{kind=link}

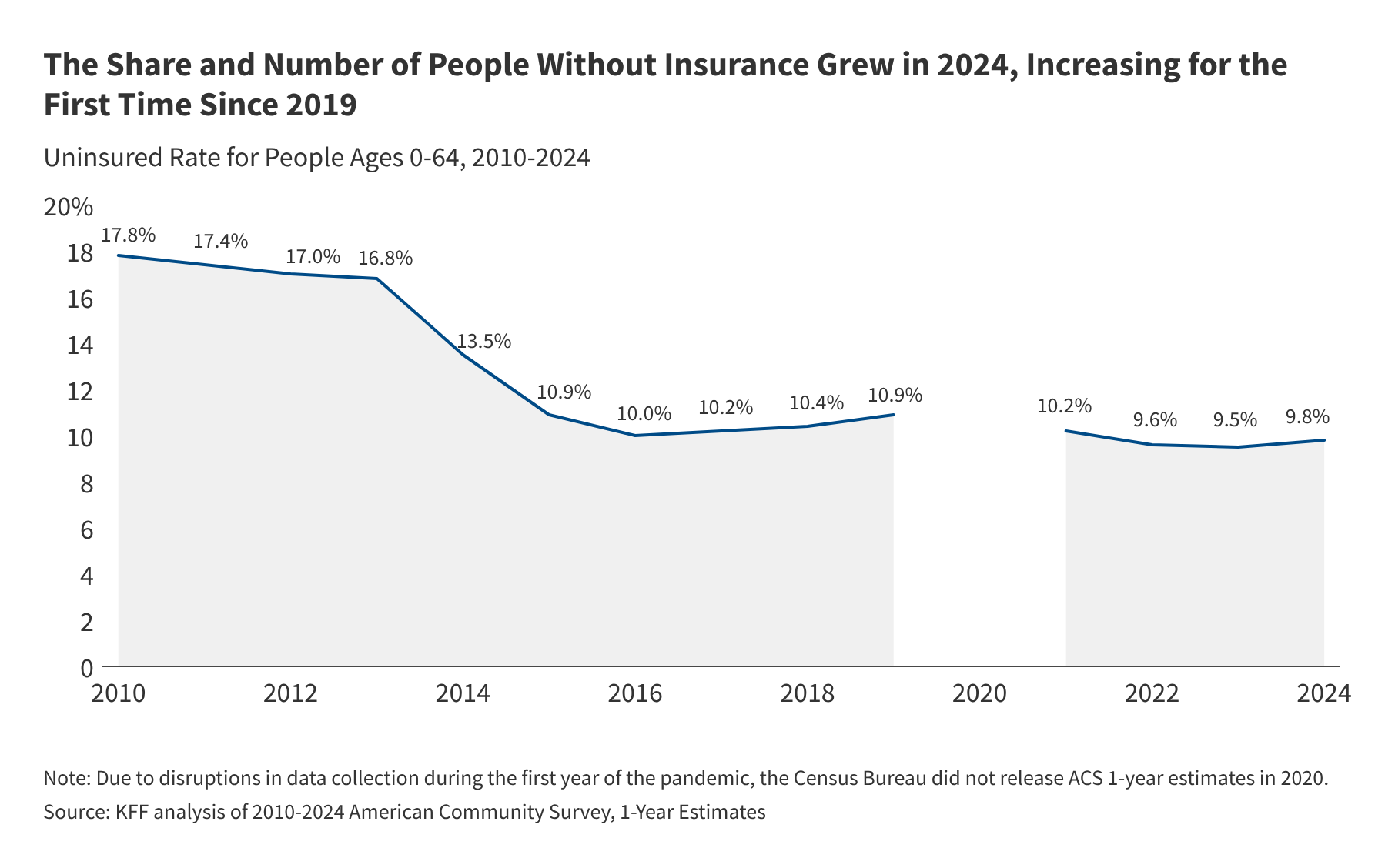

The number of uninsured individuals in the United States reached 26.7 million in 2024, marking the first increase in the uninsured population since 2019, according to data from the Kaiser Family Foundation (KFF). The uninsured rate for the non-elderly population rose to 9.8%, up from 9.5% the previous year, primarily driven by a nationwide reduction in Medicaid enrollment as states resumed eligibility redeterminations.

Why is the uninsured rate increasing?

The primary driver behind the rising uninsured rate is the “unwinding” of the Medicaid continuous enrollment provision. During the COVID-19 pandemic, states were prohibited from disenrolling members; once that requirement ended in 2023, millions were removed from the program. While enrollment in Affordable Care Act (ACA) Marketplace plans reached record highs in 2024, these gains were insufficient to fully offset the loss of Medicaid coverage, according to KFF researchers. Additionally, rising premiums and the expiration of certain enhanced tax credits have made private insurance less accessible for low-to-middle-income families.

Who is most likely to be uninsured?

Demographic data reveals persistent disparities in health coverage. According to the U.S. Census Bureau, individuals in low-income families and people of color face the highest risks.

* Employment status: Approximately 85% of uninsured individuals are part of a family with at least one worker, yet many report that their employer does not offer coverage or that they are ineligible due to part-time status.

* Geographic location: Residents of states that have not expanded Medicaid are nearly twice as likely to be uninsured—14.5% compared to 8.0% in expansion states—as noted by KFF.

* Race and ethnicity: American Indian, Alaska Native, Hispanic, and Black populations remain disproportionately represented among the uninsured compared to White and Asian counterparts.

How does being uninsured affect healthcare access?

Lack of insurance functions as a significant barrier to receiving timely medical care. Data from the National Center for Health Statistics indicates that uninsured adults are more than twice as likely as those with private or public coverage to delay or forgo necessary medical treatment due to cost.

For patients managing chronic conditions like diabetes or hypertension, the consequences are particularly severe. Uninsured individuals with these conditions are three to four times more likely to skip medication or routine check-ups. This leads to higher rates of emergency department utilization and worse long-term health outcomes, as preventable conditions often escalate into medical emergencies.

What are the financial consequences for the uninsured?

Financial distress is a common outcome for those without coverage. According to a report by the Urban Institute, nearly 60% of uninsured adults report difficulty paying for medical care, compared to 30% of insured adults. This often results in a cycle of debt, as uninsured patients are more likely to:

* Overdraw bank accounts to cover out-of-pocket costs.

* Face collections actions from medical providers.

* Incur “medical debt,” which can negatively impact credit scores and housing stability.

Frequently Asked Questions

Am I eligible for Medicaid or Marketplace subsidies?

About half of all uninsured people qualify for either Medicaid or subsidized Marketplace plans, according to federal estimates. Eligibility depends on state expansion status and household income.

Why is employer-sponsored insurance often unavailable?

Many low-wage workers are excluded from employer plans because they work part-time or their employer does not offer a health benefit package.

Does having insurance improve health outcomes?

Yes. Research consistently shows that gaining coverage—especially through Medicaid—increases the use of preventive services, improves management of chronic diseases, and reduces mortality rates.

Keep reading