{kind=link}

KSE-100 Index Recovers on Value-Hunting Amid Market Volatility

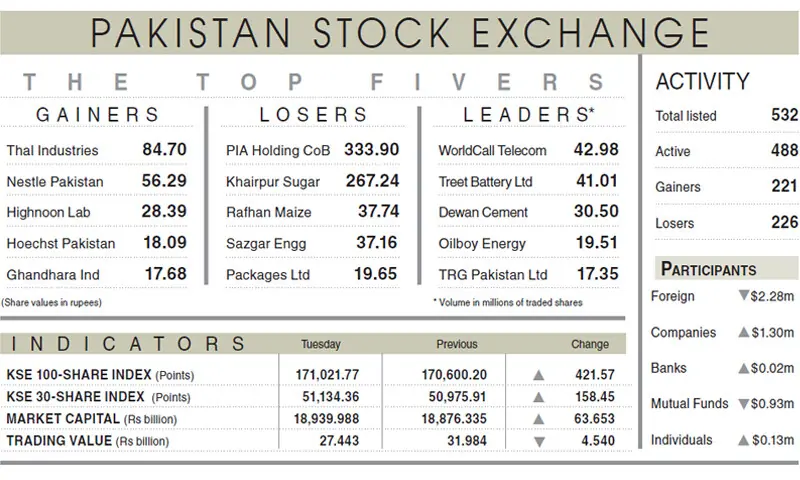

The Pakistan Stock Exchange (PSX) experienced a session of significant fluctuations on Tuesday, June 3, 2026. Despite a lack of positive economic catalysts and continued uncertainty regarding a potential US-Iran peace deal, the benchmark KSE-100 index managed to close in positive territory, driven by late-session value-hunting.

Market Performance and Key Drivers

According to data from Topline Securities Ltd, the KSE-100 index concluded the trading day at 171,021.77 points, reflecting a gain of 421.57 points, or 0.25 percent. The session was characterized by a wide trading range. the index reached an intraday high of 171,856 before retreating to a low of 170,249 amid profit-taking at higher levels.

Market sentiment found support in the decline of international oil prices, which encouraged buying activity in several heavyweight sectors. The primary contributors to the index’s recovery included:

- Meezan Bank

- Fauji Fertiliser

- United Bank

- Pakistan Telecommunication Company

- Pakistan Petroleum

Together, these equities contributed approximately 460 points to the benchmark index, helping to offset the broader market volatility.

Trading Activity and Macroeconomic Outlook

While the index finished the day higher, overall investor participation saw a decline. Total trading volume dropped by 6.60 percent to 550.79 million shares, while the traded value decreased by 14.19 percent to Rs27.4 billion. Analysts note that while the potential for a US-Iran diplomatic agreement remains a primary catalyst for market confidence, the lack of a finalized deal continues to fuel short-term instability.

On the macroeconomic front, the fiscal landscape remains in focus as reports indicate that the presentation of the FY27 federal budget has been rescheduled. Originally planned for June 5, the budget announcement is now expected to take place between June 10 and June 12.

Sectoral Spotlight: Cement Industry

The cement sector faced headwinds in May, with total despatches declining by 21 percent year-on-year to 3.8 million tonnes. This contraction was observed across both domestic and international markets:

- Local Sales: Fell to 3.2 million tonnes from 3.9 million tonnes in the previous year.

- Exports: Dropped by 36 percent year-on-year to 632,648 tonnes, compared to 989,434 tonnes in the same period last year.

Industry observers attribute this downturn largely to a reduction in working days resulting from the Eid holidays.

Key Takeaways for Investors

- Value-Hunting Prevails: Despite volatility, institutional interest in heavyweight stocks provided a floor for the market.

- Geopolitical Sensitivity: The market remains highly reactive to diplomatic developments between the US and Iran.

- Budget Delay: The postponement of the federal budget announcement may keep market participants in a wait-and-see mode regarding fiscal policy direction.

As the market navigates these uncertainties, investors should remain cautious, focusing on long-term value in the face of ongoing regional de-escalation efforts and shifting macroeconomic timelines.