{kind=link}

Italy’s Shifting Public Debt Landscape: A Growing Role for Households and Foreign Investors

Recent data from the Bank of Italy reveals a notable shift in the composition of Italy’s public debt, with households and foreign investors playing an increasingly significant role in financing it. This trend, occurring against a backdrop of global instability and evolving market confidence, warrants close attention given Italy’s substantial public debt and sensitivity to market fluctuations.

The Rise of Household and Foreign Investment

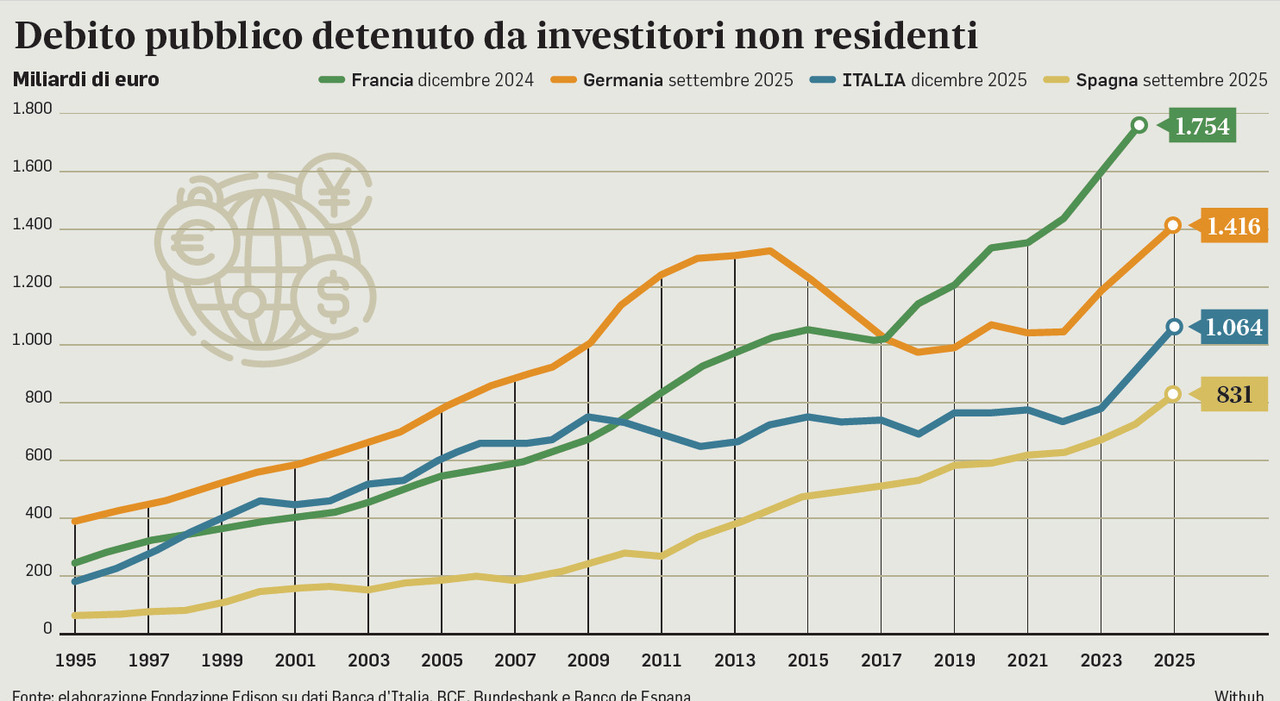

At the conclude of 2025, Italian public debt held by families and businesses reached 447 billion euros, representing 19.8% of the country’s GDP. Simultaneously, debt held by non-resident investors climbed to 1,064 billion euros, equivalent to 47.1% of GDP. This marks an acceleration from 2022, as investors regain confidence in Southern European economies.

This increase contrasts with a parallel decrease in the amount of debt held by banks and insurance companies, as well as the Bank of Italy itself.

Historical Context and the Return of Private Investors

Prior to the introduction of the Euro, Italian families and businesses were major holders of the country’s public debt. However, their share diminished initially as lower interest rates on government bonds following the Euro’s adoption made these securities less attractive, particularly amidst financial shocks like the Greek debt crisis.

Now, with the sovereign debt crisis largely behind it, and renewed confidence in Italian bonds, private investors are returning to the market. Eurostat statistics demonstrate a growing interest from Italian families in government bonds, increasing from a low of 9% of GDP in 2021 to 15.6% in 2024. Debt held by national non-financial companies has remained relatively stable at around 3.4% of GDP.

Foreign Investor Confidence and Debt Sustainability

Reassured by political stability and prudent public account management, foreign investors have also increased their holdings of Italian government bonds. The share of debt held by non-resident investors rose from a minimum of 36.5% of GDP in 2023 to 41.6% in 2024 and 47.1% in 2025.

Over the past six years, debt held by families and businesses has increased by 7.1 percentage points of GDP, while that held by non-resident investors has risen by 4.7 percentage points.

As of the end of 2025, the distribution of Italian public debt is as follows:

- Bank of Italy: 18.5%

- Banks: 20.0%

- Insurance companies, funds, other financial intermediaries: 12.7%

- Families and businesses: 14.4%

- Foreign investors: 34.4%

Italy’s public debt held by families and businesses, at 19.8% of GDP, is the highest in the Euro area. However, the share held by national non-financial private individuals remains relatively low compared to France (1.5%) and Germany (2%).

Comparative Analysis with France and Germany

While Italy’s debt held by foreigners and its national financial entities is lower than that of France and Germany in absolute value, the renewed market confidence has resulted in a relatively sustainable percentage of total debt – less than 35%. In contrast, Germany’s share is between 45% and 50%, and France’s exceeds 55%.

At the end of 2025, foreign holdings of Italian debt exceeded 1 trillion euros, while Germany’s reached 1,416 billion euros and France’s was projected to approach or exceed 1,900 billion euros. Foreign investors have significantly financed the growth of France’s debt, particularly supporting its welfare state.

The Role of “Self-Financing” and the Italy-France Spread

Italy benefits from a significant level of “self-financing” through debt held by families and businesses. Without this, Italy’s debt-to-GDP ratio would effectively drop to 117.3% at the end of 2025. This dynamic, coupled with the changing investor landscape, helps explain the recent narrowing – and occasional reversal – of the spread between Italian and French government bonds.

As France faces concerns regarding its debt levels and political reforms, foreign investors are demanding higher rates, while Italy’s domestic support provides a stabilizing force.

Related: Iran Conflict and Italian Markets

Bank of Italy on Public Debt in January

Keep reading