{kind=link}

Credit Card Debt Trends: A Look at the Current U.S. Household Debt Landscape

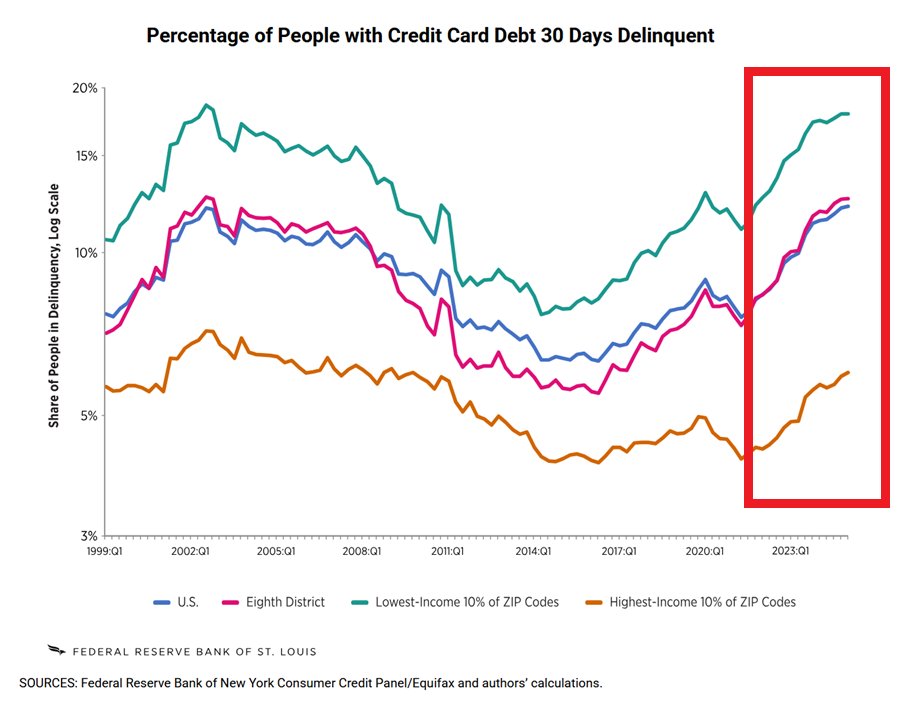

The financial health of the American consumer is once again under the microscope as new data from the Federal Reserve Bank of New York reveals the current state of credit card obligations. As of the first quarter of 2026, Americans collectively owe $1.25 trillion on their credit cards.

While this figure remains substantial, it reflects a shift in borrowing patterns. According to the New York Fed, credit card balances decreased by $25 billion during the first three months of 2026. This trend aligns with typical seasonal patterns, as consumers often reduce their credit card spending following the peak holiday shopping season at the end of the year.

Understanding the Current Debt Environment

Although credit card balances saw a slight quarter-over-quarter decline, the broader picture of household debt remains complex. The Federal Reserve Bank of New York noted that while credit card balances experienced a seasonal dip, other forms of debt—including mortgage debt, auto loans, and home equity lines of credit—trended upward during the same period.

Daniel Mangrum, a research economist at the New York Fed, stated that “household debt levels rose slightly, with modest increases in most debt types offsetting a seasonal decline in credit card balances.”

Despite the recent decrease in credit card debt, the year-over-year comparison highlights a persistent upward trajectory. Total credit card debt remains 5.9% higher than it was at the same time last year. For many households, this financial pressure is compounded by the rising cost of essential goods, such as fuel, which continues to impact personal budgets.

Key Takeaways for Consumers

- Seasonal Fluctuations: Credit card debt often ticks higher during the holiday season and typically retreats in the first quarter of the year.

- Diversified Debt: While credit card balances saw a temporary reduction, other categories such as mortgages and auto loans continue to contribute to overall household debt levels.

- Year-Over-Year Growth: Despite recent quarterly declines, the total volume of credit card debt is higher compared to the same period in the previous year.

Frequently Asked Questions

Why does credit card debt usually fall in the first quarter?

Credit card balances often rise toward the end of the year due to increased holiday-related spending. As the new year begins, consumer spending patterns typically normalize, leading to a seasonal decrease in outstanding balances.

What other types of debt are increasing?

Recent data indicates that mortgage debt, auto loans, and home equity lines of credit have seen increases, offsetting the seasonal decline observed in credit card debt.

How does the current debt level compare to last year?

Although there was a $25 billion decrease in the first quarter of 2026, total credit card debt is 5.9% higher than it was a year ago, according to the Federal Reserve Bank of New York.

Looking Ahead

Monitoring household debt is essential for understanding the resilience of the U.S. Economy. While the recent decline in credit card balances provides a momentary reprieve, the persistent year-over-year growth suggests that consumers remain heavily reliant on credit. As economic conditions evolve, keeping a close watch on delinquency rates and total debt accumulation will be vital for both individual financial planning and broader market analysis.