{kind=link}

Thomas Brown, portfolio manager of the Chielliga Valley Fund, weighed in, saying, “The two most important data for judging the Federal Reserve’s dual responsibilities of price stability and full employment are released simultaneously in one week.”

If there is a combination of employment statistics being weaker than expected and at the same time a clear slowdown in prices, there is room for expectations of the Federal Reserve to cut the policy interest rate. Conversely, if employment improves and a slowdown in prices is confirmed, expectations of a policy interest rate cut may recede.

Currently, the financial market expects interest rates to be lowered twice within the year, starting with the first cut in June. “Interest rate expectations have been surprisingly stable in recent weeks,” said Angelo Kirkapas, chief global investment strategist at Edward Jones, but cautioned, “This week’s data has the potential to shatter that stability.”

◆If you can’t answer AI, ‘sell’

Macroeconomic indicators aren’t the only test this week. As the second half of the 4th quarter earnings season unfolds simultaneously, there is a possibility that the distinction between AI beneficiaries and victims, which was raised last week, will unfold again through individual company earnings disclosures this week.

Currently, the performance of companies is expected to be solid. According to FactSet, the growth rate of earnings per share for the stock index S&P 500 companies in the fourth quarter of last year is expected to be 13%, and according to UBS, it is 20% for Nasdaq companies. It is said to be 6% points higher than the previous figure.

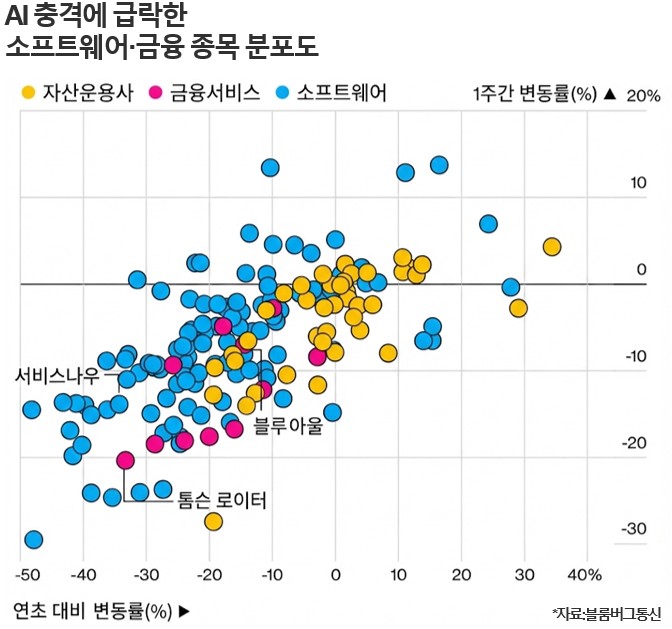

However, what the stock market showed last week is that the standards have changed. If a clear answer could not be given about AI, they reacted mercilessly by selling. For example, they began to demand ‘clear profitability’ for AI facility investment, which had previously been lenient, and of course began to doubt the viability of the software sector.

date: 2026-02-09 03:06:00

Worth a look