{kind=link}

US Existing Home Sales Stall in April as Mortgage Rates Surge

The U.S. Housing market hit a wall in April, delivering a lackluster performance during what is traditionally the busiest season for homebuying. While analysts expected a significant spring bounce, the reality was a near-flat trajectory, leaving the market in a state of malaise.

- Sales Volume: Existing home sales rose just 0.2% in April to a seasonally adjusted annual rate of 4.02 million units.

- Price Peaks: The median sales price hit an all-time April high of $417,700, up 0.9% year-over-year.

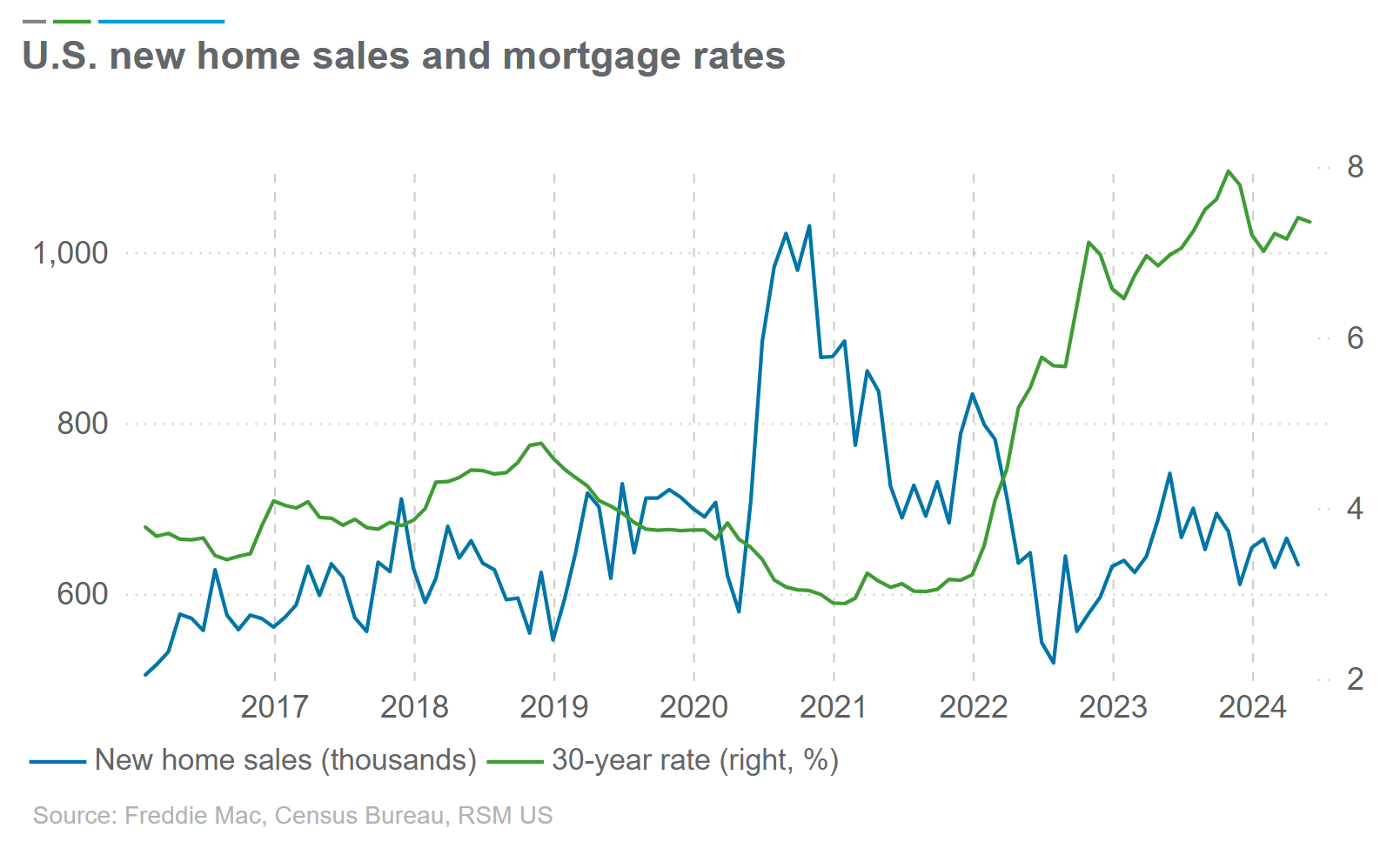

- Rate Shock: Mortgage rates spiked in April following the start of the U.S.-Israel war with Iran.

- Inventory Tightness: Supply rose to 4.4 months, still well below the 6-month threshold required for a balanced market.

April Sales Miss Expectations

The National Association of Realtors (NAR) reported that sales of previously owned homes were essentially flat in April. The 0.2% month-over-month increase fell sharply short of the 3% gain housing analysts had anticipated. This trend continues a broader slump that began in 2022, with sales hovering near a 4-million annual pace—far below the historic norm of roughly 5.2 million.

While sales remained unchanged compared to April of the previous year, the market is struggling to find momentum. This stagnation is particularly concerning given the typical spring surge in buyer activity.

Prices Hit Record April Highs

Despite the drop in sales volume, home prices aren’t falling. The U.S. Median sales price increased 0.9% from a year earlier to $417,700. According to NAR data, this represents the highest median price ever recorded for the month of April since records began in 1999.

Home prices have now risen on an annual basis for 34 consecutive months. This persistent price growth, combined with high borrowing costs, continues to squeeze buyers and limit overall market liquidity.

The Mortgage Rate Catalyst

The primary driver behind the April disappointment was a sudden shift in borrowing costs. The average rate on the 30-year fixed mortgage ended March in the high 5% range, but shot up sharply in April. This surge was triggered by geopolitical instability stemming from the start of the U.S.-Israel war with Iran.

Lawrence Yun, chief economist for NAR, noted that while average income growth has been outpacing home price gains and affordability had been improving, these macroeconomic signals were offset by the volatility in mortgage rates.

The Inventory Deadlock

Inventory levels provided a little glimmer of movement, rising 5.8% from March. However, the year-over-year increase was a meager 1.4%, bringing the total supply to 4.4 months. In a balanced market, a six-month supply is typically required to prevent sellers from holding too much leverage.

Yun emphasized that the market needs roughly 30% growth in inventory to truly stabilize. While multiple-offer scenarios are less intense than they were a few years ago, they still occur frequently. At the same time, homes are spending more days on the market, suggesting that consumers are becoming more hesitant and cautious before committing to a purchase.

Frequently Asked Questions

Why are home prices still rising if sales are flat?

Prices remain high because inventory is still critically low. With a 4.4-month supply, there aren’t enough homes to meet existing demand, which keeps upward pressure on prices even as the total number of transactions drops.

How did geopolitical events affect the housing market?

Geopolitical conflict, specifically the U.S.-Israel war with Iran, led to a sharp increase in 30-year fixed mortgage rates in April. Higher rates increase the monthly cost of a loan, which pushes many potential buyers out of the market or forces them to pause their search.

What is a “balanced market” in real estate?

A balanced market is one where neither buyers nor sellers have a distinct advantage. This is generally achieved when there is a six-month supply of homes available for sale.

Looking Ahead

The U.S. Housing market remains in a delicate position. While income growth and modest inventory gains are helping, they are currently being neutralized by volatile mortgage rates and record-high prices. Until inventory sees a more substantial increase or mortgage rates stabilize, the “spring bust” may transition into a prolonged period of stagnation for existing home sales.

Worth a look