{kind=link}

A credit card billing cycle is the interval between statement dates, typically lasting 28 to 31 days. After this cycle closes, issuers provide a grace period—usually 21 to 25 days—to pay the balance before interest accrues. According to the Consumer Financial Protection Bureau (CFPB), paying the full statement balance by the due date allows cardholders to avoid interest charges entirely.

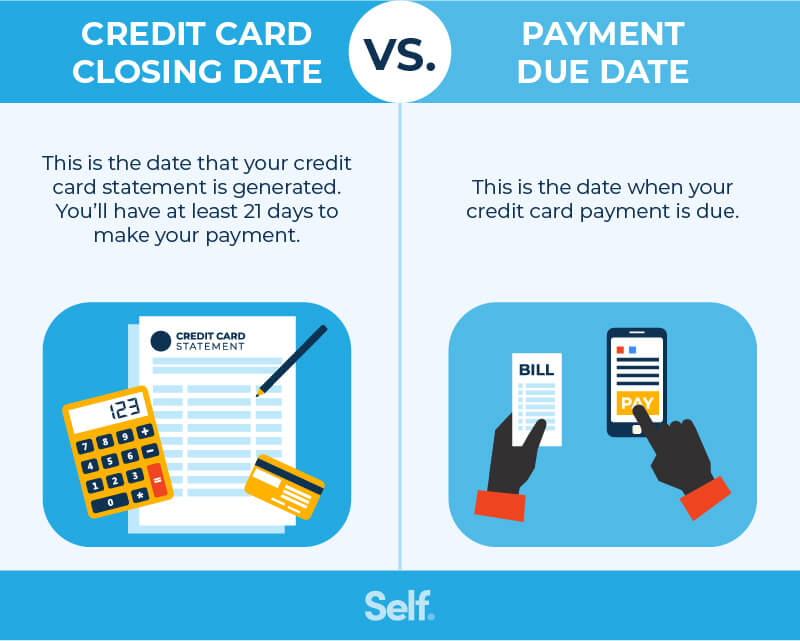

The Difference Between the Closing Date and the Due Date

Understanding the distinction between these two dates is the foundation of credit management. The closing date (or cutoff date) is the day the billing cycle ends. At this moment, the bank totals all transactions and generates your monthly statement. This balance is the “snapshot” of what you owe for that period.

The due date occurs several weeks later. This is the final deadline to make a payment to avoid late fees and interest. For example, if your billing cycle ends on October 1 and your grace period is 25 days, your payment is due by October 26. Any balance remaining after this date triggers the application of the Annual Percentage Rate (APR).

How the Grace Period Works and When It Disappears

The grace period is the interest-free window between the closing date and the due date. It exists to give consumers time to receive their bill and arrange payment. However, this benefit isn’t permanent. According to Investopedia, the grace period typically only applies if you paid your previous month’s statement balance in full.

If a cardholder carries a balance from one month to the next, they enter a state of “revolving credit.” In this scenario, the grace period vanishes. New purchases begin accruing interest immediately from the date of the transaction, regardless of when the next due date arrives. To restore the grace period, most issuers require the balance to be paid in full for one or two consecutive billing cycles.

Strategic Timing: Maximizing Your Interest-Free Float

Savvy users time their largest purchases to maximize the time they hold onto their cash, a strategy known as “float.” By making a significant purchase immediately after the closing date, the transaction won’t appear on a statement for nearly 30 days. When the next statement is generated, the user still has another 20 to 25 days before the payment is due.

This timing can effectively grant the consumer up to 50 to 55 days of interest-free borrowing. This is a common tactic used by business owners to manage short-term cash flow without incurring financing costs.

The Impact of the Cutoff Date on Credit Scores

The closing date is more than just a billing marker; it is the day your credit utilization ratio is reported to credit bureaus like Experian and Equifax. Credit utilization is the percentage of your total available credit that you are currently using.

If you have a $10,000 limit and your balance is $4,000 on the closing date, the bank reports 40% utilization, even if you pay that balance in full two days later. High utilization can lower a credit score. To optimize this, some users make a “pre-payment” a few days before the closing date to ensure the reported balance is low, thereby boosting their credit score.

Comparison: Closing Date vs. Due Date

| Feature | Closing Date (Cutoff) | Due Date |

|---|---|---|

| Purpose | Ends the billing cycle; generates the statement. | Deadline to pay the statement balance. |

| Credit Impact | Determines the utilization ratio reported to bureaus. | Missing this date results in late fees and score drops. |

| Timing | Occurs every ~30 days. | Occurs ~21-25 days after the closing date. |

| Action Required | None (Administrative snapshot). | Payment of at least the minimum (or full balance). |

Frequently Asked Questions

What happens if I pay before the closing date?

Paying before the closing date reduces the balance that will appear on your statement. This lowers your reported credit utilization, which can positively impact your credit score.

Can the closing date change?

Yes. While most dates are fixed, many issuers allow customers to request a change to their billing cycle date to better align with their payroll schedule.

Does the minimum payment stop interest?

No. Paying only the minimum amount avoids late fees and protects your account from going into default, but it does not stop interest from accruing on the remaining unpaid balance.