{kind=link}

Managed Care in Medicaid: Trends, Challenges, and Future Outlook

Managed care is now the dominant model for delivering healthcare to individuals enrolled in Medicaid. As of 2024, approximately 78% of Medicaid beneficiaries receive their care through comprehensive managed care organizations (MCOs). While managed care is widespread, states retain significant flexibility in determining which populations and services are included, leading to substantial variation across the country.

States and MCOs have faced rate-setting uncertainties following the finish of the COVID-19 pandemic’s continuous enrollment provision, which led to the disenrollment of millions of people. As individuals with fewer healthcare needs were disenrolled, the remaining population often had higher health risks and costs. Looking ahead, changes stemming from the 2025 federal budget reconciliation law are expected to create further challenges for MCO rate setting, impacting enrollment and spending through changes to program financing, work requirements, and eligibility redeterminations. Federal spending cuts and a tighter fiscal climate will likely have implications for states, enrollees, plans, and providers.

1. Capitated Managed Care is the Dominant Delivery System

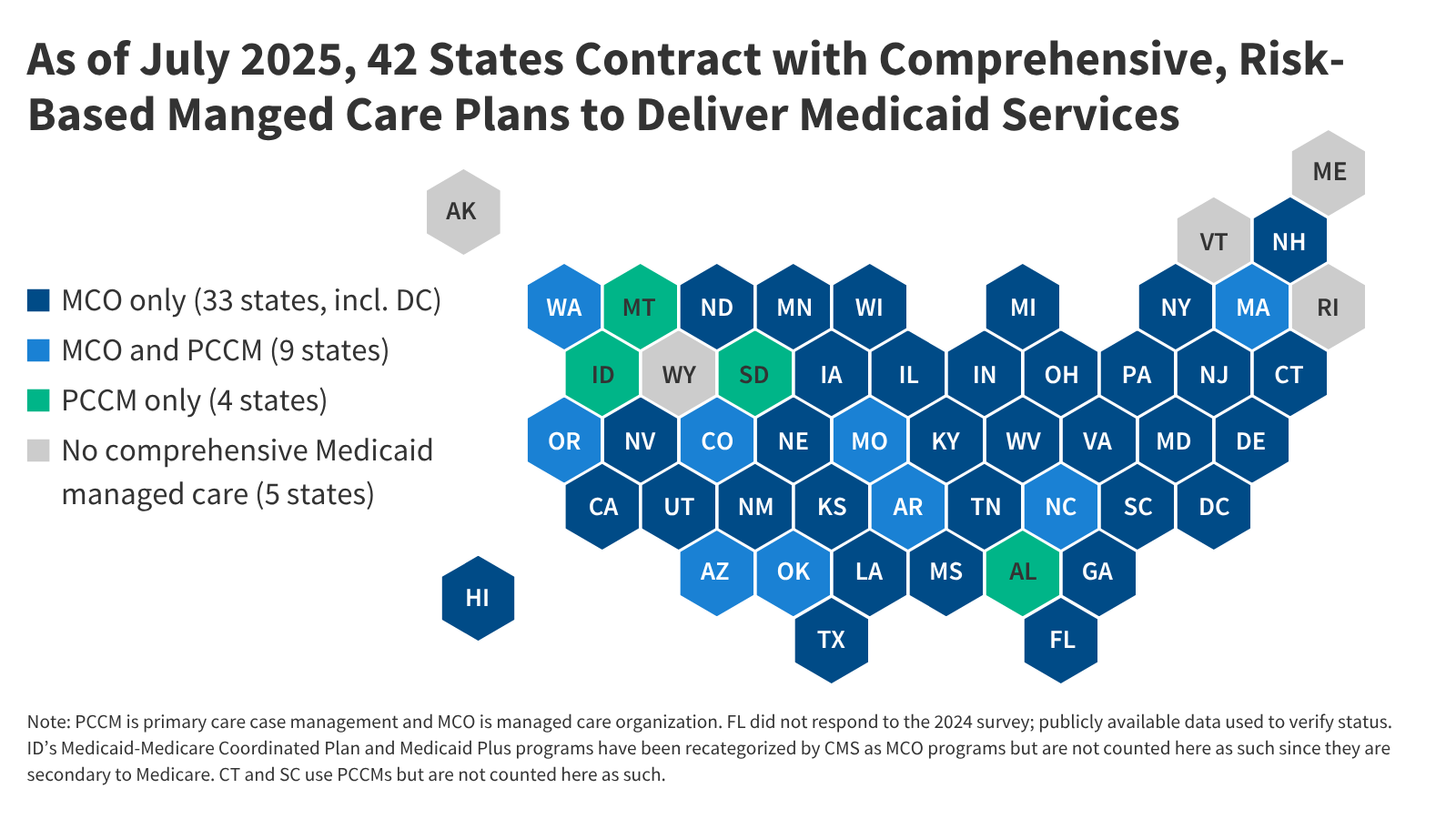

States design and administer their own Medicaid programs within federal guidelines. Nearly all states utilize some form of managed care, including comprehensive risk-based managed care and/or primary care case management (PCCM) programs. As of July 2025, 42 states (including the District of Columbia) contract with comprehensive, risk-based MCOs to provide care to at least some Medicaid beneficiaries. Oklahoma recently joined this group, implementing capitated, comprehensive Medicaid managed care for most children and adults on April 1, 2024. Idaho is transitioning away from PCCM programs and plans to implement comprehensive MCOs by January 2030. Medicaid MCOs provide comprehensive acute care and, in some cases, long-term care, receiving a set per-member-per-month payment for these services.

2. MCOs Account for Half of Medicaid Spending

In fiscal year 2024, total state and federal Medicaid spending reached $919 billion. Payments to MCOs accounted for approximately 50% of this total. The share of spending allocated to MCOs varies by state, influenced by factors such as the proportion of the Medicaid population enrolled in MCOs, the health profile of the population, and whether high-risk beneficiaries are included in MCO enrollment.

3. Over Three-Quarters of Beneficiaries are in MCOs

As of July 1, 2024, over 66 million Medicaid enrollees – 78% of the total – received care through risk-based MCOs. Thirty states had at least 75% of their Medicaid beneficiaries enrolled in MCOs.

