{kind=link}

Hospital Prices: Why Private Insurance Costs Are Outpacing Medicare

For most Americans, healthcare affordability isn’t just a political talking point—it’s a monthly financial burden. While hospital spending accounts for nearly one-third of total healthcare expenditures, the cost of that care varies wildly depending on who is paying the bill. Recent data reveals a widening gap: prices paid by private insurers are climbing significantly faster than those paid by Medicare.

Understanding this disparity is crucial because these costs don’t stay with the insurance companies. They trickle down to patients through higher monthly premiums, steeper cost-sharing obligations, and even reduced wages for employees with employer-sponsored coverage.

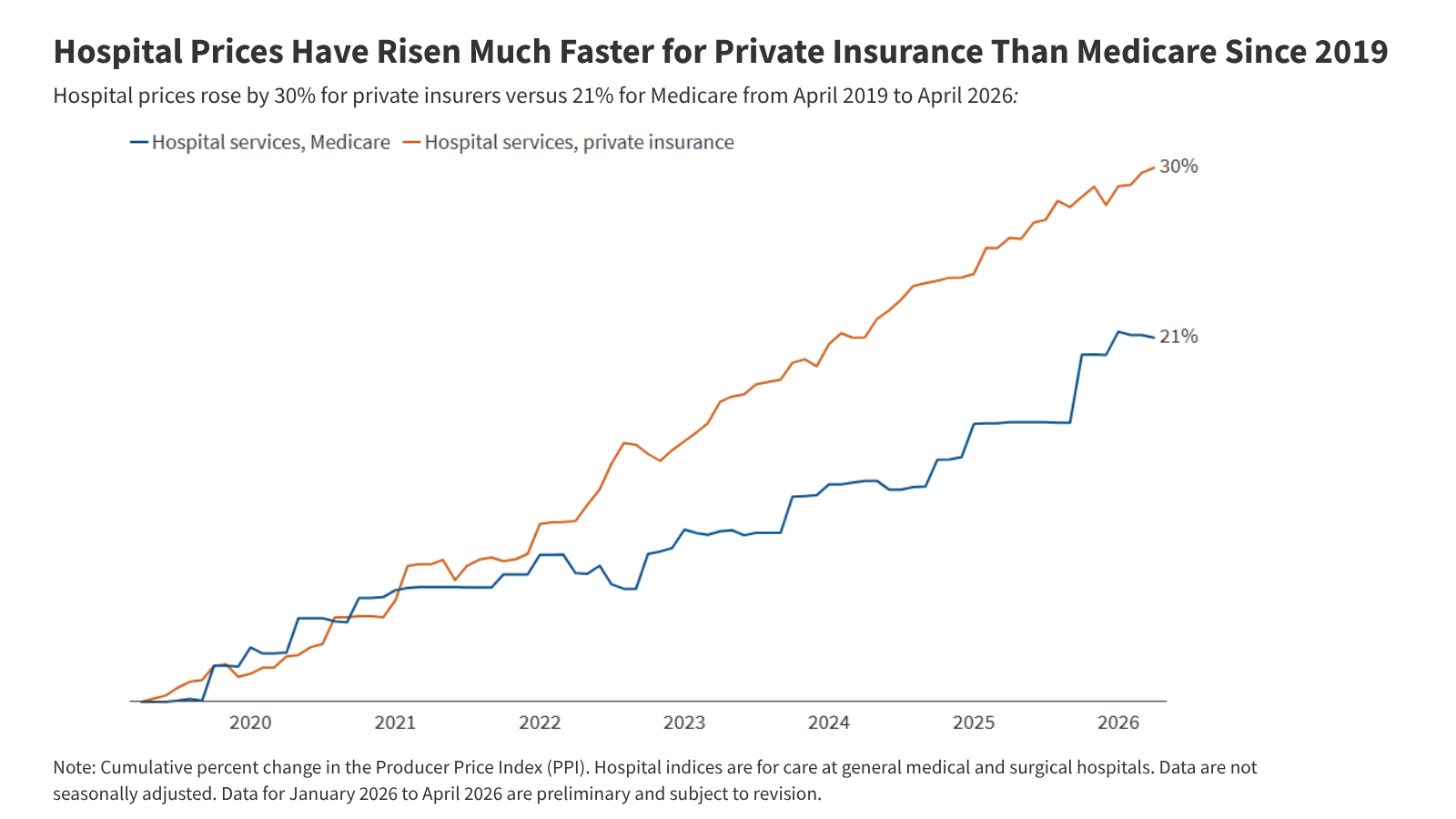

- The Growth Gap: From April 2019 to April 2026, private insurance prices for hospital care rose by 30%, while Medicare rates increased by 21%.

