{kind=link}

Navigating the Compliance Burden: Global Systemically Crucial Banks and U.S. Surcharge Proposals

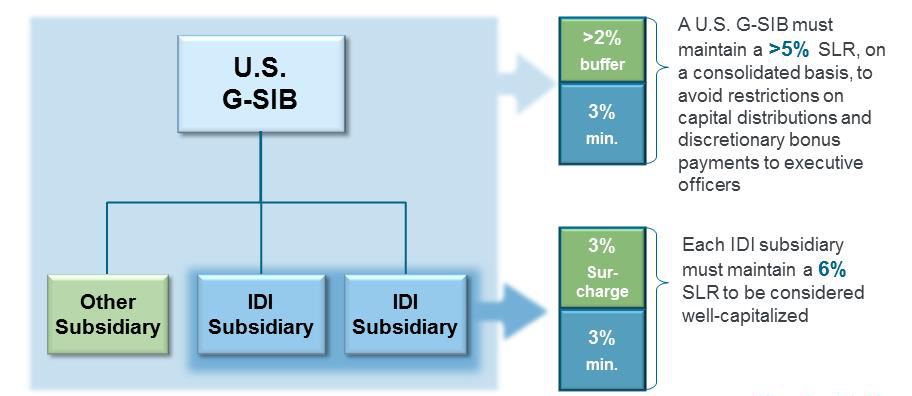

For Global Systemically Important Banks (G-SIBs), the regulatory landscape is shifting once again. As financial authorities refine capital requirements to bolster systemic stability, a new proposal regarding U.S. Surcharges has emerged as a significant operational hurdle. For these major institutions, the challenge isn’t just the capital cost itself—it’s the daily, granular data management required to remain in compliance.

The Data Management Challenge

The core of the issue lies in the complexity of calculating systemic risk scores. G-SIBs are evaluated based on a variety of indicators, including size, interconnectedness, complexity, and cross-jurisdictional activity. When regulators propose adjustments to how these surcharges are calculated, banks must pivot their internal reporting systems to capture, aggregate, and validate vast amounts of data on a daily basis.

For many global banks, this creates a “data headache.” Internal systems often struggle to reconcile disparate data streams across international borders, especially when regulatory definitions of “exposure” or “complexity” change. The administrative burden of ensuring that every transaction is correctly categorized to satisfy U.S. Regulatory standards often requires an overhaul of existing risk management infrastructure.

Why Surcharges Matter

Surcharges are designed to ensure that the largest, most interconnected financial institutions hold enough capital to absorb potential losses, thereby protecting the broader economy. By increasing the cost of being a G-SIB, regulators aim to discourage excessive risk-taking and incentivize firms to simplify their corporate structures.

However, the operational reality for these banks is that compliance is not a one-time setup. It is a continuous cycle of:

- Data Granularity: Ensuring that daily reporting reflects the most accurate picture of firm-wide exposure.

- System Integration: Linking global branches and subsidiaries to a centralized reporting hub that speaks the language of U.S. Regulators.

- Validation and Audit: Maintaining a clear, defensible audit trail for every calculation, which is essential to avoid regulatory scrutiny.

Key Takeaways for Market Participants

As the industry navigates these proposed changes, several factors remain critical for investors and bank management teams:

- Increased Operational Costs: The cost of compliance is rising, driven by the need for more sophisticated data management tools and human capital.

- Capital Allocation Shifts: Banks may adjust their business models to reduce their systemic footprint, potentially leading to a retreat from certain high-complexity or high-exposure activities.

- Focus on Regulatory Technology (RegTech): Expect a surge in investment toward automated reporting solutions that can handle the volume and velocity of data required for modern capital surcharges.

Looking Ahead

The ongoing dialogue between regulators and the banking sector is essential to ensuring that capital requirements are effective without being unnecessarily stifling. For G-SIBs, the path forward requires a transition from manual, legacy reporting processes to agile, data-driven frameworks. While the “daily data headache” is a significant concern today, it also represents a necessary evolution toward a more transparent and resilient global financial system.

the ability to manage this data efficiently will likely become a competitive advantage. Institutions that can successfully integrate their regulatory reporting with their broader risk management strategy will be better positioned to navigate the evolving demands of the U.S. Financial landscape.