{kind=link}

U.S. Consumer Borrowing Surges in March: A Deep Dive into Credit Trends and Economic Implications

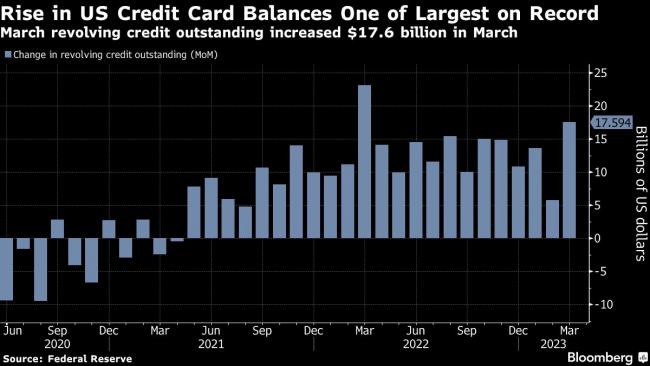

May 7, 2026 — American consumers ramped up borrowing in March at the fastest pace since late 2022, driven by a sharp rise in both credit card balances and non-revolving credit. The latest data from the Federal Reserve’s G.19 Consumer Credit Report reveals a 5.8% annualized increase in total consumer credit—a notable acceleration from the 3.2% growth observed in the first quarter. This surge, the most significant since the post-pandemic borrowing boom of 2022, signals shifting consumer behavior amid persistent economic uncertainty.

Key Drivers Behind the Borrowing Spike

The March increase was primarily fueled by two categories:

- Non-revolving credit (e.g., auto loans, student loans, and mortgages), which rose at a 3% annualized rate—reflecting continued demand for big-ticket purchases despite higher interest rates.

- Revolving credit (predominantly credit card debt), which climbed at a 3.8% annualized pace, marking a return to pre-2023 levels of consumer leverage.

Economists attribute the uptick to several factors:

- Inflation pressures forcing households to rely more on credit for essential expenses.

- Stronger labor markets in early 2026, with wage growth outpacing inflation in key sectors.

- Lender loosening of underwriting standards in response to competitive pressure, particularly for subprime borrowers.

“The data suggests consumers are increasingly treating credit as a tool to bridge income gaps rather than a last-resort option,” said Federal Reserve economists in a recent statement. “While this may support near-term spending, it also raises longer-term risks if borrowing outpaces income growth.”

Economic Implications: Boon or Burden?

The borrowing surge has sparked debate among policymakers and analysts about its broader economic impact.

Potential Benefits

- Consumer spending boost: Higher credit usage typically translates to increased retail sales, particularly in discretionary categories like travel and electronics.

- Lender profitability: Banks and fintechs stand to benefit from elevated origination volumes and higher interest revenue, especially as credit card APRs remain near multi-year highs.

- Housing market resilience: Non-revolving credit growth suggests continued demand for mortgages and home equity lines of credit (HELOCs), supporting real estate stability.

Risks to Monitor

- Debt sustainability: Household debt-to-income ratios are approaching pre-2008 financial crisis levels, raising concerns about repayment capacity if unemployment ticks up.

- Credit card delinquencies: Late payments on revolving debt have already risen by ~12% year-over-year in some regions, per Federal Reserve data.

- Fed policy divergence

The data arrives as the Federal Reserve faces pressure to balance inflation control with financial stability. While the central bank has signaled no immediate rate cuts, a prolonged borrowing boom could force a harder pivot if credit conditions deteriorate.

Industry Reactions: Banks vs. Fintechs

The credit expansion is reshaping competition between traditional banks and digital lenders:

- Banks are leveraging their deposit bases to offer competitive rates on credit cards and personal loans, though their market share in revolving credit has slipped to ~68% from 75% in 2020.

- Fintechs (e.g., Affirm, Afterpay, and buy-now-pay-later platforms) are gaining traction with younger borrowers, capturing ~15% of the revolving credit growth in March.

- Credit unions are also expanding their lending footprints, with membership-based models offering lower rates than big banks—a trend accelerated by the recent NCUA’s regulatory adjustments.

“The fragmentation of credit markets is here to stay,” noted CFPB Director Rohit Chopra in a recent speech. “Consumers now have more options—but also more complexity in managing debt across platforms.”

What’s Next for Consumer Credit?

Looking ahead, three scenarios could unfold:

- Moderation: If wage growth accelerates further, borrowing may stabilize as households rely less on credit for essentials.

- Acceleration: Persistent inflation or a recession could push more consumers into higher-cost debt, exacerbating financial stress.

- Regulatory crackdown: The CFPB or Fed may tighten underwriting rules if delinquencies rise sharply, as seen in the 2023 credit card market intervention.

For investors and entrepreneurs, the trends present both opportunities and warnings:

- Opportunity: Fintechs with AI-driven risk models (e.g., Upstart, Kabbage) are well-positioned to capture the “credit underserved” segment.

- Risk: Traditional banks face pressure to improve digital lending experiences or risk losing market share to agile competitors.

- Watchlist: Monitor the Fed’s balance sheet runoff and its potential impact on liquidity for consumer lenders.

Key Takeaways

To summarize the March consumer credit report:

- Total U.S. Consumer borrowing grew by 5.8% annualized in March—the fastest pace since late 2022.

- Revolving credit (credit cards) rose 3.8%, while non-revolving credit (auto/student loans) grew 3%.

- Banks remain dominant but are losing share to fintechs and credit unions.

- Risks include rising delinquencies and potential regulatory responses.

- Sectors to watch: retail, housing, and digital lending platforms.

FAQ: Consumer Credit Surge—What You Need to Know

Q: Why is credit card debt rising again?

A: Higher living costs (e.g., groceries, gas) and stagnant wage growth in some sectors are forcing consumers to rely on revolving credit for essentials. Promotional 0% APR offers have encouraged more spending.

Q: Is this a sign of a coming recession?

A: Not necessarily. While elevated borrowing is a red flag, it’s not a definitive recession indicator. The key will be tracking delinquency rates and income growth in the coming quarters.

Q: How can I protect my finances in this environment?

A: Focus on:

- Paying down high-interest debt (e.g., credit cards) aggressively.

- Avoiding new loans unless absolutely necessary.

- Building a 3–6 month emergency fund to reduce reliance on credit.

Q: Will the Federal Reserve raise interest rates further?

A: Unlikely in the near term. The Fed’s focus is now on monitoring inflation and financial stability, but any sharp rise in delinquencies could prompt a harder stance.

Conclusion: A Crossroads for Consumer Finance

The March borrowing surge underscores a pivotal moment for the U.S. Economy. While credit expansion can stimulate growth, it also tests the resilience of households and lenders alike. For businesses, the data signals both a competitive landscape and a need for vigilance in risk management. As always, the devil will be in the details—specifically, whether this borrowing binge proves to be a temporary blip or the beginning of a longer-term trend.

One thing is clear: The era of “free money” is over. The question now is whether consumers—and the economy—can adapt.

Related reading