{kind=link}

Should You Pay Off Your Mortgage Early? A Strategic Analysis for Italian Borrowers (2026)

With a €60,000 mortgage at a fixed 1.6% rate maturing in 2035, you’re facing a critical financial decision: Should you pay it off early, or keep the liquidity for higher-yielding opportunities? The answer depends on three key factors—opportunity cost, tax implications, and personal risk tolerance. Here’s how to decide, backed by 2026 market data and expert insights.

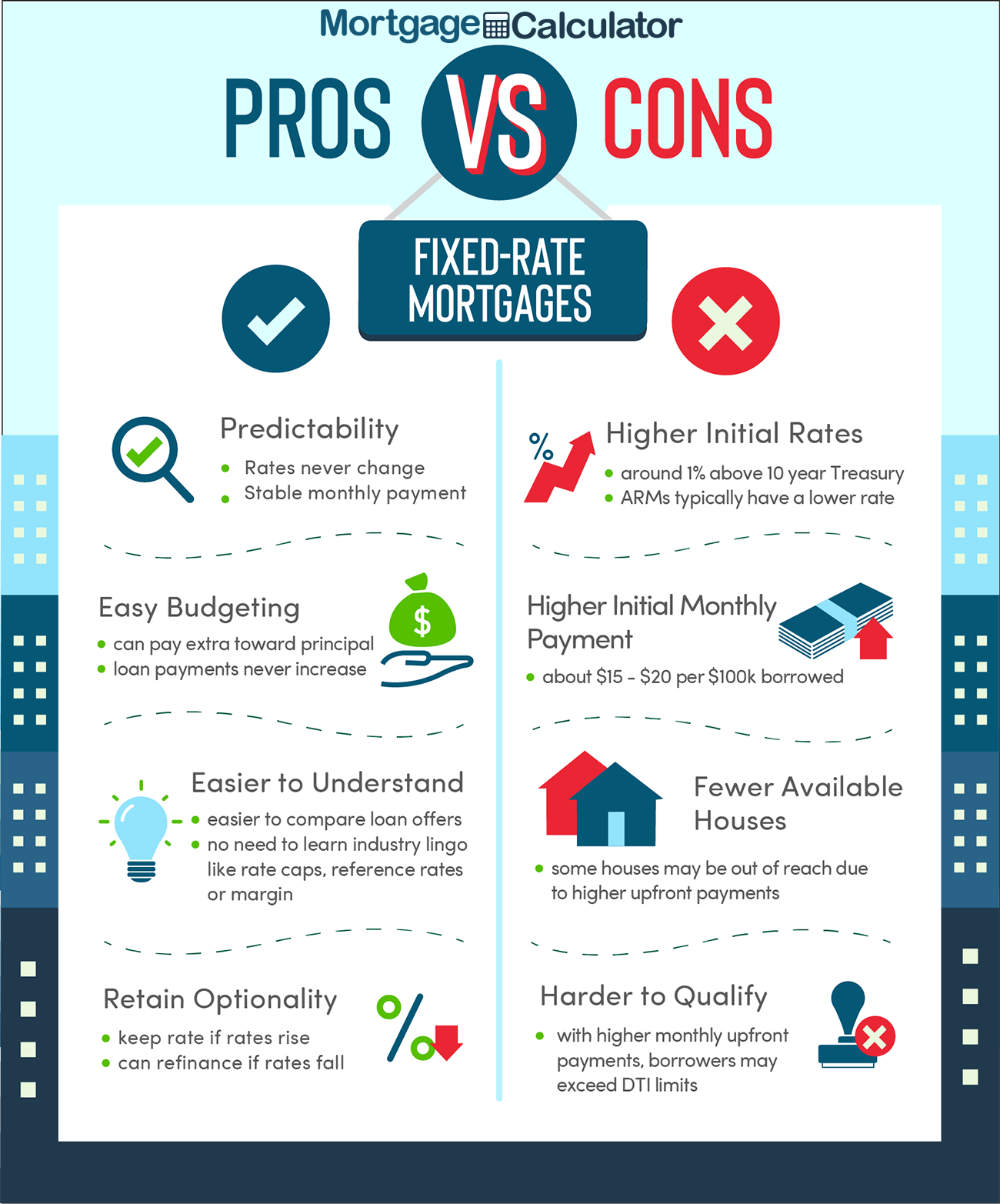

— ### **The Core Question: Is Early Repayment Worth It?** Your mortgage—€58,000 remaining, fixed at 1.6%, due in 2035—presents a straightforward math problem: – **Annual interest cost**: ~€928 (1.6% of €58,000). – **Total interest over 9 years**: ~€8,352 if paid as scheduled. But the decision isn’t just about interest. It’s about **what you could earn elsewhere** with that €60,000. In Italy’s 2026 financial landscape, the answer hinges on three scenarios: 1. **You have no higher-yielding investments** (e.g., emergency funds, low-risk savings). 2. **You can reinvest the funds at a rate higher than 1.6%** (e.g., dividend stocks, P2P lending, or business opportunities). 3. **Your personal risk profile** favors debt elimination over speculative gains. — ### **Scenario 1: No Better Use for the Money? Pay It Off.** If your liquidity is sitting in a **0.5%–1.0% yield account** (the average Italian savings rate in early 2026 per Banca d’Italia’s latest report), eliminating the mortgage **locks in a guaranteed 1.6% return**—far superior to inflation-adjusted savings. **Key Benefits:** – **Psychological relief**: Debt elimination reduces stress, especially in volatile markets. – **No refinancing risk**: Fixed rates protect you from future hikes (though 1.6% is already near historic lows for Italy). – **Simplified finances**: Fewer monthly obligations improve cash flow flexibility. **When to Choose This:** ✅ You’re risk-averse. ✅ Your savings are earning <1.6%. ✅ You lack diversified investments (e.g., no stocks, bonds, or rental income). --- ### **Scenario 2: Higher-Yielding Opportunities Exist? Hold or Invest Instead** If you can **earn more than 1.6% after taxes and fees**, keeping the mortgage may be smarter. For example: - **Dividend stocks**: Italian blue chips like Enel or UniCredit yield ~3–5% pre-tax in 2026 (Borsa Italiana data). – **P2P lending**: Platforms like Moneyfarm offer ~4–6% net returns on balanced portfolios. – **Real estate**: Rental yields in Milan and Rome average **4–6%** (Omniland 2026 report). **Tax Consideration**: Italy’s **26% capital gains tax** (for holdings >1 year) reduces net returns. If your post-tax yield exceeds 1.6%, investing may still win. **When to Choose This:** ✅ You have a diversified, tax-efficient investment strategy. ✅ Your portfolio can absorb short-term volatility. ✅ You’re targeting long-term wealth growth (e.g., retirement). — ### **Scenario 3: The Hybrid Approach—Partial Repayment** Instead of an all-or-nothing decision, consider **targeted prepayments**: – **Overpay by 20–30%** to reduce the loan’s interest burden without tying up all your capital. – **Use windfalls** (bonuses, tax refunds, inheritance) to chip away at the principal. – **Refinance if rates