4. Children and Adults are Most Likely Enrolled

Children and adults eligible through the Affordable Care Act (ACA) expansion are most likely to be enrolled in MCOs, with enrollment rates of 90% and 86%, respectively. Approximately 72% of other adults (parents and pregnant individuals) were enrolled in comprehensive MCOs in 2023. Individuals eligible through disability pathways and those aged 65+ are less frequently enrolled, although states are increasingly including these groups in MCOs over time.

5. Market Concentration Among MCOs

As of July 2024, there were 291 Medicaid MCOs operating across the country. Fifteen parent firms operate MCOs in two or more states, accounting for over 62% of enrollment. Five publicly traded companies – Centene, UnitedHealth Group, Elevance (formerly Anthem), Molina, and Aetna/CVS – control 47% of all Medicaid MCO enrollment.

6. States Determine Service Coverage

While MCOs provide comprehensive services, states decide which services to include within MCO contracts. Common carve-outs include dental, non-emergency medical transportation (NEMT), and behavioral health. Over two-thirds of individuals enrolled in comprehensive MCOs also receive services through limited benefit plans or fee-for-service systems.

7. Rate Setting and Risk Mitigation

MCOs are financially at risk for covered services, receiving capitation payments from states. Capitation rates must be actuarially sound and may incorporate risk mitigation strategies. States may use risk-sharing arrangements, risk adjustments, or medical loss ratios (MLRs) to manage financial risk. States are required to ensure an MLR of at least 85%, but are not always required to enforce remittance payments when MLR standards are not met.

8. Changes to State Directed Payments

States are generally prohibited from directing how MCOs pay providers, but may implement state directed payments (SDPs) with CMS approval. The 2025 federal budget reconciliation law introduces changes to SDP rules, potentially impacting provider payments.

9. Strengthening Access Standards

The Biden administration finalized rules in 2024 to strengthen access standards and improve the quality of care in Medicaid managed care. These rules establish national maximum wait time standards for routine appointments and enhance state monitoring and enforcement efforts. The future of these rules is uncertain.

10. Improving Program Monitoring and Transparency

CMS has taken steps to improve managed care program monitoring and transparency, including developing standardized reporting templates and releasing informational bulletins. CMS began publicly posting the Managed Care Program Annual Report (MCPAR) and MLR Summary Reports on Medicaid.gov in 2024.