{kind=link}

South Korea’s Household Loan Market: Interest Rates Rise Amidst Easing Regulations

South Korea’s household loan market is experiencing a complex shift, with lending interest rates increasing even as deposit rates fall and financial authorities consider easing regulations. This divergence is driven by changing market expectations regarding base interest rate cuts and a decrease in demand for loans, coupled with rising global interest rate trends.

COFIX and Deposit Rate Trends

According to the Korea Federation of Banks, the COFIX (Cost of Funds Index) ratio, based on January transactions, was 2.77%, a decrease of 0.12 percentage points from the previous month’s 2.89%.1 While COFIX had risen for four consecutive months, this marks a turning point after five months. The decline in COFIX is attributed to falling bank deposit interest rates. For example, NH Nonghyup Bank lowered its highest interest rate for one-year term deposits from 3% to 2.9% in January, effectively eliminating 3% term deposit rates from the five major banks (Kookmin, Shinhan, Hana and Woori).1

Banks experienced a decreased need for funding due to continued conservative loan execution and a decline in lending opportunities, contributing to the lower COFIX.1

Rising Lending Interest Rates

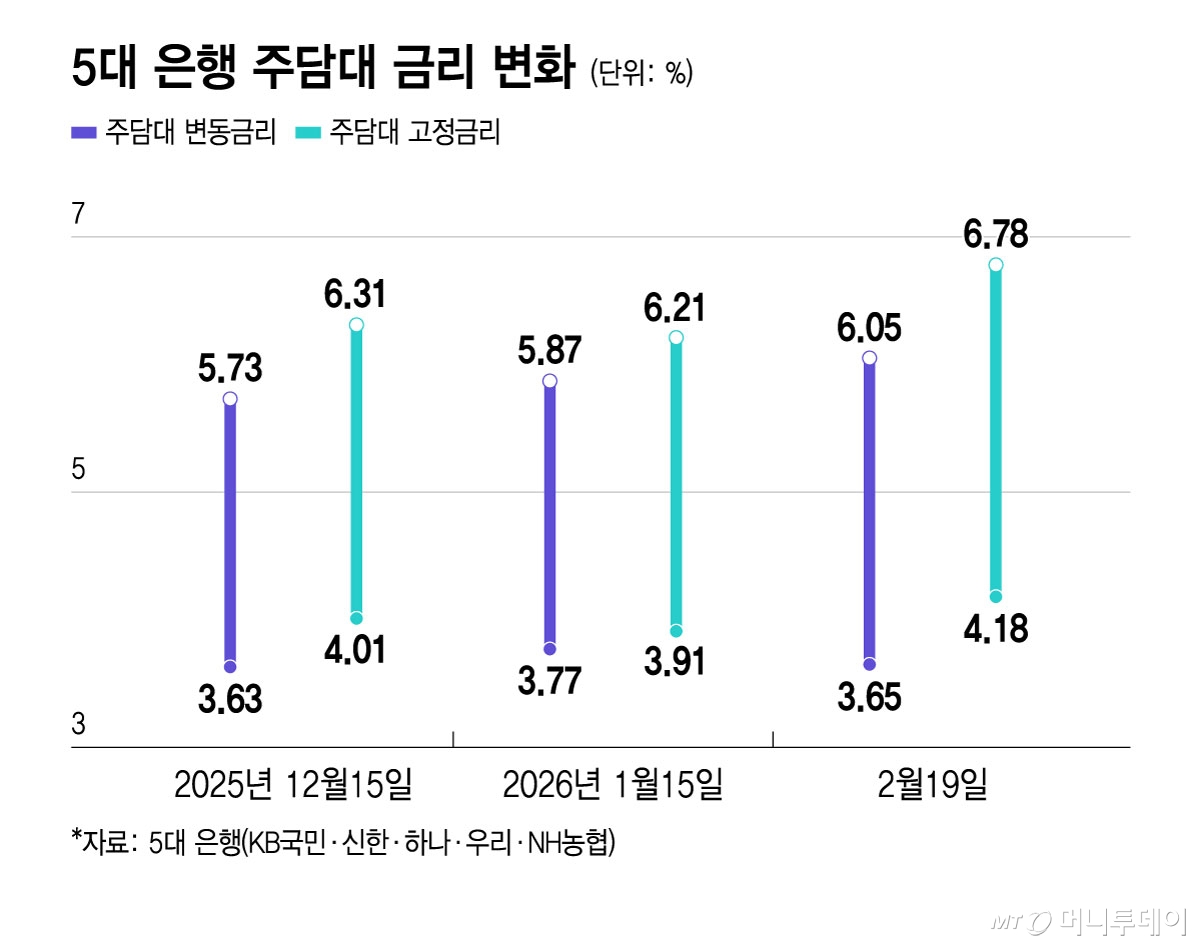

Despite the falling COFIX, lending interest rates are on the rise. As of February 19, 2026, variable interest rates for home mortgage loans from the five major banks ranged from 3.65-6.05%, an increase of 0.18 percentage points from January 15th (3.77-5.87%).1 Fixed-rate mortgage products saw an even larger increase, rising 0.57 percentage points from 3.91-6.21% to 4.18-6.78% during the same period.1

This increase in lending rates is linked to rising market interest rates and diminishing expectations of a base interest rate cut. The interest rate on 3-year Treasury bonds closed at 3.140% on February 13th, up from 2.950% at the conclude of the previous year. Similarly, the interest rate on 5-year financial bonds, a benchmark for fixed mortgage products, rose from 3.499% to 3.687% over the same timeframe.1

Government Response and Market Outlook

The Bank of Korea’s decision to freeze the base interest rate on February 15th and remove references to potential rate reductions from its official statement has further fueled expectations of stable or even increasing interest rates.1 The banking sector anticipates that rising loan interest rates will persist due to limited loan demand and the potential for further increases in market interest rates.

In response to the rising lending rates, financial authorities are considering the introduction of long-term fixed-interest rate mortgage products, potentially with maturities of up to 30 years. Currently, most fixed-rate mortgages in South Korea have a 5-year fixed-rate period followed by a transition to a variable rate, or interest rates are adjusted every five years.

Household Loan Trends

Household loans extended by South Korean banks have been decreasing. Outstanding household loans stood at 1,172.7 trillion won (US$805.75 billion) at the end of January, down 1 trillion won from the previous month.1 This decline follows the first drop since January 2025, which occurred in December, marking a second consecutive month of decrease. Home-backed loans decreased by 600 billion won in January, while unsecured and other household loans fell by 400 billion won.1

These declines are attributed to tightened lending regulations aimed at stabilizing the housing market.2

Keep reading