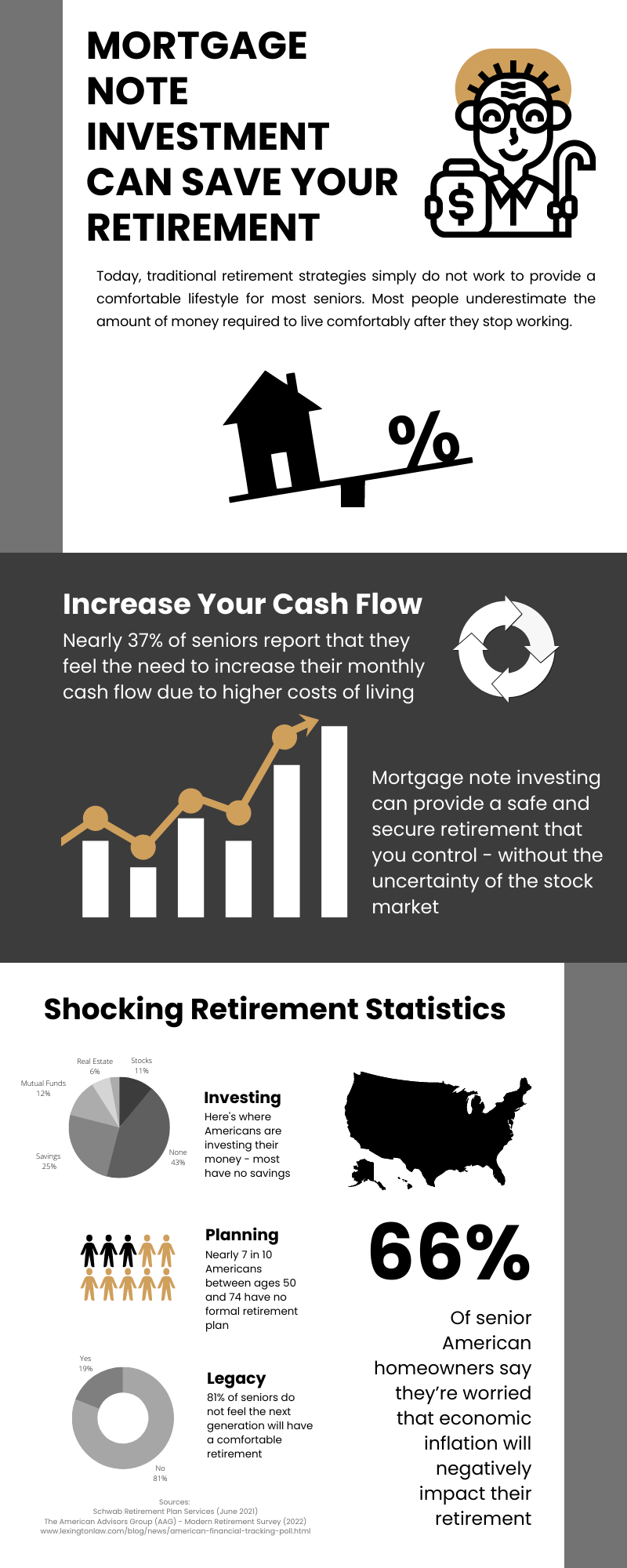

Planning for retirement requires a delicate balance between liquid assets, guaranteed income streams, and real estate equity. For those entering retirement with a combination of a pension, Social Security, and modest savings, the primary challenge often lies in managing debt—specifically a significant mortgage—against the backdrop of economic volatility.

Key Takeaways for Retirement Planning

- Income Stability: Pensions and Social Security provide the foundation, but inflation and systemic risks can erode their purchasing power.

- Equity vs. Liquidity: High home equity is a powerful asset, but it cannot be used to pay monthly bills without a strategic liquidation or borrowing plan.

- Systemic Risks: Future adjustments to Social Security benefits and inflation forecasts can significantly impact long-term budgeting.

Evaluating the Social Security Outlook

While Social Security is a cornerstone of retirement, it is not without risk. Current projections indicate that the system faces significant headwinds. According to reports from MarketWatch, the program could potentially run out of money in as little as six years.

The implications for retirees are stark: unless Congress intervenes to shore up the system, beneficiaries could face an automatic 20% cut to their checks starting in roughly six years. This makes it imperative for retirees to avoid over-reliance on Social Security and to maintain a diversified financial cushion.

The Impact of Inflation

Inflation remains a critical variable in retirement sustainability. Analysts warn that Cost-of-Living Adjustments (COLA) may demand to rise by as much as 3.2% to preserve pace with rising costs. While a higher COLA increases the nominal monthly check, it is often a reaction to “rocketing inflation” that increases the cost of basic goods and services, potentially neutralizing the benefit of the increase.

Managing Home Equity and Debt

A common dilemma for retirees is holding significant equity in a primary residence while carrying a substantial mortgage. In a scenario where a home is worth $1 million but carries a $300,000 debt, the homeowner possesses $700,000 in “paper wealth.”

Because this equity is illiquid, it doesn’t contribute to daily cash flow. Retirees must decide whether to maintain the mortgage and use their pension and Social Security for payments, or to find a way to unlock that equity to eliminate debt and increase monthly disposable income.

Strategic Paths to Retirement Sustainability

Depending on individual risk tolerance and cash flow needs, retirees generally consider three paths:

1. The Debt-Retention Strategy

If the pension and Social Security payments comfortably cover the mortgage and living expenses, keeping the home and the debt may be viable. However, this leaves the retiree vulnerable to the aforementioned 20% potential cut in Social Security benefits.

2. Downsizing for Liquidity

Selling a high-value home and purchasing a smaller, less expensive property allows a retiree to eliminate the mortgage and convert a portion of the $700,000 equity into liquid savings. This increases the cash buffer beyond the initial $235,000 in savings.

3. Equity Extraction

Options such as reverse mortgages or home equity lines of credit (HELOCs) can provide liquidity without requiring a move. However, these options often come with interest costs that can erode the estate’s total value over time.

Frequently Asked Questions

What happens if Social Security funds run out?

If the trust funds are depleted and Congress does not act, the system may be forced to implement automatic benefit cuts, which some estimates place at approximately 20%.

How does COLA affect my retirement check?

The Cost-of-Living Adjustment is designed to protect the purchasing power of Social Security benefits. When inflation rises, the COLA typically increases the monthly payment amount to help retirees keep up with the cost of living.

Is it better to pay off a mortgage before retiring?

Eliminating a mortgage reduces monthly overhead, which lowers the “burn rate” of savings. For those with significant home equity but limited liquid cash, downsizing is often the most effective way to achieve this.

Related reading