- Accelerated Costs: Private insurance prices grew 47% more quickly than Medicare rates over this seven-year period.

- Market Power: Hospital consolidation is a primary driver, with one or two health systems controlling at least 75% of the inpatient market in 83% of large metropolitan areas as of 2024.

- Regulatory Differences: Medicare rates are set annually by CMS based on law and regulation, while private rates are the result of direct negotiations between hospitals and insurers.

The Data: A Seven-Year Trend of Divergence

To track these trends, analysts utilize the Bureau of Labor Statistics (BLS) Producer Price Index (PPI), which measures prices from the perspective of the service provider. Between April 2019 and April 2026, the divergence in pricing became clear.

While private insurance and Medicare rates grew at a similar pace during the first year (April 2019 to April 2020), private rates accelerated more quickly every year from 2020 through 2025. Although the growth rate for private insurance slowed relative to Medicare between April 2025 and April 2026, the overall gap has widened significantly over the long term.

Why Private Insurance Prices Are Rising Faster

Unlike government-set rates, private insurance prices are determined by negotiations. Several systemic factors have shifted the bargaining power in favor of hospitals:

1. Market Consolidation

When a few large health systems dominate a region, they have more leverage to demand higher prices from insurers. This consolidation is widespread; in 2024, 83% of large metropolitan areas saw one or two health systems controlling at least 75% of the inpatient hospital care market.

2. Inflation and Operating Costs

The pandemic triggered massive spikes in labor and supply expenses. Because hospitals faced higher input costs, they negotiated for higher reimbursement rates. However, because insurance contracts are often multi-year agreements, there is typically a lag before these increased costs are reflected in the final price.

How Medicare Rates Stay Relatively Lower

Medicare operates on a fundamentally different pricing model. Traditional Medicare hospital prices are updated annually by the Centers for Medicare and Medicaid Services (CMS) through the Inpatient and Outpatient Prospective Payment Systems (IPPS and OPPS).

Several mechanisms help restrain Medicare’s price growth compared to the private sector:

- Regulatory Frameworks: CMS sets rates based on estimates of hospital input costs and overall inflation.

- Productivity Adjustments: Under the Affordable Care Act, certain adjustments reduce the growth of traditional Medicare rates, based on the assumption that hospitals are becoming more efficient at delivering care.

- Sequestration: Budgetary rules require automatic reductions in Medicare payments. While these were temporarily suspended starting in May 2020, they were gradually reintroduced in April and July 2022, putting downward pressure on prices.

Policy Responses: Capping the Cost

Lawmakers are increasingly exploring ways to rein in these spiraling costs. Strategies generally fall into two categories: promoting competition to break up consolidated markets or implementing direct price caps.

Some states have already taken aggressive action:

- Indiana: The state recently enacted a law that will eventually cap private insurance prices for nonprofit hospitals.

- Oregon: Since 2019, Oregon has capped hospital prices at 200% of traditional Medicare rates for its state employee plan.

Frequently Asked Questions

What is the Producer Price Index (PPI) and why is it used here?

The PPI measures the price of goods and services from the perspective of the producer (in this case, the hospital). It is preferred over the Consumer Price Index (CPI) for this analysis because it allows researchers to break down price growth by the specific payer, such as distinguishing between Medicare and private insurance.

Do Medicare Advantage plans pay more than traditional Medicare?

Evidence suggests that rates paid by Medicare Advantage plans for hospital services are generally close to the rates paid by traditional Medicare, and their price increases have likely remained aligned over time.

How does hospital consolidation affect the average patient?

While the effect on the quality of care remains unclear, a substantial body of evidence shows that when hospitals consolidate, prices rise. This leads to higher premiums for the insured and higher costs for the uninsured.

Looking Ahead

The widening gap between private and public healthcare pricing highlights a systemic vulnerability in the U.S. Healthcare market. As market consolidation continues to concentrate power in a few large systems, the pressure on private insurers—and by extension, patients—will likely increase. Whether state-level price caps or federal competition policies can effectively bend the cost curve remains the central question for healthcare affordability in the coming decade.

Keep reading