{kind=link}

Understanding General Obligation Bonds and Municipal Debt

General obligation (Head) debt is a primary tool used by local governments to finance the infrastructure and services that sustain a community. Unlike revenue bonds, which are paid back by specific project earnings, GO debt is backed by the taxing power of the issuing entity, meaning it is paid directly through taxpayer dollars. These funds are typically used to support essential services and operations.

How General Obligation Debt Works

At its core, general obligation debt allows a municipality to borrow large sums of money for public works. Because the debt is secured by the issuer’s ability to levy taxes, it is often viewed as a stable investment. However, this reliance on taxpayer funds means that the financial burden of this debt can limit a city’s ability to invest in other critical areas until the obligations are met.

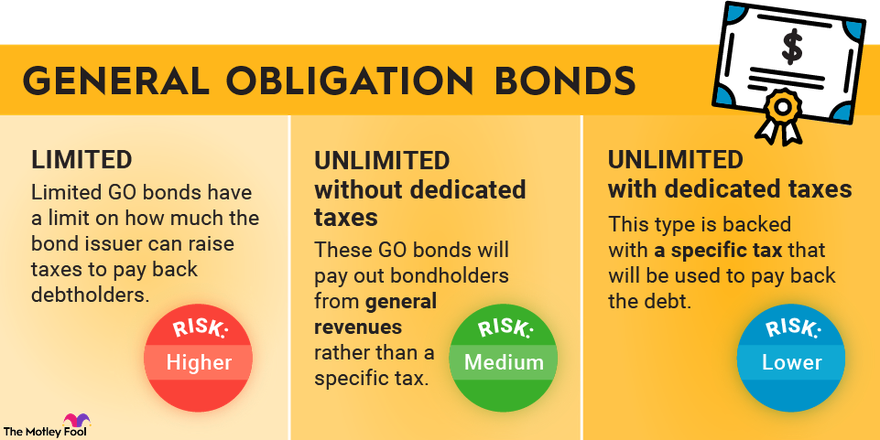

Types of GO Pledges

Not all general obligation bonds are structured the same. Some utilize a limited-tax general obligation pledge. In this arrangement, the issuing local government is asked to raise property taxes if it becomes necessary to meet existing debt service obligations. Such increases are typically bound by specific legal limits.

Legal Constraints and Debt Limits

To prevent over-borrowing and protect taxpayers, many jurisdictions implement strict debt limits. Using the Ohio Revised Code as a framework, these limits are generally categorized into two types:

- Direct Debt Limit: These are limitations on the principal amount of net indebtedness that a township, county, school district, or municipal corporation can incur.

- Indirect Debt Limit: This refers to limitations on the issuance of unvoted certificates of indebtedness, notes, or general obligation bonds. These limits result from restrictions on the amount of unvoted taxes that can be levied annually on general tax lists.

Further restrictions may include a “Ten-mill limit,” which refers to unvoted taxes of ten mills annually on each dollar of property tax valuation, or a “One per cent limit,” where unvoted taxes amount to one percent annually of the true money value of listed property.

The Real-World Impact of Bond Management

Effective management of GO debt can lead to significant financial advantages for the public, while poor management can create long-term burdens.

Taxpayer Savings

Strategic bond sales can reduce the cost of borrowing. For example, the California Treasurer’s Office reported that taxpayers saved millions of dollars after the agency sold more than $2 billion worth of general obligation bonds.

Path to Debt-Free Status

While GO debt is a useful tool, paying it off unlocks municipal budgets. One Metro Detroit city recently became debt-free after spending 16 years paying off $14 million in general obligation debt, removing a financial burden that had previously limited its investment capabilities.

Key Takeaways

- Funding Source: GO debt is paid directly by taxpayers to fund essential operations.

- Tax Flexibility: Limited-tax pledges may allow governments to raise property taxes within legal bounds to service debt.

- Regulatory Guards: Direct and indirect debt limits exist to control the amount of indebtedness a local government can incur.

- Fiscal Impact: While bond sales can save taxpayers millions, long-term debt can restrict a city’s ability to invest in new projects.