{kind=link}

Traditional vs. Roth IRAs: How to Choose the Right Retirement Strategy

Deciding between a Traditional and Roth IRA isn’t just about picking an account; it’s about deciding when you want to pay the government its cut. Whether you’re a high-earner looking for a “backdoor” entry or someone starting their first investment account, the choice boils down to your current tax bracket versus your expected bracket in retirement.

- Traditional IRA: Offers an immediate tax deduction; you pay taxes upon withdrawal.

- Roth IRA: No immediate tax break; withdrawals in retirement are tax-free.

- Backdoor Roth: A strategy allowing high-income earners to contribute to a Roth IRA despite income limits.

- Deadline: Taxpayers have until Wednesday, April 15, to make contributions for the 2025 tax year.

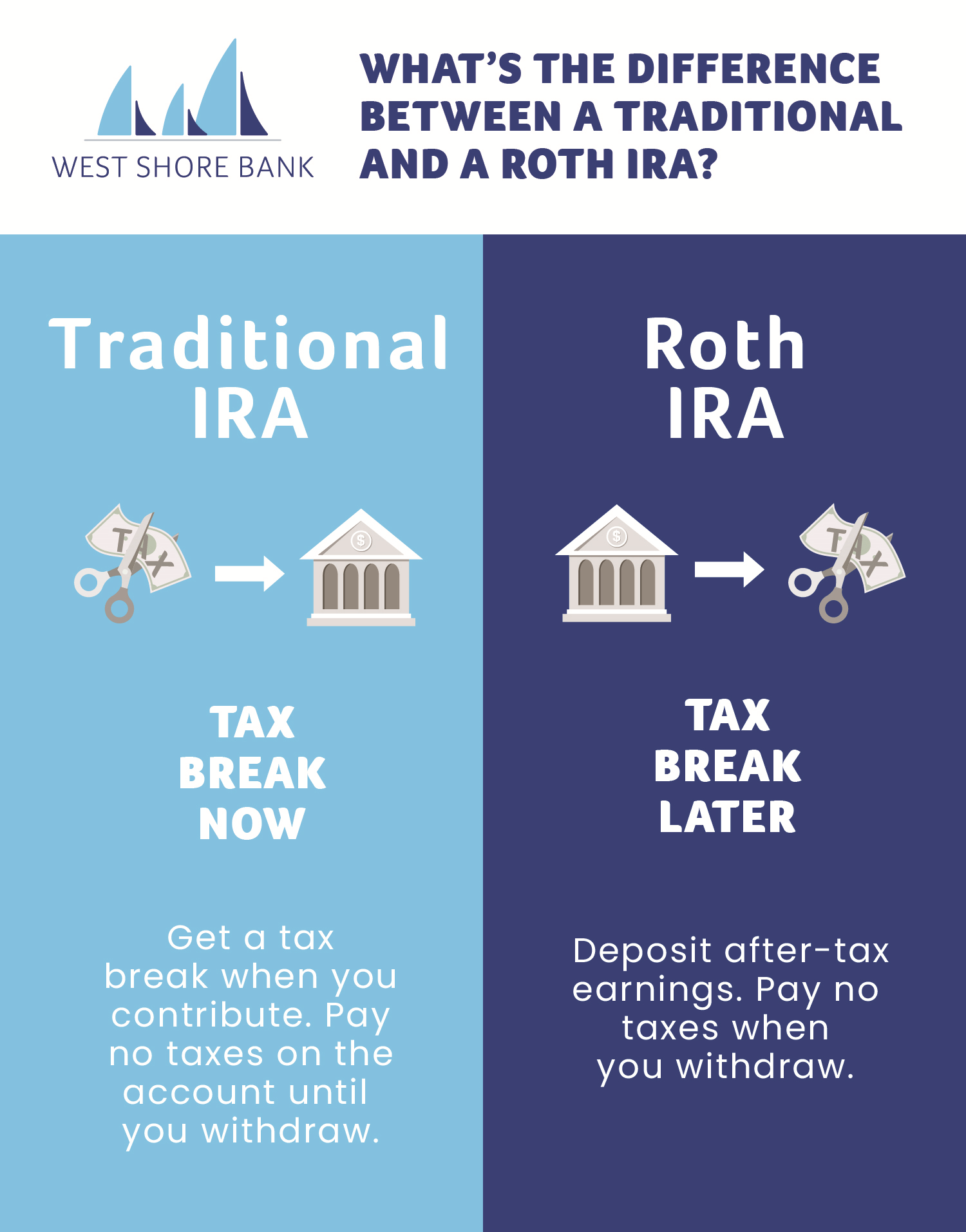

Understanding the Core Difference: Pre-Tax vs. After-Tax

The fundamental difference between these two accounts is the timing of the tax hit. A Traditional IRA allows you to contribute pretax dollars. This means you can deduct the contribution from your current taxable income, lowering your tax bill today. However, the trade-off is that every dollar you withdraw during retirement is counted as taxable income.

A Roth IRA flips this script. You contribute after-tax dollars, meaning there’s no immediate tax deduction. The benefit arrives later: when you withdraw the money in retirement, the principal and all the growth are entirely tax-free.

Comparison at a Glance

| Feature | Traditional IRA | Roth IRA |

|---|---|---|

| Upfront Tax Break | Yes (Deductible) | No |

| Tax on Withdrawals | Taxed as Income | Tax-Free |

| RMDs | Required starting at age 73 | No RMDs |

The “Backdoor Roth” Strategy for High Earners

For those whose adjusted gross income exceeds official limits for straightforward Roth contributions, the “backdoor Roth” is a critical tool. This two-step process allows anyone with taxable income to shelter their future gains from federal taxes, regardless of how much they earn.

According to MarketWatch, this strategy is particularly effective if you convert a traditional IRA to a Roth. While you’ll take a one-time tax hit during the conversion, it simplifies future contributions by allowing a clean backdoor Roth process every year without further complications.

