{kind=link}

The 30-Year Treasury Yield Surges to 20-Year Highs: What It Means for Markets, Inflation, and the Fed

The 30-year Treasury yield has climbed to its highest level in nearly two decades, reaching 5.13% as of May 15, 2026—a move that signals a seismic shift in global financial markets. This spike, driven by persistent inflation fears, geopolitical tensions, and hawkish Federal Reserve policy, is forcing investors to reassess risk, debt strategies, and the long-term trajectory of interest rates. For businesses, homeowners, and policymakers, the implications are profound. Here’s what you need to know.

— ### Why the 30-Year Yield Matters The 30-year Treasury bond is often called the “long bond,” and its yield serves as a benchmark for mortgage rates, corporate borrowing costs, and even global risk appetites. When yields rise, borrowing becomes more expensive, and fixed-income assets like bonds lose value. The current surge—now at levels last seen in June 2007—is a clear warning that the era of ultra-low rates is over. Key drivers behind the surge: – Inflation persistence: The Consumer Price Index (CPI) rose 3.8% year-over-year in April 2026, driven by soaring energy costs ([U.S. Bureau of Labor Statistics](https://www.bls.gov/cpi/)). – Geopolitical risks: The unresolved Iran war and Strait of Hormuz tensions have sent oil prices higher, further stoking inflation fears ([U.S. Energy Information Administration](https://www.eia.gov/)). – Fed policy uncertainty: With the Federal Reserve maintaining a restrictive stance, markets are pricing in prolonged high rates ([Federal Reserve Economic Data](https://fred.stlouisfed.org/)). — ### The Domino Effect: How Higher Yields Reshape Markets #### 1. Mortgages and Housing: A Double Whammy – The 30-year mortgage rate, closely tied to the 10-year Treasury yield (now at 4.59%), has already surged to its highest level since May 2025 ([Freddie Mac](https://www.freddiemac.com/)). – Impact: Homebuyers face higher monthly payments, and refinancing becomes less attractive. Existing homeowners with adjustable-rate mortgages (ARMs) may see their rates reset upward. #### 2. Stocks and Corporate Debt: The Sell-Off Signal – Rising yields tighten financial conditions, historically triggering sell-offs in growth stocks and high-debt companies. The S&P 500 dropped 1.2% on May 15, 2026, with tech and real estate sectors leading declines ([S&P Global](https://www.spglobal.com/)). – Corporate borrowing: Companies with long-term debt (e.g., utilities, real estate investment trusts) will see higher interest expenses, squeezing margins. #### 3. Global Bonds: A Flight to Safety Unravels – The U.S. Treasury yield spike is part of a broader global bond sell-off, with Germany’s 10-year bund yield hitting 2.8%—its highest since 2011 ([Deutsche Bundesbank](https://www.bundesbank.de/)). – Emerging markets: Countries with dollar-denominated debt (e.g., Argentina, Turkey) face renewed default risks as capital flows reverse. — ### The Fed’s Dilemma: To Cut or Not to Cut? The Federal Reserve is caught between two fires: 1. Inflation: Core CPI remains sticky, with services inflation (excluding housing) at 4.1% YoY ([BLS](https://www.bls.gov/)). 2. Growth risks: A prolonged high-rate environment could tip the economy into recession, as seen in the 2022–2023 slowdown. Market bets: – The CME Group’s FedWatch tool shows traders now price in a 25-basis-point rate cut by December 2026, down from a 50% chance just weeks ago ([CME FedWatch](https://www.cmegroup.com/)). – Key question: Will the Fed pivot before yields breach 5.5% on the 30-year**—a level that historically triggers preemptive easing? — ### What This Means for Investors and Businesses #### For Investors: ✅ Bonds: Long-duration Treasuries and corporates are under pressure. Consider shorter-duration bonds or floating-rate notes to hedge against further yield spikes. ✅ Stocks: Value stocks (financials, energy) may outperform growth (tech, consumer discretionary) in this environment. ✅ Gold and commodities: Safe-haven assets like gold and oil could see volatility as geopolitical risks persist. #### For Businesses: 💰 Debt refinancing: Lock in rates now if possible—expect higher costs for new issuances. 🏢 Commercial real estate: Cap rates will rise, pressuring property values in sectors like offices and retail. 📈 M&A activity: Higher borrowing costs could delay deals, but distressed assets may emerge as targets. — ### The Bigger Picture: Are We in a New Era of High Rates? The 30-year yield’s surge isn’t just a blip—it reflects structural changes: – Demographics: An aging population increases demand for safe assets like Treasuries, but supply constraints keep yields elevated. – Fiscal policy: Rising government debt (now $34.5 trillion, or 95% of GDP ([U.S. Treasury](https://www.treasury.gov/)) limits the Fed’s ability to cut rates aggressively. – Global central bank divergence: While the Fed may ease, the European Central Bank and Bank of Japan are expected to keep rates higher for longer, keeping the dollar strong. Historical comparison: | Event | 30-Year Yield Peak | Outcome | 2007 Financial Crisis | ~5.2% | Recession, Fed cuts to near-zero | | 1994 Bond Market Crash | ~8.5% | Fed hiked rates, but growth held | | 1981 Volcker Shock | ~15% | Deep recession, inflation crushed | Today’s parallel: The 2007 comparison is the closest, but with a critical difference—inflation expectations are far stickier than in the mid-2000s. — ### FAQ: Your Burning Questions Answered

