{kind=link}

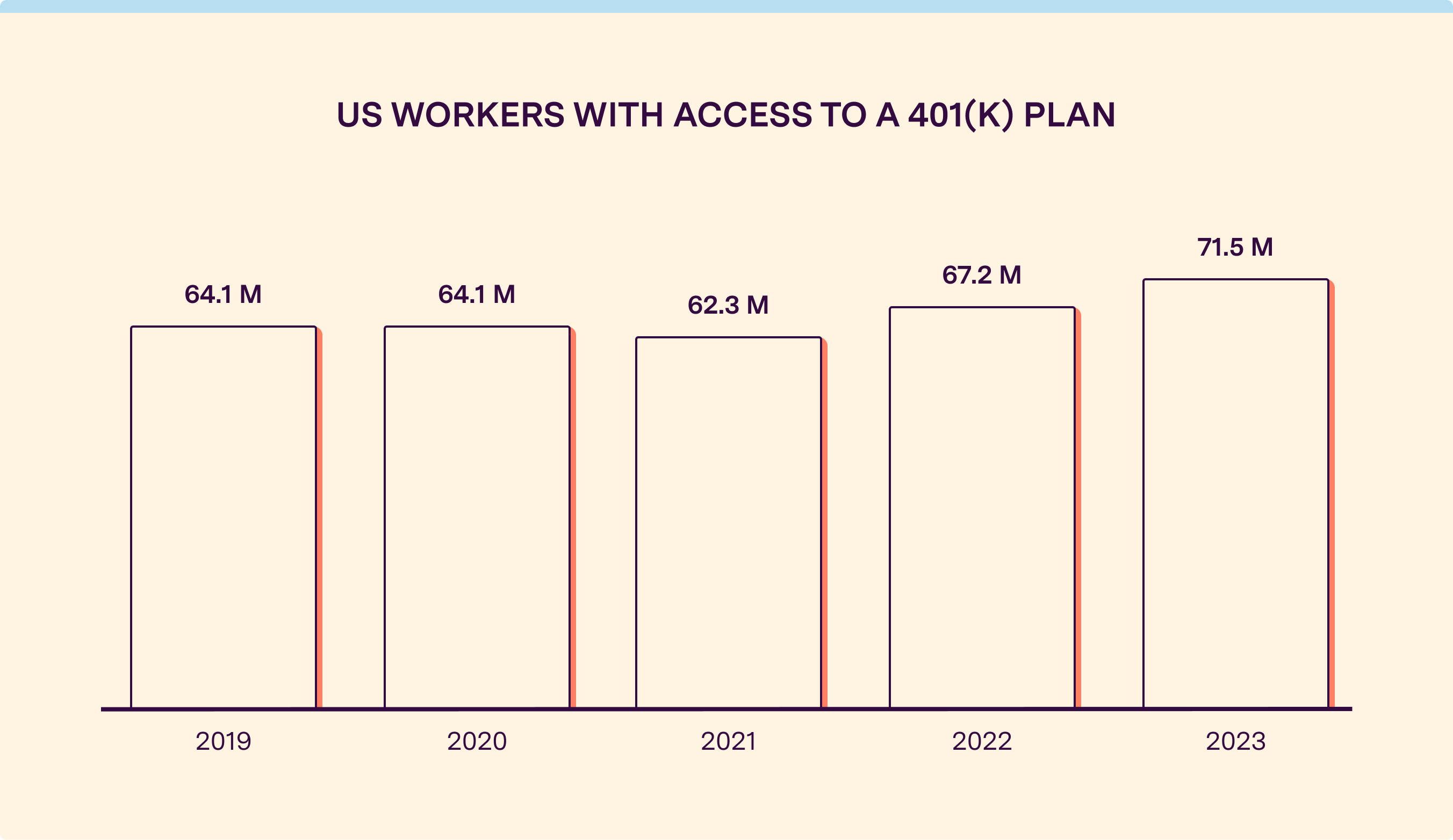

Approximately 56 million U.S. workers lack access to employer-sponsored retirement plans like 401(k)s, according to a report by AARP. This gap leaves a significant portion of the workforce reliant on Social Security or individual savings, increasing the risk of retirement insecurity as the U.S. population ages.

The Scale of the Retirement Savings Gap

The AARP findings highlight a systemic failure in retirement infrastructure. While 401(k) plans are a staple of corporate benefits, they aren’t universal. A large segment of the workforce—particularly those in small businesses, the gig economy, and part-time roles—don’t have a vehicle to save for the future with tax advantages.

According to the Bureau of Labor Statistics (BLS), the prevalence of employer-sponsored retirement plans varies wildly by industry. Workers in the private sector are significantly less likely to have access to these plans than government employees, creating a tiered system of retirement readiness.

Why Millions Are Missing Out

The lack of 401(k) access isn’t usually a choice made by the employee, but a limitation of the employer. Small businesses often cite the administrative cost and complexity of setting up a plan as primary barriers. For many “solopreneurs” and freelancers, the only option is an Individual Retirement Account (IRA), which lacks the employer-matching contributions that accelerate wealth building in a 401(k).

This disparity is most acute among low-wage workers. AARP notes that those without access to employer plans are often the same individuals who cannot afford to contribute to private IRAs due to immediate cost-of-living pressures.

Comparison: 401(k) vs. Individual Alternatives

For the 56 million workers without a company plan, the options are limited. The following table compares the primary vehicles available to these workers against the traditional 401(k).

| Feature | Employer 401(k) | Traditional/Roth IRA | Social Security |

|---|---|---|---|

| Employer Match | Often available | None | N/A |

| Contribution Limit | High (Annual cap set by IRS) | Lower (Annual cap set by IRS) | Based on earnings |

| Management | Employer-selected provider | Self-directed | Government-managed |

The Impact of the SECURE 2.0 Act

To combat this gap, the U.S. government passed the SECURE 2.0 Act. This legislation aims to make it easier for small businesses to start retirement plans by providing tax credits to employers who establish them. It also introduces “auto-enrollment” requirements for new plans, which removes the friction of manual sign-ups that often prevents workers from participating.

Despite these legislative efforts, the transition takes time. Many small firms still operate without formal plans, leaving their employees to navigate retirement planning independently.

Frequently Asked Questions

What is the difference between a 401(k) and an IRA?

A 401(k) is offered by an employer and often includes a company match. An IRA (Individual Retirement Account) is opened by the individual through a brokerage or bank. Both offer tax advantages, but 401(k)s generally have higher annual contribution limits.

Can freelancers get a 401(k)?

Yes. Self-employed individuals can open a “Solo 401(k),” which allows them to contribute as both the employer and the employee, though it requires more administrative setup than a standard IRA.

Does lack of a 401(k) mean no retirement?

No, but it means a higher reliance on Social Security. Without the compounded growth of a tax-advantaged investment account, workers may find their monthly Social Security checks insufficient to maintain their standard of living.

Outlook for the U.S. Workforce

The AARP data suggests that legislative fixes like SECURE 2.0 are necessary but insufficient on their own. The growth of the “gig economy” continues to outpace the creation of portable benefit systems. Until retirement savings are decoupled from specific employers and tied more closely to the individual worker, the gap for those 56 million people is likely to persist.

Worth a look