{kind=link}

Rising Euribor and Iran Tensions Prompt Calls for Mortgage Holders to Switch to Fixed Rates

As the war in Iran escalates, concerns are mounting over potential inflation and subsequent interest rate hikes, putting pressure on Spanish mortgage holders. Economic expert Gonzalo Bernardos advises those with variable-rate mortgages, particularly those with over 10 years remaining on their loans, to consider switching to fixed rates.

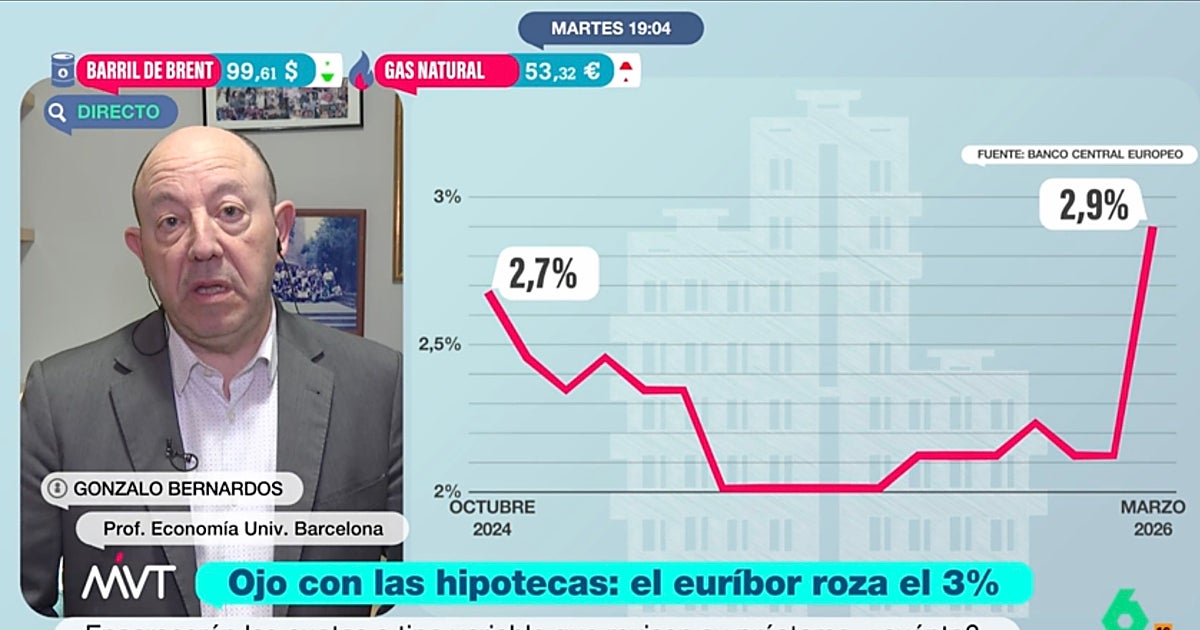

Euribor Reaches Highs Not Seen Since 2024

The twelve-month Euribor, the primary indicator for calculating variable mortgages in Spain, is nearing 3% in daily rates, reaching levels not observed since September 2024. This increase is fueled by the geopolitical instability in Iran and the resulting anxieties about rising energy prices and inflation.

ECB’s Potential Response to Inflation

Bernardos suggests that the European Central Bank (ECB) is likely to respond to increased inflation by raising interest rates, mirroring its actions following the Russian invasion of Ukraine in 2022. He recalls that in January 2022, inflation stood at 5.1%, yet the ECB maintained a 0% interest rate until July, before ultimately increasing rates. The ECB has indicated it has learned from past mistakes and may act more swiftly to address inflation if the conflict in Iran persists.

Fixed-Rate Mortgage Options Still Available

Despite the rising Euribor, Bernardos highlights that fixed-rate mortgages are still available at competitive rates. He specifically mentions that wholesale mortgage lenders are offering fixed rates as low as 2.4%. This presents an opportunity for variable-rate mortgage holders to secure a more predictable and potentially lower interest rate.

Impact of Euribor Increase on Mortgage Payments

The increase in the Euribor will translate to higher mortgage payments for those with variable-rate loans. For a €150,000 mortgage, the annual savings from a lower Euribor could be around €48, even as for a €300,000 mortgage, it could be approximately €96. While, with the Euribor climbing, these savings are diminishing.

The advice from experts like Gonzalo Bernardos underscores the importance of proactively reviewing mortgage options in the face of economic uncertainty and geopolitical events.

Keep reading