{kind=link}

Navigating UAE Corporate Tax: Avoiding Common Compliance Pitfalls

When the UAE introduced its corporate tax regime, many businesses anticipated a smooth transition. The country has long been recognized for its investor-friendly policies and transparent regulatory frameworks. However, navigating corporate tax in the UAE requires diligent planning, current knowledge, and a thorough understanding of the Federal Tax Authority’s (FTA) expectations. As companies adapt to this latest landscape, a clear pattern emerges: most compliance issues stem from recurring, preventable mistakes. Understanding these pitfalls and how to avoid them can be the difference between seamless annual filings and costly penalties.

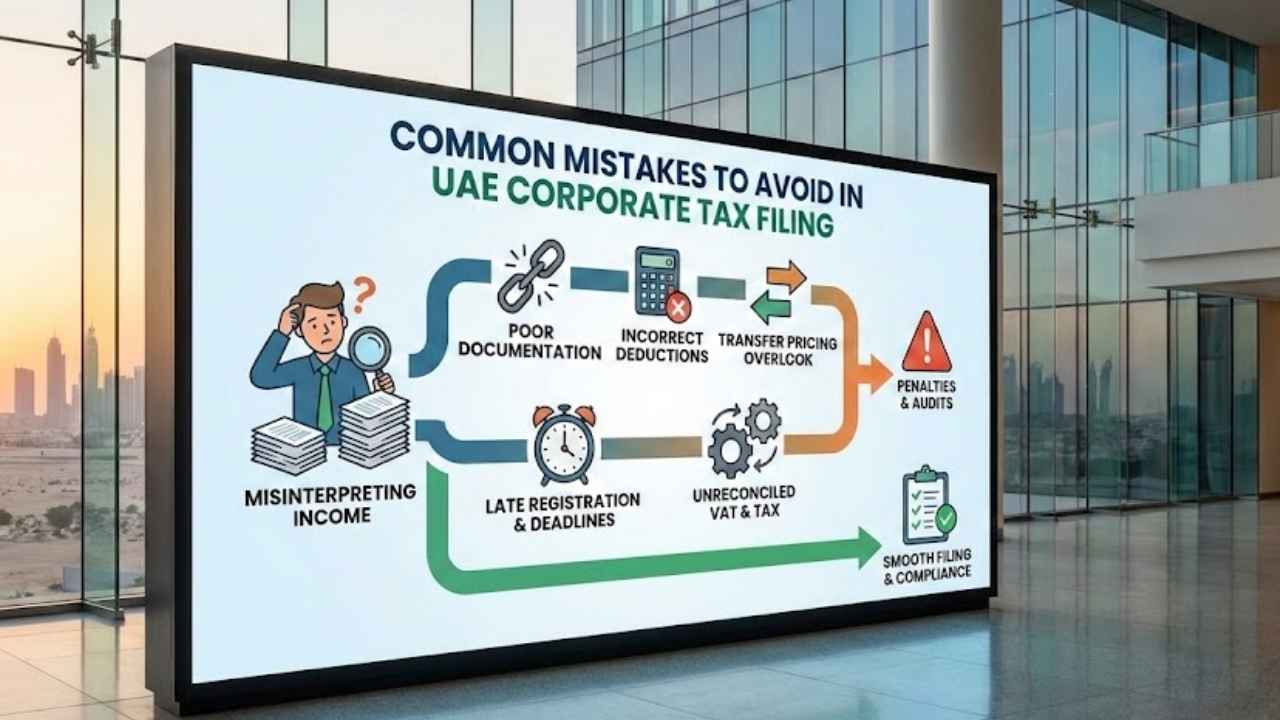

Misinterpreting Taxable and Non-Taxable Income

One of the initial challenges companies face is differentiating between income subject to corporate tax and income that remains exempt. While the law provides clarity, these nuances are easily overlooked. For instance, income from qualifying free zone entities, passive income streams, and certain capital gains may be eligible for preferential treatment, provided specific conditions are met. Misinterpreting these rules can lead to underreporting or overreporting, both of which raise compliance concerns.

A proactive approach is to categorize income streams at the beginning of each financial year, rather than waiting until filing season. This ensures consistency, minimizes disputes, and increases confidence in your calculations.

Poor Documentation and Record-Keeping

Accurate recordkeeping has always been crucial for Value Added Tax (VAT) compliance in the UAE, but corporate tax adds another layer of responsibility. Many businesses still rely on outdated filing systems or fragmented financial data that doesn’t align with statutory requirements. Common issues include missing or incomplete records, unreconciled cash flows, and unsupported expense claims.

The FTA requires records to be clear, organized, and accessible for at least seven years. Without robust documentation, defending your tax return during an audit becomes difficult. Implementing a centralized digital system or partnering with a provider that manages one can help ensure a complete and audit-ready financial trail.

Incorrect Classification of Allowable Deductions

Companies often miss opportunities to reduce their tax liability due to misunderstandings about deductible expenses. Certain expenditures, such as entertainment, penalties, or personal-apply costs, are explicitly non-deductible. Others, like staff expenses, operational costs, or depreciation, require strict calculation methods. Misclassification is particularly common among Small and Medium Enterprises (SMEs) that may lack in-house tax expertise, potentially leading to inflated claims, reduced taxable income, and increased penalty risk.

Establishing a clear internal policy for categorizing expenses, ideally reviewed by a qualified tax professional, is the safest course of action.

Overlooking Transfer Pricing Requirements

Businesses dealing with related parties, whether locally or internationally, must comply with transfer pricing rules. This aspect is often underestimated, as it’s perceived as relevant only to multinational corporations. However, under UAE regulations, even small businesses owned by related individuals may fall within the transfer pricing scope. Proper documentation, arm’s length pricing, and timely submission of transfer pricing disclosures are essential. Ignoring these requirements can result in lengthy assessments and potential adjustments by the authorities.

Late or Incorrect Tax Registration

A recurring mistake is delaying registration for corporate tax. Some businesses assume they are exempt or that the registration deadline doesn’t apply to them. However, the FTA has clarified that every taxable person must register within the specified period, even if their income is below the taxable threshold or if they operate from a free zone. Late registrations attract fines and hinder accurate and timely filing.

Missing Filing Deadlines

As with VAT, missing corporate tax deadlines carries significant costs. Filing and payment timelines are fixed, and penalties for late submissions accumulate rapidly. A simple internal compliance calendar can significantly reduce the risk of missed dates. Many organizations also delegate this responsibility to external tax advisors to ensure consistent oversight and timely filing.

Not Reconciling Corporate Tax and VAT Records

Because both tax regimes rely on accurate financial data, inconsistencies between corporate tax and VAT filings can raise red flags. For example, if revenue declared for VAT doesn’t align with taxable income calculations for corporate tax, it could trigger an audit. Reconciling your books across both tax types ensures your financial statements present a consistent picture, which the FTA closely examines.

corporate tax filings don’t have to be overwhelming. Most mistakes occur because businesses rush the process, overlook details, and lack timely professional guidance. By recognizing common pitfalls and addressing them proactively, companies can strengthen their financial governance and remain compliant with the UAE’s regulatory expectations.