{kind=link}

The Impact of Expiring Enhanced Premium Tax Credits on ACA Marketplace Enrollment in 2026

The expiration of enhanced premium tax credits, established by the American Rescue Plan in 2021 and extended through 2025 by the Inflation Reduction Act, has significantly affected Affordable Care Act (ACA) Marketplace enrollment. These credits, which reduced premiums for millions of Americans, ended at the end of 2025, leading to sharp increases in premium payments and a notable decline in coverage. This article examines the early indicators of the impact on enrollment, plan selections, and out-of-pocket costs in 2026.

Key Findings: Enrollment Decline and Premium Increases

According to data from the Centers for Medicare & Medicaid Services (CMS) and state-based Marketplace (SBM) Open Enrollment reports, average monthly effectuated ACA Marketplace enrollment is projected to fall to approximately 17.5 million people in 2026, down from 22.3 million in 2025. This represents a potential drop of 4.8 million people. The decline is most pronounced among individuals with incomes just above 400% of the federal poverty level (FPL), who had previously benefited from the enhanced subsidies.

premium payments for ACA Marketplace enrollees increased by an average of 58% from $113 to $178 per month. This is lower than the 114% increase projected by the Kaiser Family Foundation (KFF) if all enrollees had remained in their original plans. The discrepancy arises because many individuals switched to higher-deductible bronze plans, and those just above the subsidy cliff (400%-500% FPL) were more likely to drop coverage entirely.

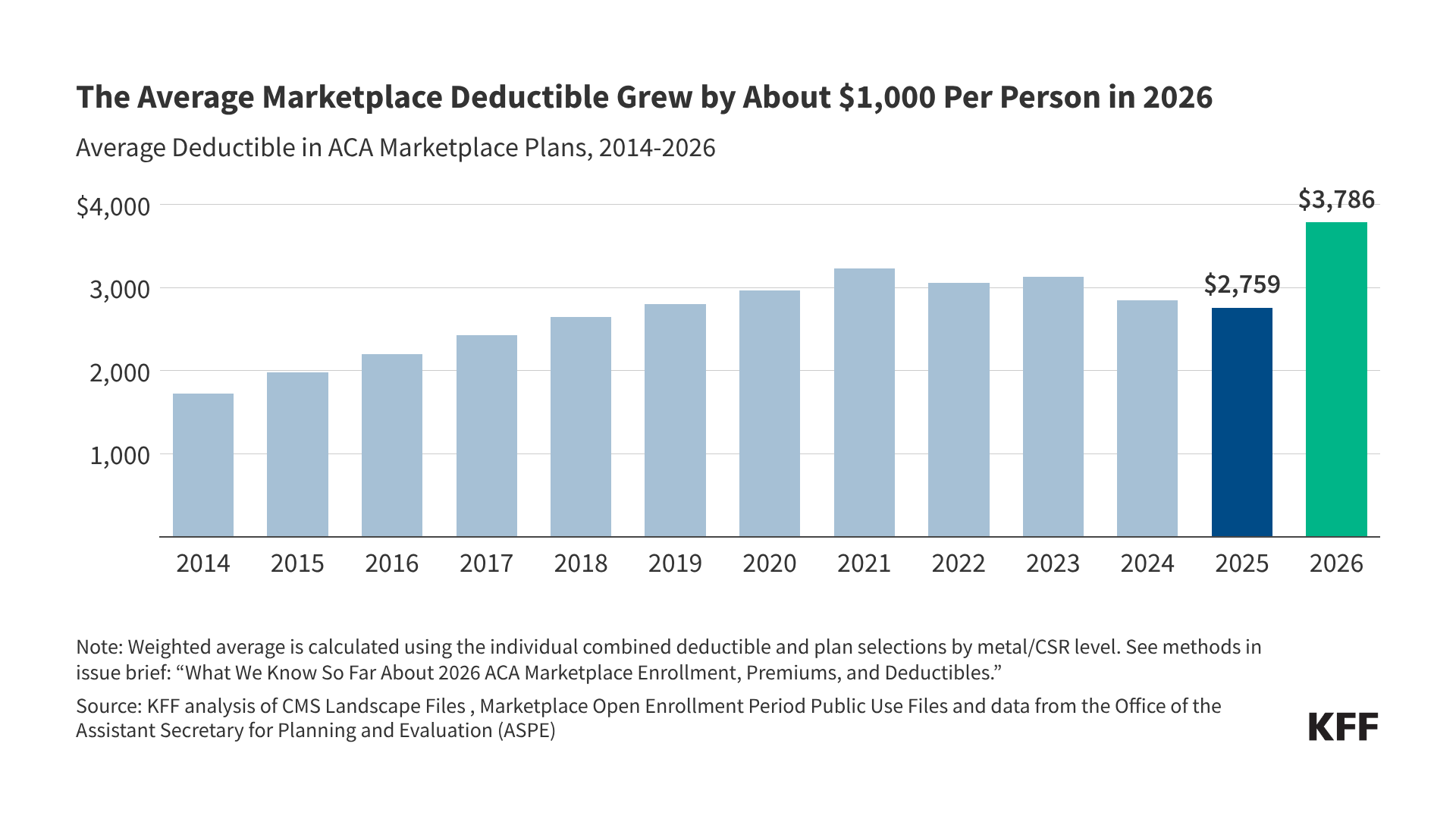

Shift to Higher-Deductible Plans

The average ACA Marketplace deductible increased by 37% (or $1,027 per person) to a record high of $3,786 in 2026. This marks the steepest increase in deductibles ever recorded in the individual market. The shift from silver plans, which offered reduced deductibles for lower-income enrollees, to bronze plans with high deductibles reflects the financial burden on those losing subsidies.

The share of consumers selecting bronze plans rose from 30% (7.3 million people) in 2025 to 40% (9.2 million people) in 2026. Conversely, the share of silver plan selections fell to 43%, the lowest on record. This trend underscores the financial challenges faced by individuals without subsidies, who are increasingly opting for plans with lower premiums but higher out-of-pocket costs

Related reading