Q: Will mortgage rates keep rising?

A: Likely yes—unless the Fed cuts rates aggressively or inflation cools sharply. The 30-year mortgage rate is already near its highest level since 2023, and further yield increases will push it higher. Locking in a rate today may be wise for long-term borrowers.

Q: Are bonds still a safe investment?

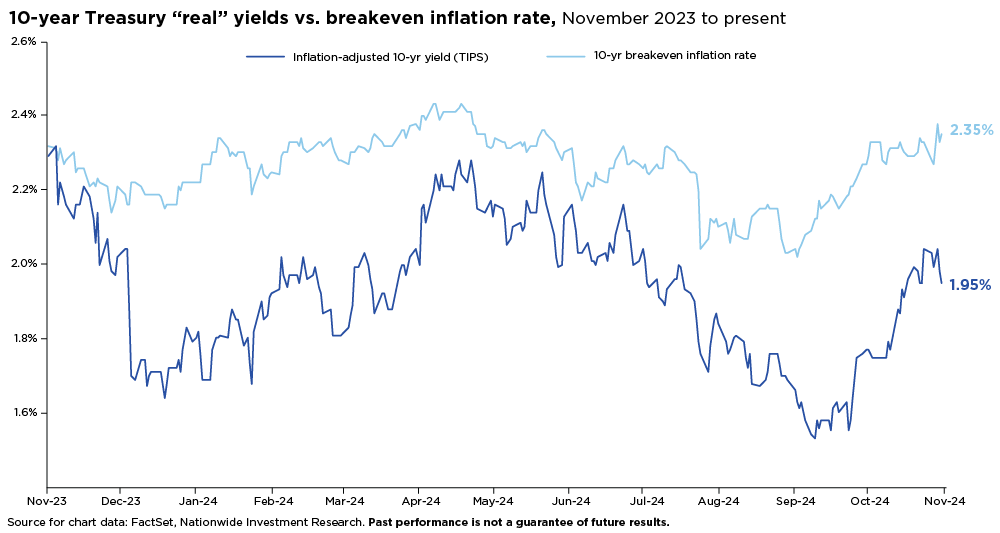

A: Not in their traditional form. Long-duration bonds (10+ years) are volatile in a rising-rate environment. Instead, consider: – Short-term Treasuries (1–3 years) – Tips (Treasury Inflation-Protected Securities) – Floating-rate notes

Q: Could this trigger a recession?

A: Possible—but not inevitable. The 2022–2023 rate hikes caused a growth slowdown, but a full recession requires a more severe tightening. Watch for: – Inverted yield curve (already present, with 2-year yields above 10-year) – Job market cracks (unemployment currently at 3.9%, but rising) – Consumer spending (retail sales growth has slowed to 2.5% YoY)

Q: What sectors benefit from higher yields?

A: Financials (banks, asset managers), energy, and utilities typically thrive. Tech and consumer staples may struggle unless earnings growth offsets higher borrowing costs.

— ### The Bottom Line: Prepare for a Higher-Rate World The 30-year Treasury yield’s surge is a wake-up call: the post-2008 era of cheap money is over. For investors, the playbook shifts from “reach for yield” to “preserve capital.” For businesses, cost management and financial flexibility become critical. And for policymakers, the challenge is threading the needle between taming inflation and avoiding a growth collapse. One thing is certain: The next 12–18 months will test whether markets have fully priced in the new reality of persistent high rates. The Fed’s next move—and the geopolitical landscape—will dictate the path forward. —

Key Takeaways

- The 30-year Treasury yield hit 5.13%, its highest since June 2007, signaling a shift to higher long-term rates.

- Drivers include sticky inflation (3.8% YoY CPI), geopolitical risks (Strait of Hormuz), and Fed policy uncertainty.

- Mortgages, stocks, and corporate debt are under pressure, while safe-haven assets like gold and oil face volatility.

- The Fed’s next move is critical—markets now price in a rate cut by December 2026, but inflation risks delay.

- Investors should prioritize liquidity, shorter-duration assets, and hedging strategies in this environment.