{kind=link}

Understanding DSCR Loans: How Rental Income Qualifies Borrowers

A Debt Service Coverage Ratio (DSCR) loan allows real estate investors to qualify for financing based on a property’s projected or actual rental income rather than the borrower’s personal income or employment history. According to Investopedia, lenders calculate the ratio by dividing a property’s net operating income by its total debt service. A ratio of 1.0 indicates the property generates exactly enough income to cover its mortgage payments, while a ratio above 1.0 signals surplus cash flow.

Calculating the Debt Service Coverage Ratio

Lenders use the DSCR as a primary metric to assess the risk of a commercial or investment property loan. The formula is straightforward: divide the property’s annual net operating income (NOI) by the annual mortgage debt service (principal and interest).

For example, if a property generates $120,000 in annual rental income and has $100,000 in annual debt obligations, the DSCR is 1.2. Most conventional lenders typically require a minimum DSCR between 1.2 and 1.25 to approve a loan. This threshold ensures a safety buffer if rental income fluctuates or unexpected expenses arise. As noted by the Office of the Comptroller of the Currency (OCC), this assessment remains a cornerstone of commercial real estate underwriting, as it focuses on the asset’s ability to sustain its own financing.

Advantages for Real Estate Investors

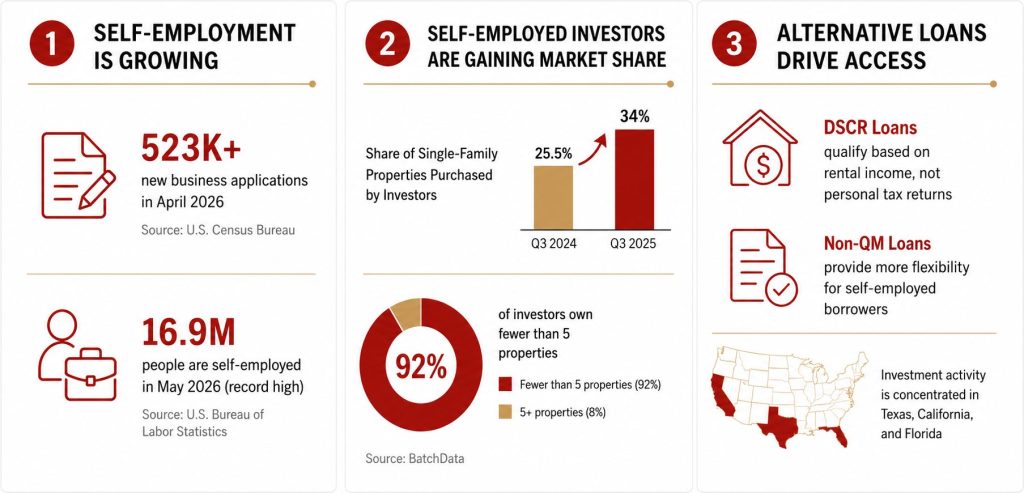

The primary appeal of DSCR loans is the removal of traditional income verification requirements. Borrowers are not required to provide tax returns, W-2s, or pay stubs. This structure is particularly beneficial for:

* Self-Employed Investors: Individuals with complex tax filings or write-offs that may lower their “qualifying” income on paper.

* Portfolio Expansion: Investors who have reached the limit of conventional loans and need to scale their holdings.

* Speed of Closing: Because the underwriting process focuses on the property’s financial performance rather than the borrower’s personal credit history, the approval timeline is often faster than traditional residential mortgages.

While these loans offer flexibility, they often come with higher interest rates and larger down payment requirements compared to primary residence mortgages. Lenders typically require down payments ranging from 20% to 25% to mitigate the increased risk associated with non-traditional documentation.

Key Differences: DSCR Loans vs. Conventional Mortgages

| Feature | DSCR Loan | Conventional Mortgage |

| :— | :— | :— |

| Primary Qualification | Property Rental Income | Borrower Debt-to-Income (DTI) |

| Income Verification | Not Required | Required (Tax returns, W-2s) |

| Down Payment | Typically 20%–25% | Can be as low as 3%–5% |

| Interest Rates | Generally Higher | Generally Lower |

Risks and Market Considerations

Investors should remain aware that relying solely on property performance carries inherent risks. If a property experiences high vacancy rates or requires significant capital expenditures, the DSCR may drop below the lender’s required threshold. If the ratio falls below 1.0, the borrower must cover the shortfall out of pocket, which can strain personal liquidity.

Before committing to a DSCR loan, investors should conduct rigorous due diligence on local rental market trends and vacancy rates. As the Federal Reserve has noted in guidance regarding commercial real estate, fluctuations in market conditions directly impact the income-generating potential of investment properties, making accurate projections essential for long-term loan sustainability.

Keep reading