{kind=link}

The Evolving Landscape of U.S. Consumer Credit: Key Insights for 2026

The U.S. Consumer credit market is currently navigating a complex, “K-shaped” trajectory, characterized by shifting origination patterns and rising financial pressure on borrowers. According to TransUnion’s Q1 2026 Credit Industry Insights Report (CIIR), the auto-finance sector remains a focal point for this divergence, as market participants grapple with volume fluctuations and the broader economic environment.

Auto-Finance Performance and Market Trends

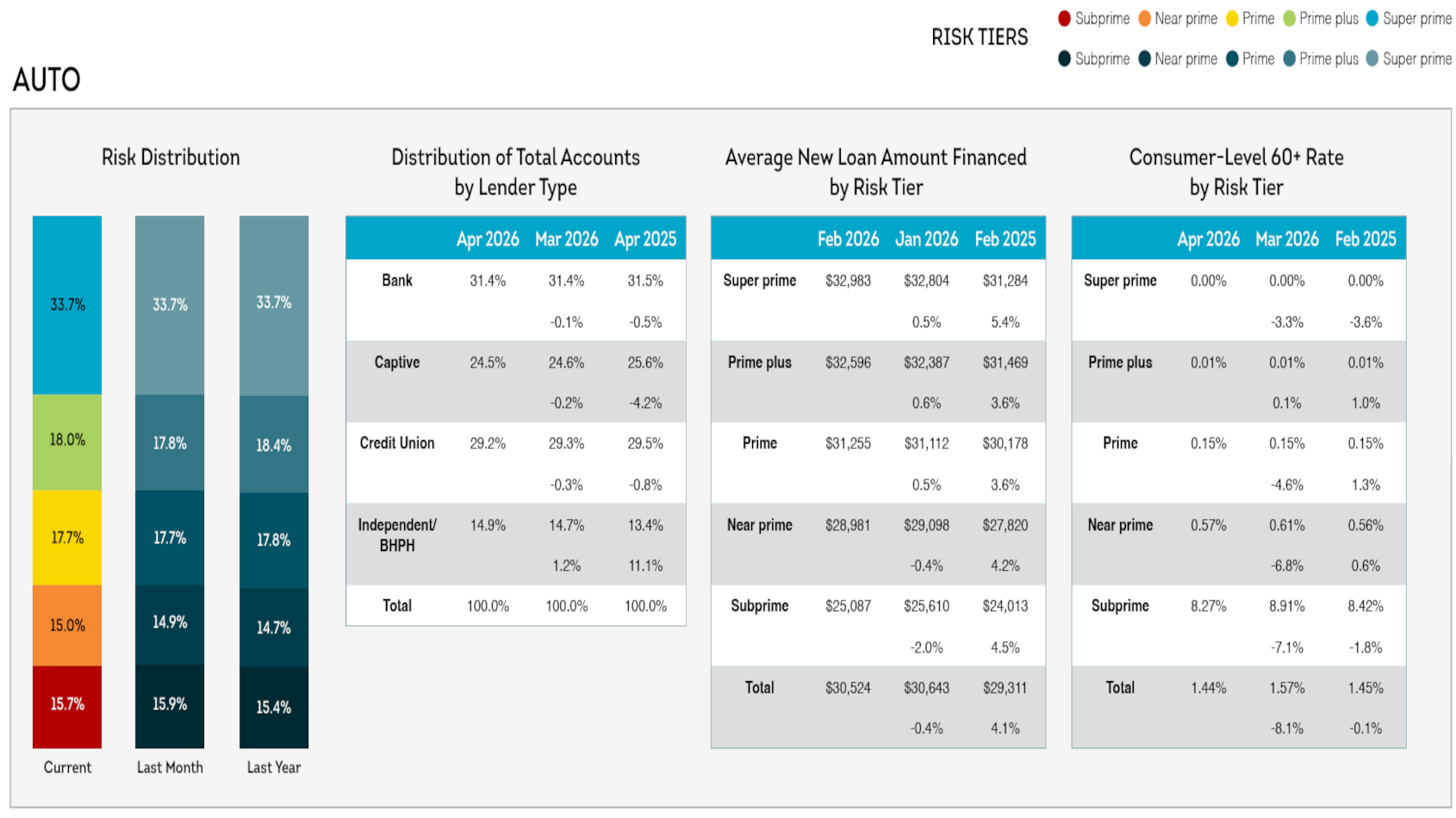

The auto-finance market continues to show signs of a sluggish recovery, with origination volumes still trailing pre-pandemic levels. Data from the Q1 2026 report indicates that originations—viewed one quarter in arrears—declined by 0.92% in Q4 2025. When measured against the same period in 2019, volumes remain approximately 10% lower than those recorded prior to the pandemic.

Interestingly, this downward pressure on originations is not limited to subprime borrowers. Analysts observed a contraction across higher credit tiers, with super-prime originations falling 5.4% year-over-year, while prime plus originations decreased by 2.9%.

Rising Costs and Financial Strain

For the average consumer, the cost of vehicle ownership continues to climb. TransUnion reported that average monthly payments for new vehicles increased by 4.3% year-over-year to $786, while used-vehicle payments rose 2.9% to $536. These increases are mirrored by the rise in amounts financed: new-vehicle financing climbed 6.6% to $45,028, and used-vehicle financing rose 5.0% to $27,232.

This upward trend in payment obligations is occurring alongside a slight deterioration in credit performance. As of Q1 2026, the 60-day delinquency rate in the auto-finance sector edged up to 1.57%.

Understanding Your Credit Report

While industry-wide trends provide a macro view of the economy, it is essential for individuals to remain informed about their personal credit health. TransUnion, one of the three nationwide consumer reporting companies, provides consumers with access to their credit data to help monitor their financial standing.

What You Should Know About Your Credit Data

- Access: Under federal guidelines, consumers are entitled to request free credit reports.

- Content: Reports typically include personal identification details, payment histories for credit cards and loans, debt collection information—such as medical debt exceeding $500 that is more than 365 days delinquent—and public records like bankruptcies.

- Security: Consumers have the right to place a freeze on their credit reports to prevent unauthorized access.

- Inquiries: It is a common misconception that checking your own credit report hurts your score; requesting your own report does not negatively impact your credit standing.

Key Takeaways for Borrowers

- Market Divergence: The credit market is splitting along a K-shaped path, affecting borrowers across all credit tiers.

- Auto-Finance Headwinds: High amounts financed and rising monthly payments are contributing to increased risk for both consumers and lenders.

- Proactive Monitoring: Consumers should regularly review their credit reports for accuracy, as this is a fundamental step in maintaining financial health.

- Delinquency Trends: With 60-day delinquency rates in auto finance ticking upward, borrowers should prioritize maintaining consistent payment schedules to avoid long-term credit damage.

As the market moves through the remainder of 2026, the intersection of rising vehicle costs and tightening underwriting standards will likely remain a critical area for both investors and consumers to monitor. Staying informed through official credit reporting channels remains the most effective strategy for navigating these economic shifts.

Keep reading