{kind=link}

As of late 2024, American households hold record levels of liquid assets in money-market funds and certificates of deposit (CDs), totaling over $6.5 trillion, according to data from the Federal Reserve. While these vehicles provided attractive, low-risk yields during the Federal Reserve’s aggressive rate-hiking cycle, the transition to a lower-interest-rate environment is eroding “real” returns, forcing savers to reevaluate their cash-heavy strategies as inflation continues to outpace net gains.

The Shift in Money-Market Fund Dynamics

Money-market funds have acted as a primary destination for retail and institutional cash since the Federal Reserve began raising the federal funds rate in March 2022. According to the Investment Company Institute, total assets in money-market funds reached an all-time high of $6.51 trillion in October 2024. Investors moved capital into these funds to capture yields that briefly exceeded 5% while keeping liquidity high.

However, the landscape is shifting. Following the Federal Reserve’s decision to cut interest rates by 50 basis points in September 2024, yields on these funds began a downward trajectory. Unlike long-term bonds, money-market funds adjust their holdings—typically short-term Treasury bills and commercial paper—almost immediately to reflect current market rates. Consequently, as the central bank eases monetary policy, the “carry” on these cash piles is shrinking, reducing the passive income many households grew accustomed to over the past 18 months.

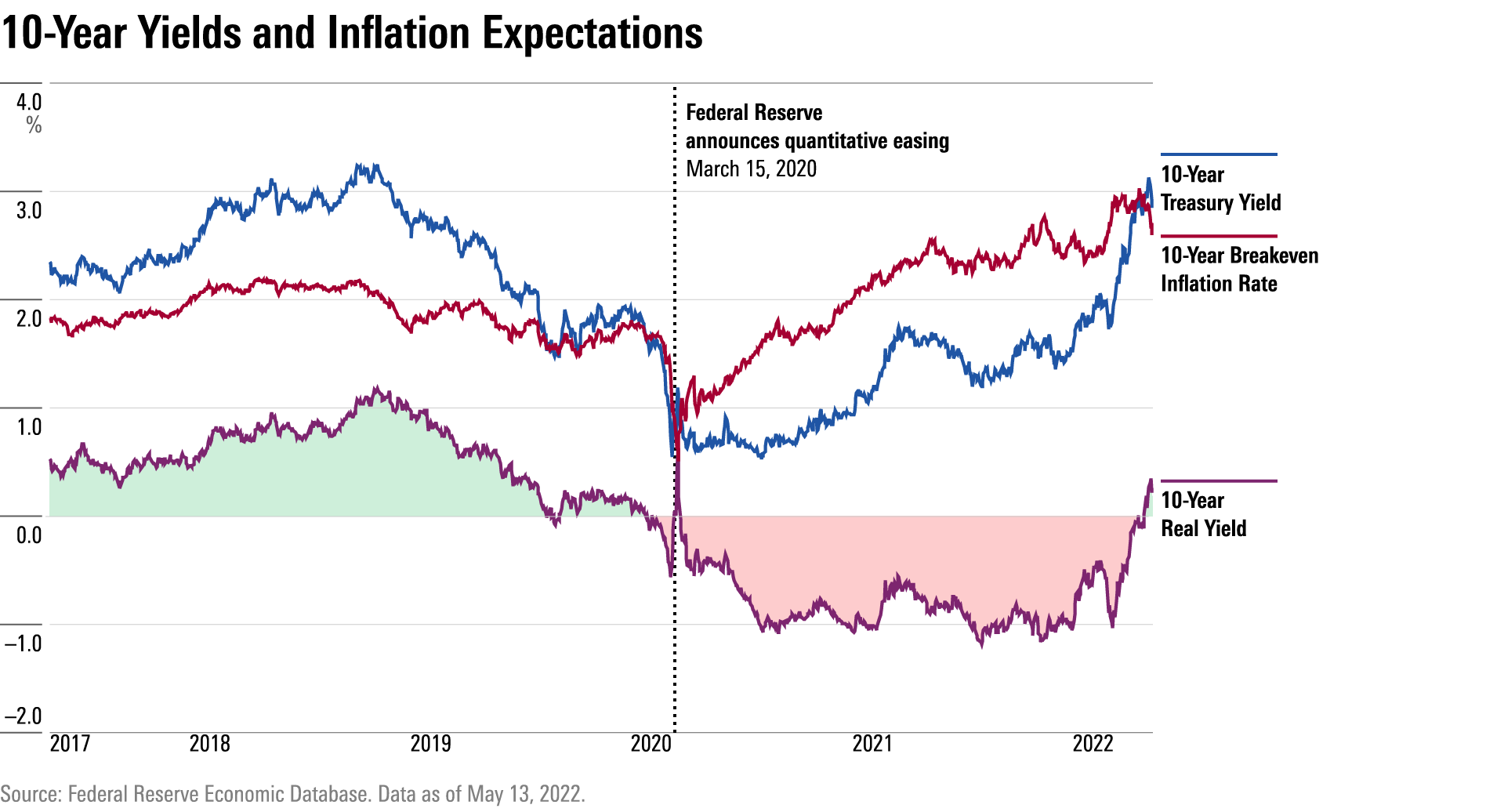

Real Yields and the Inflation Factor

The “real” yield—the nominal interest rate minus the inflation rate—is the metric that determines whether a cash position is actually growing in purchasing power. With the Bureau of Labor Statistics reporting a Consumer Price Index (CPI) increase of 2.4% for the 12 months ending September 2024, cash held in accounts yielding 3% or less is barely keeping pace with the rising cost of goods and services.

When investors account for taxes on interest income, many are effectively experiencing negative real returns. For an investor in a 24% federal tax bracket, a 4% yield is reduced to a 3.04% after-tax return. When compared against core inflation, this leaves little to no margin for wealth accumulation. This environment creates a “cash trap,” where the safety of money-market funds and CDs comes at the cost of long-term capital erosion.

Comparison: CDs vs. Money-Market Funds

Investors often choose between money-market funds and CDs based on their need for liquidity versus their desire to lock in a specific rate. The following table highlights the structural differences currently influencing investor behavior:

| Feature | Money-Market Funds | Certificates of Deposit (CDs) |

|---|---|---|

| Liquidity | High (daily access) | Low (early withdrawal penalties) |

| Rate Structure | Variable (follows Fed policy) | Fixed (locked at opening) |

| Risk Profile | Low (not FDIC insured) | Very Low (FDIC insured) |

While money-market funds offer immediate access, CDs have become a preferred tool for those looking to “lock in” current rates before further expected cuts by the Federal Reserve. According to the FDIC, while national average rates on savings accounts remain low, some institutions continue to offer competitive promotional rates on longer-term CDs to attract deposits.

What Happens Next for Savers

The primary risk for investors currently holding excess cash is the “reinvestment risk.” As short-term rates decline, the income generated by these massive cash reserves will continue to fall. Financial analysts, including those at Goldman Sachs, suggest that the Federal Reserve will likely continue a gradual path of normalization, which implies that the era of “easy money” from cash accounts is ending.

For individuals, the decision to remain in cash involves balancing the need for an emergency fund against the opportunity cost of missing out on potential returns in other asset classes. As real yields turn negative, many investors are expected to shift a portion of their liquidity into intermediate-term bonds or dividend-paying equities to maintain their purchasing power, a trend that typically follows the conclusion of a central bank’s tightening cycle.