{kind=link}

Understanding the Growth and Landscape of Medicare Advantage in 2026

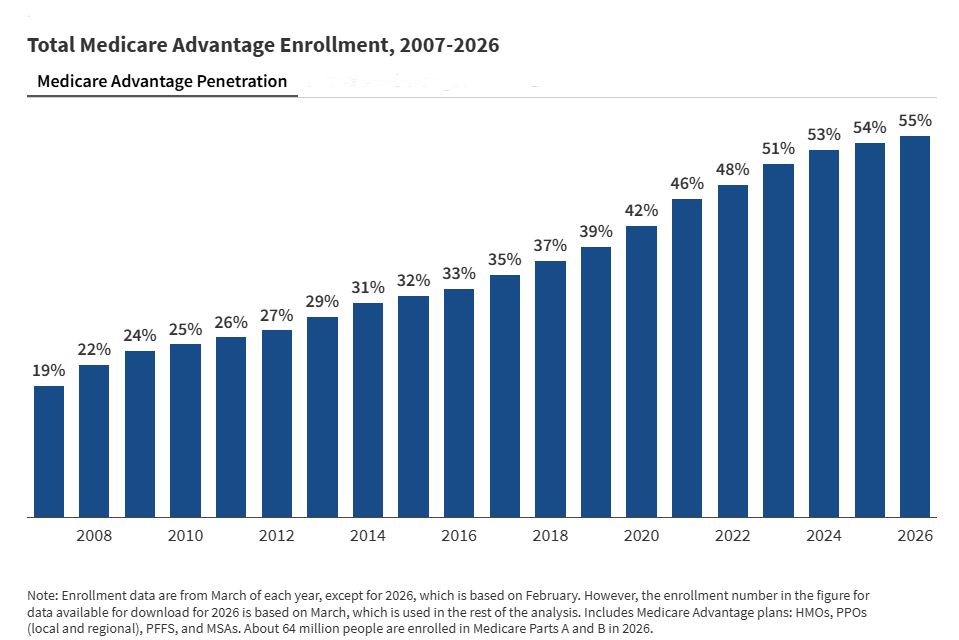

As a physician, I often hear questions from my patients about how to navigate their health insurance options as they approach retirement. One of the most significant shifts in the American healthcare landscape over the last two decades has been the rapid expansion of Medicare Advantage (MA). As of 2026, more than half of all eligible Medicare beneficiaries have chosen these private plan alternatives over traditional, fee-for-service Medicare.

For those trying to make sense of these trends, it is helpful to understand not just the numbers, but the structure of these plans and what they mean for your access to care.

What is Medicare Advantage?

Medicare Advantage, often referred to as Medicare Part C, is a private insurance option that bundles your hospital (Part A) and medical (Part B) coverage. Many of these plans also include prescription drug coverage (Part D) and offer supplemental benefits that traditional Medicare does not typically cover, such as dental, vision, and hearing services. Because these plans are managed by private companies, they often come with their own networks of providers and specific rules regarding prior authorizations for procedures or treatments.

Key Trends in 2026 Enrollment

The growth of Medicare Advantage has been consistent, with 55% of eligible beneficiaries now enrolled in these plans. While the pace of this growth is beginning to stabilize, the composition of the enrollment is shifting toward more specialized care models.

- Special Needs Plans (SNPs): A significant portion of the recent growth—roughly 85% of the net increase in enrollment—has come from Special Needs Plans. These plans are designed for beneficiaries with specific needs, such as those who are dually eligible for Medicare and Medicaid, individuals with severe chronic conditions, or those requiring institutional care.

- Market Concentration: The market remains highly concentrated. Two major parent organizations, UnitedHealth Group and Humana, account for nearly half (46%) of all Medicare Advantage enrollees nationwide. In many counties, these two companies provide the vast majority of available plan options.

- Group Plans: About 16% of enrollees are covered through employer or union-sponsored group plans, which remain a popular way for retirees to maintain benefits that supplement traditional Medicare.

Why Enrollment Matters for Policy

From a public health and economic perspective, the shift toward Medicare Advantage has significant implications. Federal spending on these plans is a frequent topic of debate among policymakers. According to the Medicare Payment Advisory Commission (MedPAC), payments to private plans currently exceed what the government would spend for similar beneficiaries under traditional Medicare. In 2026, these payments are 14% higher per person. Policymakers continue to weigh how to manage these costs without disrupting the supplemental benefits or the plan choices that many beneficiaries have come to rely on.

What This Means for You

If you are exploring your options, it is important to remember that Medicare Advantage is not a “one size fits all” product. Because plans are managed by private insurers, your experience—including your out-of-pocket limits, provider networks, and prior authorization requirements—can vary significantly depending on the plan you choose and where you live.

When evaluating your coverage, consider the following:

- Check Provider Networks: Ensure your preferred physicians and specialists are in-network for the specific plan you are considering.

- Review Supplemental Benefits: If you prioritize dental, vision, or hearing coverage, look closely at the plan’s Evidence of Coverage document.

- Understand Prior Authorization: Some plans require you to get approval before receiving certain services. Make sure you are comfortable with the plan’s requirements before enrolling.

Looking Ahead

The Congressional Budget Office projects that Medicare Advantage enrollment will continue to rise, potentially reaching 63% by 2034. As the program evolves, my best advice remains the same: stay informed. Use official resources, such as Medicare.gov, to compare plans in your area. Understanding the nuances of your coverage is the first step in taking control of your long-term health and wellness.

Disclaimer: I am a physician, but this article is for informational purposes only and does not constitute personalized medical or financial advice. Always consult with a licensed insurance advisor or official government resources when making decisions about your Medicare coverage.

Keep reading