{kind=link}

Understanding Medicare Advantage: A 2026 Guide to Benefits and Coverage

For millions of Americans, navigating the choice between traditional Medicare and Medicare Advantage (MA) is a critical annual task. As we move through 2026, understanding how these private plans function is essential for managing your healthcare costs and access to services.

What is Medicare Advantage?

Medicare Advantage, often referred to as Medicare Part C, allows private insurance companies to provide your Medicare benefits. When you enroll in an MA plan, the federal government pays these private insurers a set amount per month to cover your care. These payments are adjusted based on factors such as your county of residence, your health status, and the plan’s quality star rating.

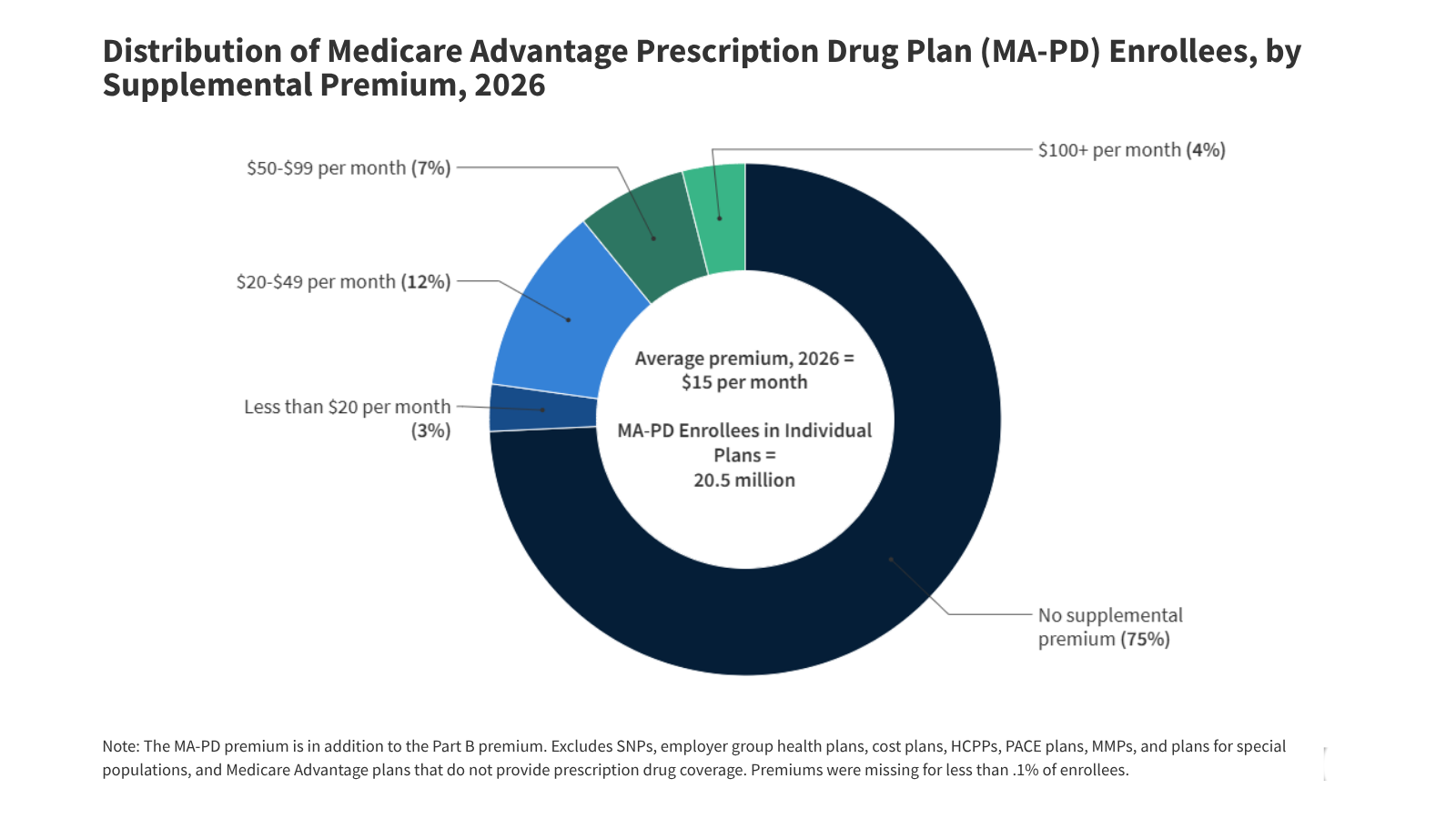

Because these plans receive federal payments, they are often able to offer supplemental benefits—such as dental, vision, and hearing coverage—that traditional Medicare does not typically include. Many plans also provide these benefits without charging an additional premium beyond your standard Medicare Part B payment.

Key Trends for 2026

As of 2026, the landscape of Medicare Advantage continues to evolve. Here is what beneficiaries should know:

- Premium Stability: A significant majority of enrollees in individual Medicare Advantage plans with prescription drug coverage pay no monthly premium other than their standard Medicare Part B premium.

- Out-of-Pocket Protections: Unlike traditional Medicare, which does not have a cap on out-of-pocket spending, all Medicare Advantage plans are required to set an annual limit on your out-of-pocket costs for Part A and Part B services.

- Prior Authorization: Nearly all Medicare Advantage enrollees are in plans that require prior authorization for certain services. This process is most frequently applied to high-cost care, such as inpatient hospital stays, skilled nursing facility stays, and specific Part B drugs.

- Supplemental Benefits: While vision, dental, and hearing benefits remain widely available, the availability of some other extras—such as over-the-counter benefits, transportation, and meal services—has seen some fluctuation compared to previous years.

Essential Considerations for Beneficiaries

While the prospect of “extra” benefits and zero-premium plans is attractive, it is important to look at the fine print. Medicare Advantage plans often utilize networks of providers. This means your choice of doctors and hospitals may be restricted compared to traditional Medicare, which is accepted by most providers nationwide.

the use of prior authorization can sometimes act as a barrier to receiving care. Before enrolling, it is wise to verify whether your preferred physicians are in the plan’s network and to understand the specific requirements for obtaining approval for procedures or specialists.

Frequently Asked Questions (FAQ)

Does Medicare Advantage cover prescription drugs?

Most Medicare Advantage plans include prescription drug coverage (MA-PD). If you choose a plan that does not include drug coverage, you generally cannot join a stand-alone Medicare Part D plan.

What is a Special Needs Plan (SNP)?

SNPs are a type of Medicare Advantage plan designed for individuals with specific health needs or circumstances, such as those who are dually eligible for both Medicare and Medicaid, or those with certain chronic conditions. These plans often provide more tailored benefits and care coordination.

How do I report Medicare fraud?

Protecting your identity is crucial. Never share your Medicare Number with anyone who calls, emails, or texts you unexpectedly. If you suspect fraud or medical identity theft, you should report it immediately through official channels at Medicare.gov.

Final Thoughts

The decision to enroll in a Medicare Advantage plan is a personal one that should be based on your specific health needs, budget, and provider preferences. As you evaluate your options, remember to look beyond the marketing of “zero-premium” plans and consider the total cost of care, including deductibles, copayments, and the potential impact of network restrictions on your access to your preferred healthcare providers.

For the most accurate information regarding plans in your specific area, always utilize the official resources provided by the federal government at Medicare.gov, where you can compare plans and view current provider networks.