{kind=link}

Mastering Commercial Real Estate: Essential Financial Metrics for Investors

For investors and developers, navigating the complexities of commercial real estate (CRE) requires more than just intuition; it demands a rigorous command of financial modeling. Whether you are evaluating a retail center, an office complex, or a multi-family asset, your ability to accurately assess value and risk is the primary determinant of your long-term success.

To make informed decisions, you must master the fundamental trio of commercial real estate analysis: Net Operating Income (NOI), Capitalization Rates (Cap Rates) and financing mathematics. These metrics provide the scaffolding for every successful deal, allowing you to move beyond speculation and into data-driven negotiation.

Understanding the Core Metrics

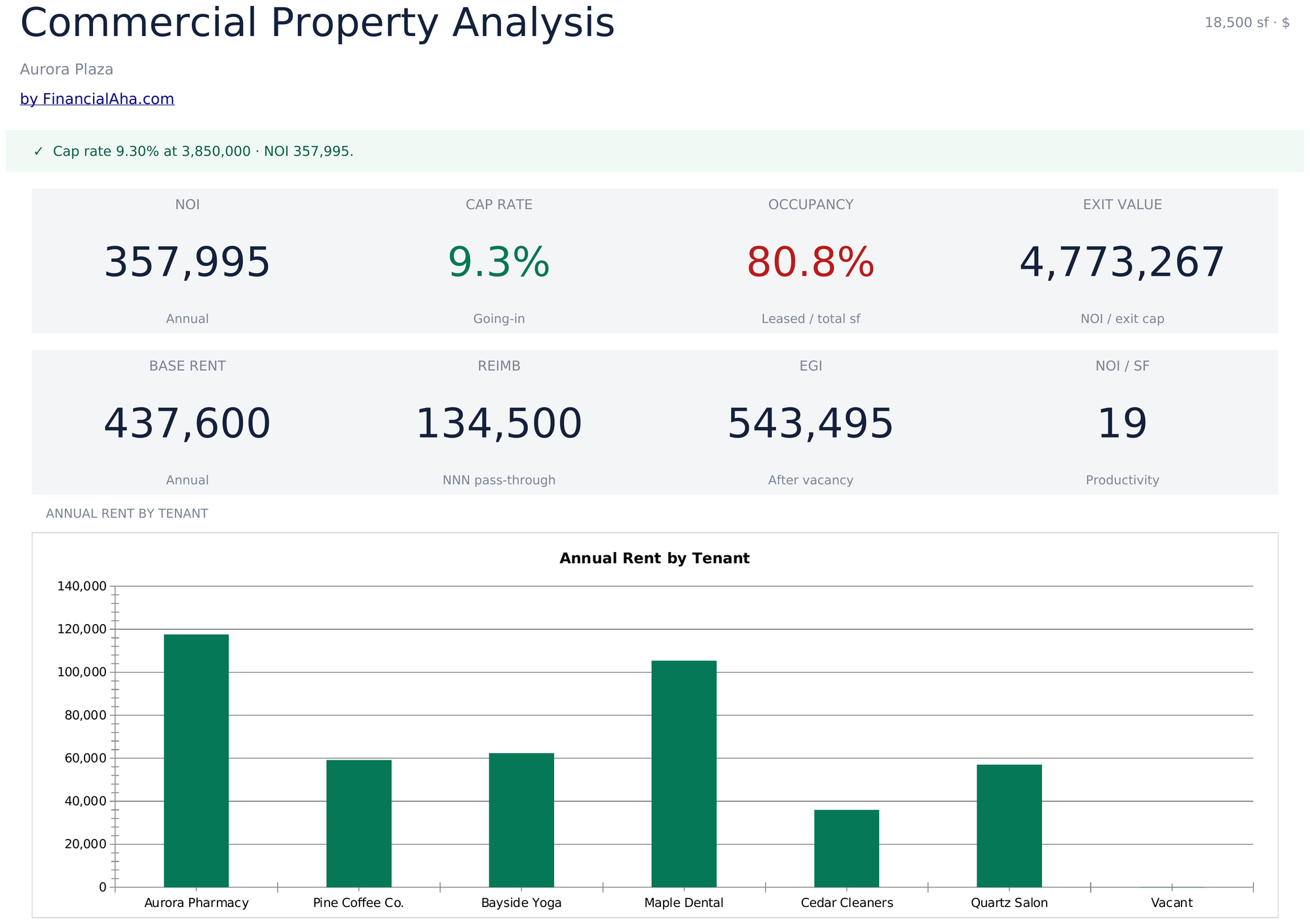

At the heart of every property valuation is the Net Operating Income, or NOI. This is the bedrock metric that reflects a property’s ability to generate cash flow. By subtracting operating expenses—such as property management fees, insurance, maintenance, and taxes—from the property’s gross income, you arrive at a clear picture of its operational efficiency.

The Role of the Capitalization Rate

Once you have established the NOI, the capitalization rate serves as the bridge to market valuation. The Cap Rate is calculated by dividing the property’s annual NOI by its current market value or purchase price. It functions as a snapshot of the asset’s yield, allowing investors to compare properties across different markets and sectors. A lower cap rate typically signals a lower-risk, highly desirable asset, while a higher cap rate may suggest greater risk or potential for value-add repositioning.

Financing Mathematics and Leverage

Rarely does an investor purchase a commercial asset with 100% equity. Understanding financing math—specifically debt service coverage ratios and loan-to-value (LTV) limits—is critical. These calculations dictate how much leverage you can safely apply to a deal without jeopardizing your cash-on-cash return. Proper analysis ensures that your debt structure aligns with the property’s income generation, protecting you against market volatility.

Key Takeaways for Successful Negotiation

- Focus on NOI Accuracy: Never rely on pro-forma projections without verifying historical operating expenses. Minor discrepancies in expense reporting can significantly inflate perceived value.

- Contextualize Cap Rates: Always compare the subject property’s cap rate against recent, comparable sales in the immediate submarket. A cap rate exists in a vacuum only until it meets the market.

- Model Multiple Scenarios: Use sensitivity analysis to stress-test your financing. How does your return profile change if vacancy rates increase or if interest rates shift by 50 basis points?

Frequently Asked Questions

Why is NOI more crucial than Gross Income?

Gross income fails to account for the costs of keeping an asset functional. NOI provides a “bottom-line” view of performance, which is exactly what lenders and institutional buyers prioritize when determining the price they are willing to pay.

How do interest rate fluctuations impact my valuation?

Because Cap Rates are often correlated with the cost of debt, rising interest rates generally put upward pressure on cap rates, which in turn leads to lower property valuations. Investors must stay attuned to macroeconomic trends to avoid overpaying in a shifting rate environment.

Strategic Outlook

The commercial real estate landscape remains a game of asymmetric information. Those who take the time to build robust, repeatable analytical models are the ones who consistently identify value where others see only risk. By mastering the interplay between NOI, cap rates, and financing, you transform from a casual market participant into a sophisticated investor capable of navigating even the most complex transactions with confidence.

Keep reading