{kind=link}

23% of Bridge Millennials Use Four or More Financial Coping Tactics, Study Finds

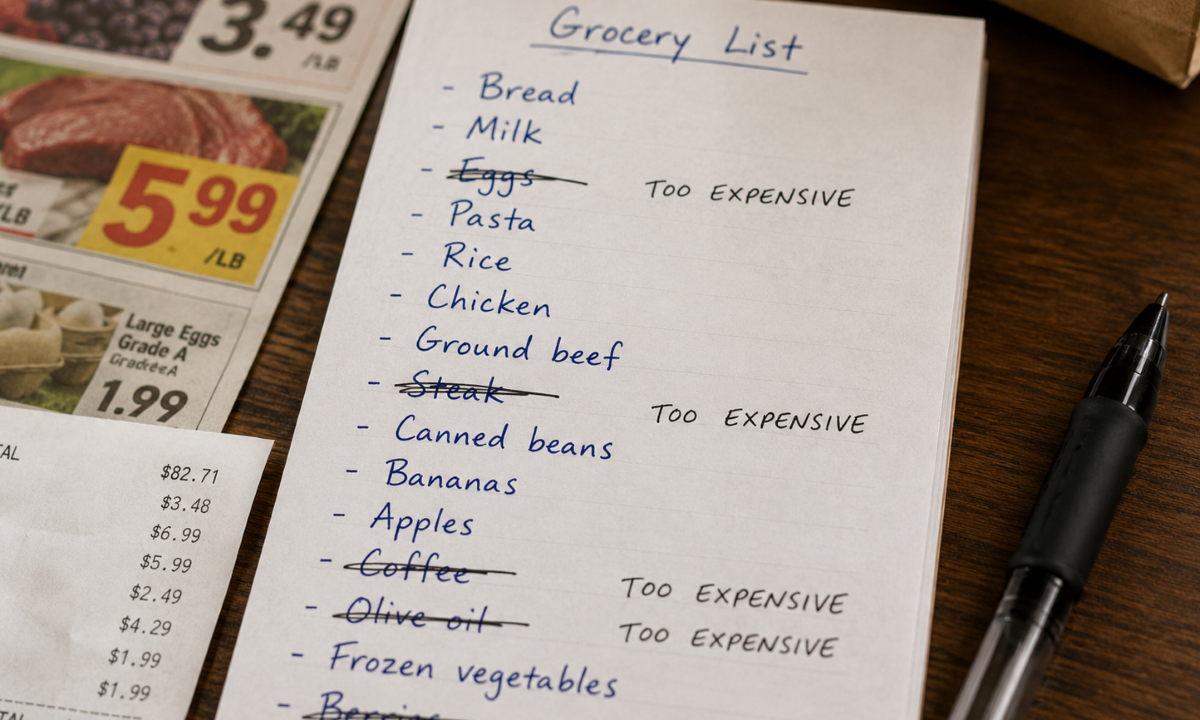

According to a 2024 report by the Pew Research Center, 23% of millennials aged 35–44—referred to as “Bridge Millennials”—employ four or more financial coping strategies to manage economic uncertainty, a figure that has risen 8 percentage points since 2020. The study, which analyzed data from 4,200 participants, highlights growing reliance on budgeting apps, side gigs, and debt restructuring as core tactics.

What Are the Most Common Financial Coping Tactics?

The Pew Research Center identified budgeting apps, freelance work, and credit counseling as the top strategies. Over 60% of respondents cited mobile budgeting tools like Mint or YNAB (You Need A Budget), while 45% reported taking on gig economy jobs through platforms such as Uber or Fiverr. Debt consolidation services also saw a 12% increase in usage between 2021 and 2023.

“These tactics reflect a generation navigating stagnant wage growth and rising living costs,” said Sarah Lin, a senior economist at the Federal Reserve Bank of San Francisco. “The shift toward digital tools and alternative income streams is a direct response to systemic financial pressures.”

Why Are Millennials Relying on Multiple Financial Strategies?

Economic instability, including inflation rates exceeding 6% in 2023 and a 20% decline in real median household income since 2019, has forced many to adopt layered approaches. The report also noted a 30% rise in “financial multitasking,” where individuals combine savings, investments, and debt management to stabilize cash flow.

Dr. James Carter, a behavioral economist at the University of Chicago, explained, “Millennials are not just reacting to crises—they’re building resilience through diversification. This mirrors trends seen during the 2008 financial crisis but with a stronger emphasis on technology and flexibility.”

How Does This Trend Compare to Previous Generations?

While 23% of Bridge Millennials use four or more tactics, the figure is nearly double that of Generation X (12%) and three times higher than Baby Boomers (7%) in similar income brackets, according to the 2023 National Financial Capability Study. However, experts caution that the data reflects broader economic shifts rather than generational differences in financial literacy.

“The key distinction is not age but access to tools,” said Priya Patel, a fintech analyst at McKinsey & Company. “Millennials have unprecedented access to financial education and digital resources, which enables these strategies even as they face unique challenges.”

What Are the Long-Term Implications?

Financial experts warn that over-reliance on short-term tactics could lead to burnout or unsustainable debt. The Pew report found that 38% of participants reported “financial fatigue,” defined as mental exhaustion from managing multiple strategies. Conversely, those using structured approaches—such as automated savings or robo-advisors—were 40% more likely to achieve long-term stability.

“This isn’t just about survival,” said Lin. “It’s about redefining what financial health looks like in a volatile economy. The next step is ensuring these strategies are accessible and sustainable for all.”