For most U.S. households, a “comfortable” retirement requires annual expenditures ranging between varying amounts. However, those figures are far from universal.

Geography as a Financial Determinant

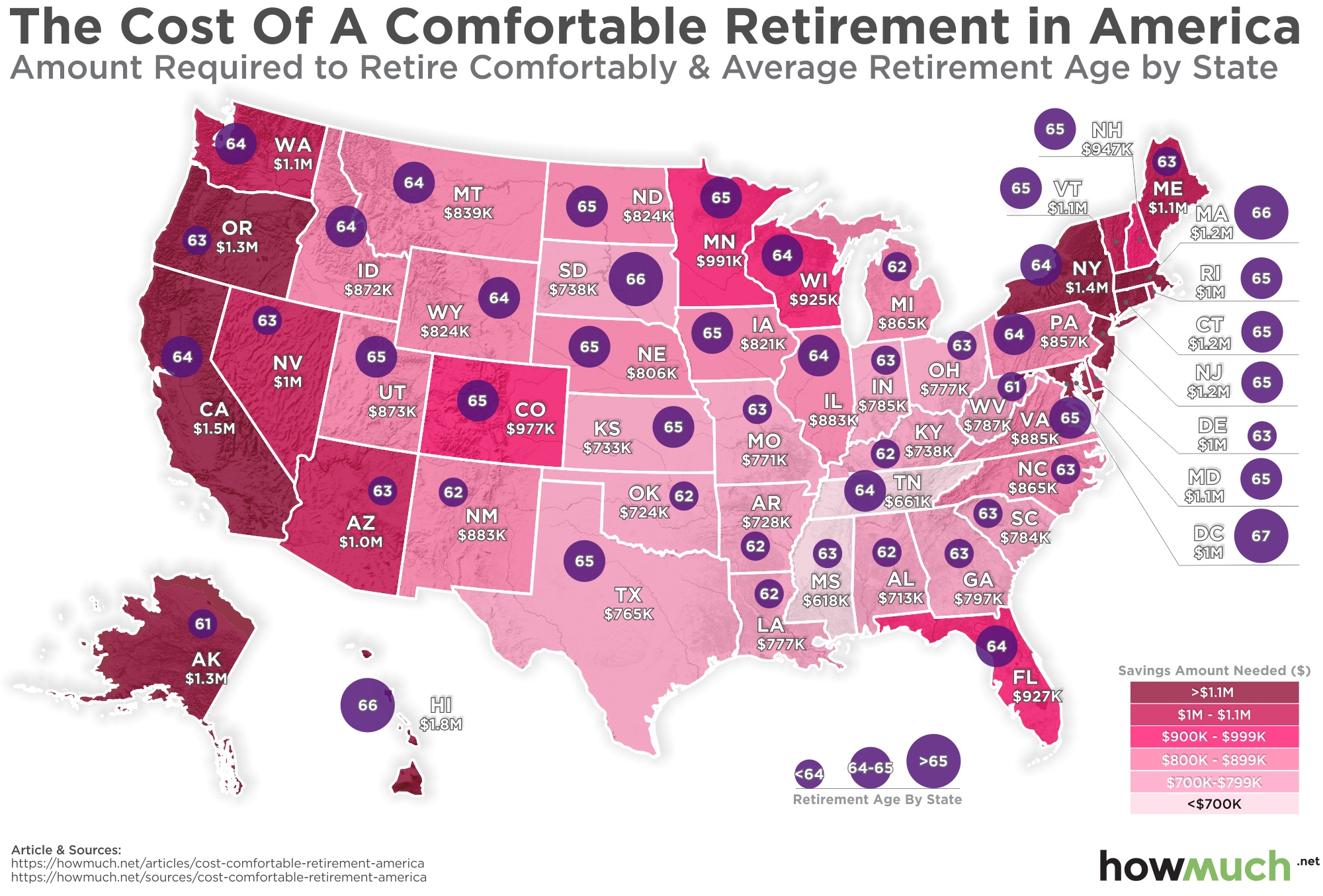

Retirement affordability is tethered to the geographic cost of living.

The Utility of Part-Time Income

Why ZIP Codes Dictate Cash Flow

National averages can be misleading.

Housing: This is typically the largest expense.

Healthcare: Costs vary by state insurance regulations and the availability of provider networks.

Building a Personalized Strategy

For couples mapping out their future, the focus should remain on three core pillars:

Fixed Expenses: Calculate the “must-haves,” including housing, utilities, and insurance.

Discretionary Spending: Define what “comfortable” means for your specific lifestyle, whether that includes travel, hobbies, or supporting family.

Income Streams: Account for Social Security, pensions, and potential part-time earnings before determining the necessary withdrawal rate from investment portfolios.

Relying on a single, generalized savings goal can lead to either unnecessary austerity or a dangerous shortfall. Instead, retirees should use localized cost-of-living calculators that account for the specific tax environment and housing market of their intended retirement destination.

How Much You Need Saved To Retire Comfortably in Every U.S. State (2026 Update)

{kind=link}