{kind=link}

Why Most Retirees Rely on Social Security, Not IRAs, for Retirement Income

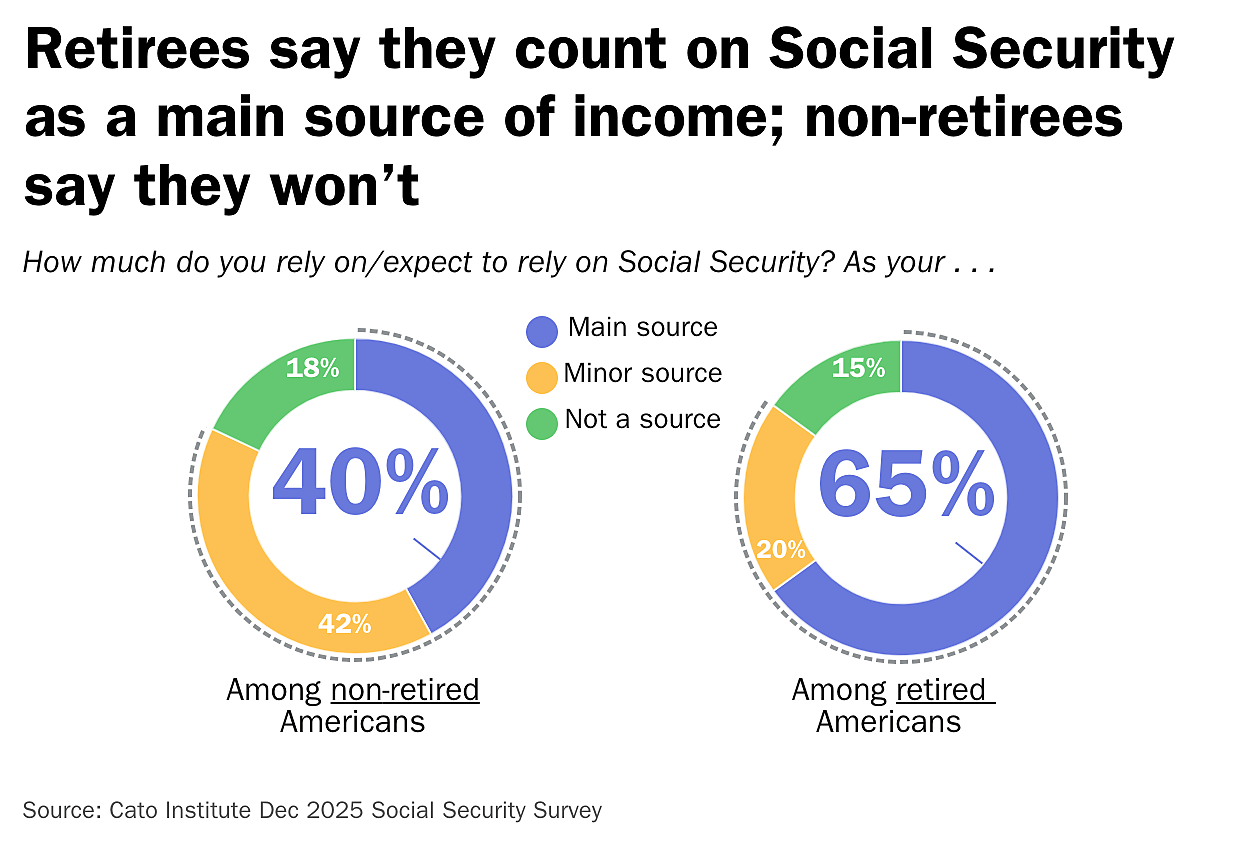

Over 60% of retirees in the United States depend on Social Security as their primary source of income, according to the Social Security Administration (SSA), despite the widespread promotion of Individual Retirement Accounts (IRAs) as a retirement savings tool. This discrepancy highlights a gap between financial planning advice and real-world retirement outcomes.

The Role of Social Security in Retirement Income

Social Security provides a guaranteed monthly payment to eligible retirees, making it a critical component of financial stability. The program, established in 1935, is funded through payroll taxes and is designed to replace a portion of pre-retirement earnings. In 2023, the average monthly benefit was $1,839, according to the SSA, offering a baseline for many seniors.

“Social Security is the bedrock of retirement security for millions,” said Sarah Smith, a senior policy analyst at the AARP. “It’s a predictable income stream that doesn’t fluctuate with market conditions, which is especially important for those with limited savings.”

Challenges with IRA Adoption

Despite the tax advantages of IRAs, participation remains uneven. The IRS reports that only 28% of U.S. households had an IRA in 2022, with lower-income individuals less likely to contribute. Factors include lack of employer-sponsored plans, financial constraints, and limited financial literacy.

“Many workers don’t have access to employer-sponsored retirement plans, and without automatic enrollment, they’re less likely to save,” said Dr. Michael Chen, an economist at the University of Chicago. “IRAs require proactive management, which can be a barrier for some.”

Comparing Social Security and IRAs

Social Security and IRAs serve different purposes. While the former offers a stable, inflation-adjusted income, the latter allows for tax-deferred growth but carries market risks. For example, a 65-year-old retiring in 2023 with a $500,000 IRA could expect a withdrawal rate of 4% ($20,000 annually), compared to an average Social Security benefit of $22,000 per year.

However, IRAs can supplement Social Security, especially for higher earners. The 2023 maximum contribution limit for IRAs is $6,500, with an additional $1,000 allowed for those aged 50 and older. Yet, these limits may not suffice for those with higher living expenses.

Strategies for Balanced Retirement Planning

Financial advisors recommend a diversified approach, combining Social Security with IRAs, 401(k)s, and other investments. The SSA advises retirees to delay claiming benefits until full retirement age (66 or 67) to maximize payments.

“Retirement planning isn’t one-size-fits-all,” said Lisa Nguyen, a certified financial planner. “It’s about understanding your needs and leveraging all available tools, from Social Security to tax-advantaged accounts.”

What’s Next for Retirement Security?

Policymakers are exploring reforms to bolster retirement savings, including expanding access to automatic enrollment in workplace plans and increasing IRA contribution limits. A 2023 proposal by the Biden administration aimed to raise the IRA limit to $10,000 annually, though it faces legislative hurdles.

As the population ages, the reliance on Social Security is expected to grow. The SSA projects that by 2035, 75% of retirees will depend on the program for at least 50% of their income, underscoring its role as a cornerstone of retirement security.