{kind=link}

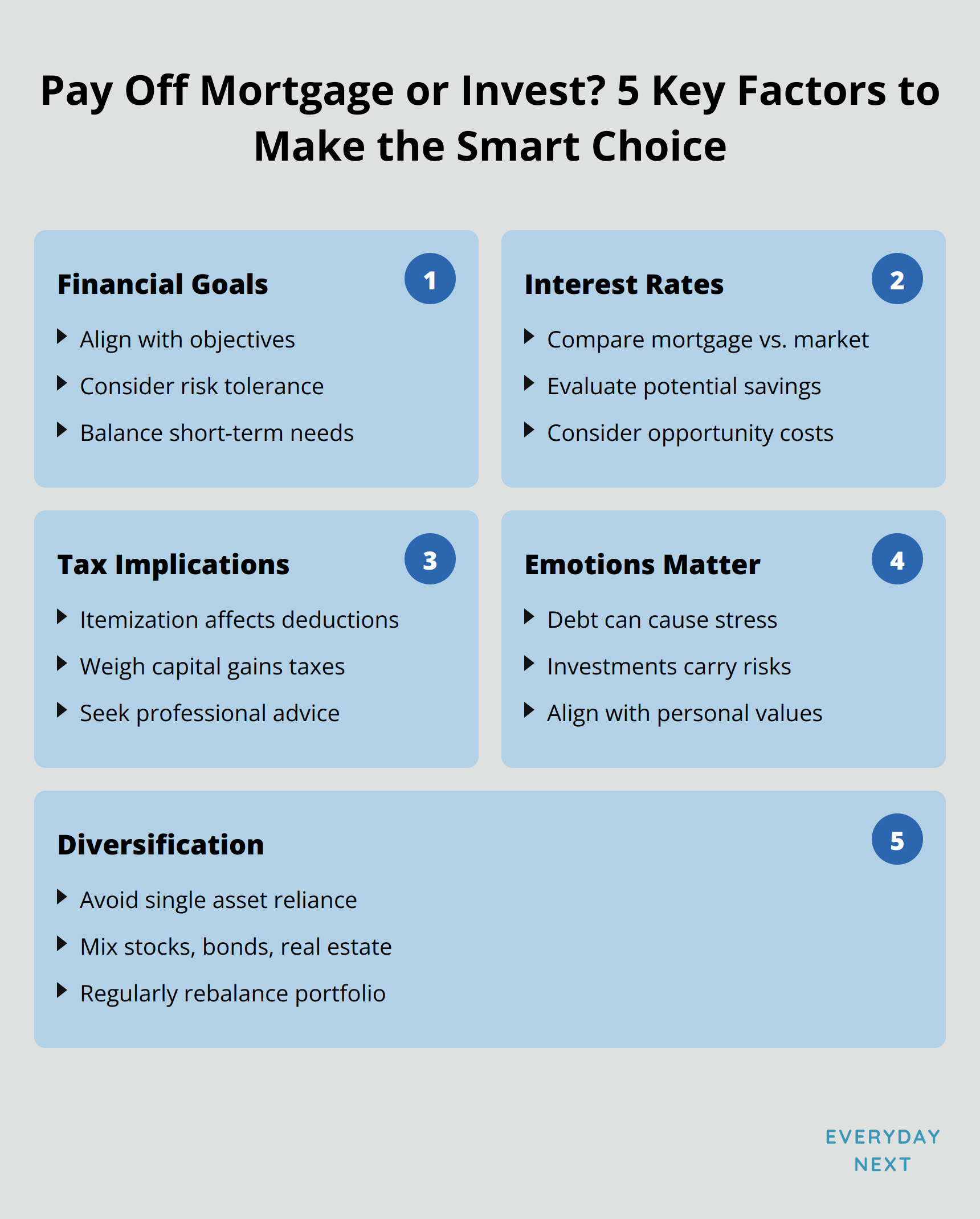

Deciding between paying off a mortgage early or investing surplus capital depends on the spread between your mortgage interest rate and potential market returns, adjusted for your personal tax situation and liquidity needs. While debt repayment offers a guaranteed, risk-free "return" equal to your interest rate, market investments historically offer higher long-term growth potential but carry volatility risks.

The Case for Early Mortgage Repayment

Paying down your mortgage is essentially a guaranteed investment with a return equal to your loan’s interest rate. According to the Consumer Financial Protection Bureau, this strategy eliminates a long-term liability, effectively lowering your monthly cost of living and reducing total interest paid over the life of the loan.

For homeowners with high-interest debt, this is often the most rational financial move. If your mortgage rate is 5% or 6%, you are effectively earning a 5% or 6% "return" on every dollar you put toward the principal. Because this return is tax-free—unlike interest earned in a savings account or dividends from a brokerage account—it provides a stable baseline for your net worth.

The Case for Market Investing

Investing your surplus funds in diversified assets, such as low-cost index funds or ETFs, historically yields returns that outpace most residential mortgage rates. The U.S. Securities and Exchange Commission notes that while stock market investments carry the risk of loss, they provide the potential for compound growth over long time horizons.

If your mortgage rate is low—for instance, fixed at 3% from a previous cycle—investing that same money in a market-tracking fund could theoretically yield 7% to 10% annually over a decade. By choosing this route, you maintain higher liquidity. Money tied up in home equity is "illiquid," meaning you cannot easily access it without a home equity line of credit (HELOC) or selling the property.

Critical Factors for Your Decision

To determine the right path, evaluate these three variables:

- Interest Rate Differential: If your mortgage rate is significantly lower than the expected return on a balanced portfolio, the mathematical advantage tilts toward investing. If your mortgage rate is high, the "guaranteed" savings of paying off debt become more attractive.

- Tax Implications: In some jurisdictions, mortgage interest may be tax-deductible, which lowers the effective cost of your debt. Conversely, investment gains are often subject to capital gains taxes, which can erode your net return. Review your local tax code or consult a tax professional to calculate your "after-tax" rate of return.

- Psychological Comfort: Financial decisions are not purely mathematical. For many, the peace of mind associated with being "debt-free" outweighs the potential for higher market gains. This is a personal risk tolerance question rather than a purely fiscal one.

Comparison Table: Debt vs. Investment

| Feature | Early Mortgage Repayment | Market Investing |

|---|---|---|

| Return | Guaranteed (equals interest rate) | Variable (market-dependent) |

| Liquidity | Low (trapped in home equity) | High (can sell assets) |

| Risk | None (debt is eliminated) | Market volatility |

| Tax Impact | Reduces interest deduction | Subject to capital gains tax |

Strategic Hybrid Approach

Many investors choose a middle ground. Rather than choosing one extreme, you can allocate a fixed percentage of monthly surplus toward extra mortgage principal while investing the remainder in a retirement or brokerage account. This "balanced" approach captures some of the long-term growth of the markets while steadily chipping away at your debt, providing both financial flexibility and a faster path to a fully owned home. Before making a decision, ensure you have an emergency fund covering three to six months of expenses; prioritizing debt repayment or investing should only occur once your short-term liquidity needs are secured.

Worth a look