drop**: Monitor the ECB’s 2026 rate forecasts—if fixed mortgages fall below 1.2%, refinancing could save you more than early repayment. **Example**: Paying an extra €10,000 now could shave **~1.5 years off your mortgage** and save ~€1,300 in interest. — ### **The Tax Angle: Deductibility and Capital Gains** In Italy, mortgage interest is **no longer tax-deductible** for most borrowers (post-2020 reforms). However: – **First-time buyers** (under 36) may still qualify for **50% interest deductions** (Agenzia delle Entrate). – **Capital gains on investments**: If you sell assets for a profit, you’ll owe **26% tax**—but this applies only to realized gains, not hypothetical returns. **Bottom Line**: Taxes favor early repayment **only if you’re in a high tax bracket and have no offsetting deductions**. — ### **Key Takeaways: Decision Flowchart** Use this quick guide to align your choice with your goals: | **Your Situation** | **Recommended Action** | **Why?** | |———————————–|————————————–|——————————————| | Savings yield <1.6% | Pay off early | Guaranteed return beats inflation. | | Can earn >2.5% post-tax elsewhere | Keep mortgage, invest funds | Higher expected returns justify risk. | | Risk-averse or nearing retirement | Pay off early | Stability > speculative gains. | | Have windfalls (e.g., bonus) | Overpay strategically | Reduce debt without sacrificing liquidity. | | Rates may drop in 2027 | Wait and monitor ECB trends | Refinancing could save more later. | — ### **FAQ: Common Concerns Addressed** #### **1. “Will paying off my mortgage hurt my credit score?”** No. In Italy, **paying off debt early has no negative impact** on your credit score (CRIF data). In fact, it may improve your **debt-to-income ratio**, which lenders view favorably. #### **2. “What if I need the money later?”** – **Emergency funds**: Keep **3–6 months’ expenses** in liquid assets (e.g., high-yield savings). – **Home equity**: If you later need cash, a **home equity loan** (tasso fisso ~2.5–3.5% in 2026) could be an option—but only if your property value has risen. #### **3. “Should I prioritize this over other debts?”** Yes. A **1.6% fixed-rate mortgage is among the cheapest debt** most Italians face. Prioritize: 1. High-interest debt (e.g., credit cards at 15–20%). 2. Variable-rate loans (risk of future hikes). 3. Your mortgage (only if it’s truly costing you more than alternatives). — ### **The Bottom Line: What Should You Do?** For your specific case (€60K, 1.6% fixed, 2035 maturity), **the optimal path depends on your investment horizon and risk tolerance**: – **If you’re conservative or lack better opportunities → Pay it off**. You’ll save ~€8,352 in interest and gain peace of mind. – **If you’re investing in assets yielding >2.5% post-tax → Keep the mortgage**. The math favors growth over debt elimination. – **If you’re unsure → Overpay by 20–30%** and reassess in 12–18 months. **One thing is certain**: In Italy’s 2026 low-rate environment, **your mortgage is no longer a financial burden—it’s a strategic tool**. Use it wisely. —

Further Reading

- Banca d’Italia: Italian Savings Rates (2026)

- Agenzia delle Entrate: Mortgage Tax Deductions

- ECB: 2026–2027 Rate Forecasts

- Omniland: Italian Rental Yields (2026)

Related reading