Contribution Limits for 2025

For the 2025 tax year, the contribution limits are as follows:

- Standard Limit: $7,000

- Catch-up Contribution: An additional $1,000 for individuals aged 50 or older (totaling $8,000).

It’s important to note that you cannot contribute more than your earned income for the year. If you’re utilizing a spousal IRA, the combined contributions cannot exceed your joint income.

Which One Should You Choose?

The decision often comes down to your marginal tax rate. If your rate is higher now than you expect it to be in retirement, a Traditional IRA’s upfront deduction is generally more attractive. If you believe you’ll be in a higher bracket later—or if you simply want the flexibility of tax-free income—the Roth is the way to go.

Other Factors to Consider:

- Liquidity: Roth IRA contributions (including those rolled over from a Roth 401(k)) can be accessed tax-free and penalty-free at any time.

- Estate Planning: Because Roth IRAs don’t have required minimum distributions (RMDs), you can leave the assets to grow and pass them on without forcing yourself to take money out at age 73.

- Diversification: Many experts suggest a “savvy combo” of both account types to provide tax flexibility during retirement.

Frequently Asked Questions

When is the deadline for 2025 contributions?

U.S. Taxpayers have until Wednesday, April 15, to take advantage of the Roth IRA tax break and make contributions for the 2025 tax year.

Can I have both a Traditional and a Roth IRA?

Yes. Having both can be an appropriate strategy to manage your tax liability across different stages of your life.

What happens if I withdraw from a Roth IRA early?

You can withdraw your original contributions tax-free and penalty-free. However, if you withdraw more than what you contributed, you may be subject to taxes and penalties.

Final Outlook

Retirement planning is rarely one-size-fits-all. While the backdoor Roth offers a powerful loophole for high earners, the choice between traditional and Roth accounts should be based on a cold analysis of your current and future tax brackets. As tax laws evolve, maintaining a mix of both account types remains one of the most effective ways to hedge against future tax increases.