{kind=link}

Timing Your Social Security: The Strategic Trade-off Between Age 62 and 70

Deciding when to claim Social Security benefits is one of the most consequential financial decisions a retiree will ever make. It isn’t just about choosing a start date; it’s a complex calculation involving longevity, health, current assets, and the desire for a guaranteed inflation-adjusted income stream.

The fundamental tension lies between the immediate gratification of early payments and the long-term security of a maximized monthly check. While claiming at 62 provides an immediate cash flow, it comes with a permanent reduction in benefits. Conversely, waiting until 70 maximizes the monthly payment but requires you to fund your lifestyle through other means for nearly a decade.

The Baseline: Understanding Full Retirement Age (FRA)

To understand the trade-off, you first necessitate to identify your Full Retirement Age (FRA). The FRA is the age at which you are entitled to 100% of your primary insurance amount. For anyone born in 1960 or later, the FRA is 67.

Your FRA serves as the anchor for all benefit calculations. If you claim before this age, your benefits are reduced; if you claim after, they are increased.

Claiming at 62: The Cost of Early Access

Age 62 is the earliest you can claim retirement benefits. However, this convenience carries a steep price. If your FRA is 67 and you claim at 62, your monthly check is permanently reduced by roughly 30%.

Choosing this path is often a necessity for those facing health challenges, urgent financial hardship, or those who believe their life expectancy is significantly shorter than the average. However, from a purely mathematical standpoint, claiming at 62 is a bet that you won’t live long enough to reach the break-even point

—the age where the total cumulative benefits of a larger, delayed check surpass the total amount collected from an earlier, smaller check.

Claiming at 70: The Power of Delayed Credits

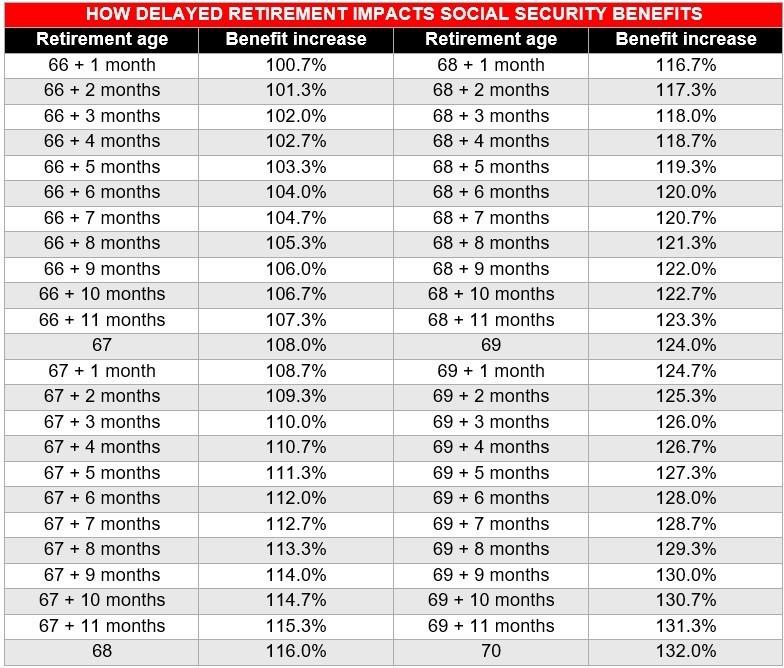

For those who can afford to wait, the rewards are substantial. Beyond your FRA, the Social Security Administration applies delayed retirement credits. These credits increase your benefit by 8% for every full year you delay claiming, up until age 70.

If your FRA is 67 and you wait until 70, your monthly benefit will be 24% higher than it would have been at 67. When compared to the reduced check you would have received at 62, the difference in monthly income can be staggering, often resulting in a check that is 70% to 80% larger than the age-62 amount.

“The decision to delay Social Security benefits to age 70 is essentially buying a larger annuity that is indexed for inflation, providing a powerful hedge against longevity risk.” Marcus Liu, Business Editor

Strategic Comparison: 62 vs. FRA vs. 70

The following table illustrates the impact of timing based on a hypothetical Full Retirement Age of 67.

| Claiming Age | Benefit Percentage | Primary Advantage | Primary Disadvantage |

|---|---|---|---|

| 62 | ~70% of FRA | Immediate cash flow; more years of payments. | Permanently lower monthly check. |

| 67 (FRA) | 100% of FRA | Full benefit entitlement. | Missed opportunity for delayed credits. |

| 70 | ~124% of FRA | Maximum possible monthly payment. | Requires other funding sources until age 70. |

Key Considerations for Your Decision

Numbers alone don’t tell the whole story. To determine your optimal claiming age, consider these three variables:

- Health and Longevity: If you have a family history of longevity, waiting until 70 is almost always the superior financial move. If you have chronic health issues, claiming early ensures you actually receive the benefits you paid into.

- Other Income Sources: If you have a robust 401(k), IRA, or pension, you can use those assets to “bridge” the gap to age 70, allowing your Social Security benefit to grow.

- Spousal and Survivor Benefits: Your claiming age affects your spouse. If you are the higher earner, delaying your benefit increases the survivor benefit your spouse will receive if you pass away first.

Frequently Asked Questions

What is the “break-even” age?

The break-even age is the point where the total money received from waiting until 70 exceeds the total money received by starting at 62. While this varies based on individual benefit amounts, it typically occurs in the late 70s or early 80s. If you expect to live past 82, waiting usually pays off.

Can I change my mind after I start claiming?

Yes, but with limits. You can stop benefits and request that they be reinstated later, but you may have to pay back some of the benefits you already received. You cannot claim “delayed credits” for the time you were already receiving benefits.

Does working while claiming early reduce my check?

Yes. If you claim benefits before your FRA and earn more than the annual earnings limit, the SSA will temporarily withhold a portion of your benefits. Once you reach FRA, these withheld benefits are recalculated and added back to your monthly check.

Final Takeaway

There is no one-size-fits-all answer to the Social Security puzzle. Claiming at 62 is a strategy for immediate liquidity and short-term need; claiming at 70 is a strategy for long-term wealth maximization and insurance against outliving your savings. The most successful retirees don’t just appear at the monthly check—they look at their entire portfolio and their projected lifespan to decide which lever to pull.

Worth a look